Let’s say you’re living abroad now.

You used to deposit money in your Indian post office savings account. Maybe you also had a PPF. Or an NSC. Now, you’re wondering—Can I still keep these accounts as an NRI? Or will the rules kick you out?

It’s not just a “yes” or “no” answer. The truth lies in what type of post office scheme you’ve invested in—and when. Plus, FEMA (Foreign Exchange Management Act) and RBI regulations play a huge role here.

Let’s break it all down.

What Happens to Your Post Office Account After NRI Status?

So, the day you officially become an NRI—what changes?

Plenty.

First off, under FEMA rules, your residential status affects your eligibility to hold certain accounts in India. That includes post office schemes.

Once you leave India for employment, education, or residency abroad for over 182 days, you’re no longer considered a “resident” under FEMA. That means your existing investments? They may no longer be valid under Indian law.

But don’t panic.

Some accounts let you continue until maturity. Others require you to close them ASAP. It depends on the scheme.

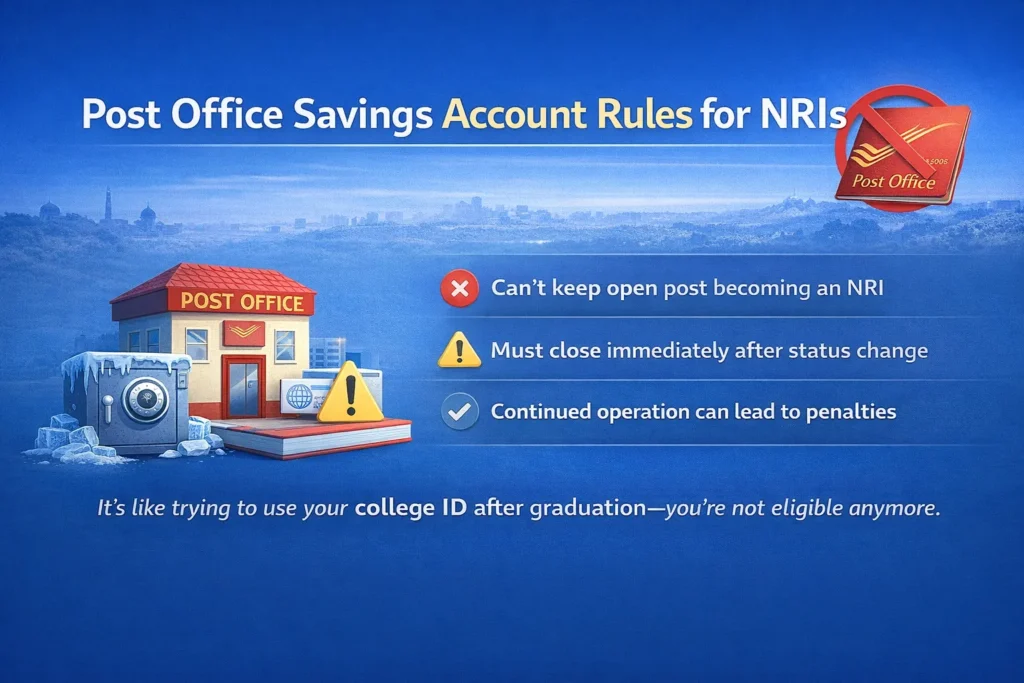

Post Office Savings Account Rules for NRIs

Here’s the thing: the plain old Post Office Savings Account is strictly meant for resident individuals.

As soon as you become an NRI:

- You’re not allowed to keep this account open.

- You must close it immediately upon a change of residential status.

- Continued operation can lead to penalties, account freeze, or even interest denial.

Think of it like this: It's like trying to use your college ID after graduation. You're not eligible anymore.

Restrictions faced by NRIs

Non-Resident Indians (NRIs) face specific restrictions regarding investments in Indian Post Office savings schemes. Here’s an overview:

Opening New Accounts: NRIs are not permitted to open new Post Office savings accounts or invest in schemes such as the Public Provident Fund (PPF), National Savings Certificate (NSC), and other small savings instruments.

Existing Accounts: If an individual opened a PPF account while residing in India and later became an NRI, they can continue to maintain the account until its maturity.However, they are not allowed to extend the account beyond the initial 15-year term.

Interest Rates and Taxation: The interest earned on PPF accounts remains tax-free in India, regardless of the account holder’s residential status.However, NRIs should be aware of potential tax implications in their country of residence, as some countries may tax foreign income.

Can NRIs Invest in Indian Post Office Schemes?

Let’s break this down into the most popular ones.

PPF (Public Provident Fund) for NRIs

A lot of NRIs have PPF accounts that they opened while they were in India. So what happens now?

- If you opened a PPF before becoming an NRI, you can continue it until maturity (15 years).

- But you can’t extend it beyond 15 years—even in 5-year blocks.

- You can continue making deposits during that period and earn interest.

- But... fresh accounts cannot be opened once you're an NRI.

I had a friend who moved to Dubai. He kept depositing into his old PPF, thinking everything was fine. But once he asked his bank, they flagged it and told him to stop immediately.

Always best to check.

NSC (National Savings Certificate) for NRIs

Here’s the rule for NSC:

- NRIs cannot invest in NSC anymore.

- But if you had invested before becoming an NRI, you can hold it till maturity.

- Just no new purchases allowed.

So if your NSC was bought when you were in India, you’re safe. Just sit tight and let it mature.

Post Office FD for NRIs

Want to park money in Post Office Fixed Deposits?

Sorry. Not allowed.

Post office FDs are strictly for resident individuals. NRIs are not allowed to:

- Open new FDs

- Renew old FDs

- Transfer funds into them

So even if you're earning in dollars, you can’t lock it in a PO FD.

Are NRIs Allowed to Open a New Post Office Account?

Let’s cut to the chase—No, you can't.

NRIs are not allowed to open any post office savings accounts, PPFs, NSCs, or FDs. That’s directly based on India Post and RBI instructions.

Even if you're in India on a short visit, the rule still applies. Residential status, not physical presence, is what matters.

It’s like owning a Netflix India subscription—you need an Indian address, Indian payment method, and yes, Indian residency status.

FEMA & RBI Guidelines on Post Office Accounts for NRIs

So who decides these rules?

Answer: FEMA (Foreign Exchange Management Act) and RBI (Reserve Bank of India).

FEMA governs foreign investments and banking regulations for NRIs. RBI issues circulars and banking notifications in line with FEMA.

Here’s what they say:

- Only resident Indians can open and maintain post office accounts.

- Once you become an NRI, you're expected to:

- Inform the bank/post office

- Convert your accounts (if eligible)

- Or close them (if required)

FEMA treats an NRI’s investments differently due to the foreign exchange element involved. So it's not just about legality—it's about currency compliance too.

What If You Already Have an Account Before Becoming NRI?

Good question. This is where most people fall into the grey zone.

Let’s say you opened a post office account before you left India. What now?

- You’re not allowed to continue holding the savings account.

- You must close it after becoming an NRI.

- For PPF and NSC, you can hold till maturity but can’t extend or reinvest.

You should ideally update your KYC and submit Form 30C to your post office declaring your change in status. Most people ignore this and keep things running—but that’s risky.

Closure Rules & Deadlines for NRIs

Here’s where things get serious. The closure process is not optional. Let’s break it down by product.

NRI PPF Account Closure Procedure

If your PPF account is nearing maturity, you have two options:

- Let it run its course and withdraw on maturity.

- Withdraw prematurely under specific conditions.

But here’s the catch: If authorities find you’ve continued PPF without eligibility, they may:

- Stop interest payments

- Penalize the account

- Freeze your withdrawal

Don’t wait for a red flag. Visit your bank or post office, declare your NRI status, and follow their closure/settlement steps.

NSC Premature Withdrawal Rules

NSC does not allow premature withdrawal, except in rare situations:

- Death of the holder

- Court order

- Forfeiture

So if you’ve already invested, you’ll need to wait until it matures. But again, no reinvestment allowed after maturity.

Tax Implications & Repatriation Rules for NRI Post Office Accounts

Here’s another big question: What about taxes?

Interest earned on:

- PPF → Tax-free (even for NRIs)

- NSC → Taxable

- Post Office FDs → Taxable

If you're an NRI, you also need to declare:

- Indian income in your tax return (in India)

- Use NRO accounts to receive funds from matured schemes

- Follow RBI repatriation rules to transfer money abroad

A CA once told me, “Many NRIs forget that just because it’s India income doesn’t mean they can hide it. The government tracks PAN-linked investments.”

Always declare interest income, even if tax is minimal.

What Are the Penalties for Non-Compliance?

Think it doesn’t matter?

It does.

Keeping a post office account after becoming an NRI can lead to:

- Account freeze

- Loss of interest

- RBI and FEMA violations

- Possible monetary penalties under FEMA (up to 3x the amount involved)

There have been cases where people got notices years later. Just because no one asked questions at first doesn’t mean you’re off the hook.

Alternatives for NRIs After Post Office Account Closure

So now you’re thinking, If I can’t keep my post office account, then what?

Good news—there are better options for NRIs.

Here are some alternatives:

- NRE/NRO savings accounts: Fully legal, compliant, and tailored for NRIs.

- NRE Fixed Deposits: Tax-free interest. Good for sending money from abroad.

- FCNR Deposits: Maintain deposits in foreign currency. No conversion risk.

- Mutual Funds via NRO/NRE: Invest in equity, debt, hybrid—just check if AMC accepts NRI applications (especially from US/Canada).

I personally shifted all my investments to NRE FDs once I moved abroad. It was simple, transparent, and most importantly—legal.

Alternative Investment Options for NRIs

While NRIs cannot invest in Post Office schemes, they have access to other investment avenues in India, such as:

- National Pension System (NPS): NRIs can invest in NPS, which offers retirement benefits.

- Equity Market and Mutual Funds: NRIs can invest in Indian equities and mutual funds, subject to certain regulations

- Fixed Deposits: NRIs can open Non-Resident External (NRE) or Non-Resident Ordinary (NRO) fixed deposit accounts with Indian banks

- Real Estate: NRIs can invest in residential and commercial properties in India, though there are restrictions on agricultural land

It’s advisable for NRIs to consult with financial advisors or legal experts to understand the regulations and tax implications associated with these investment options.

FAQs

Can NRI open a post office account?

No. NRIs are not eligible to open any India Post account as per new rules.

What happens if I don’t close my savings account after becoming an NRI?

Your account may be frozen, interest may be denied, and you could face FEMA penalties.

Can NRIs hold NSC till maturity?

Yes, if it was purchased before NRI status. No fresh investments are allowed.

Can NRI invest in PPF now?

No. Only continuation of existing PPF (opened before becoming NRI) is allowed till maturity.

Can I repatriate funds from a closed post office account?

Yes, via your NRO account, following RBI’s repatriation limits and documentation.

Are there tax benefits for NRI post office investments?

PPF remains tax-free. Others like NSC and FDs are taxable under Indian laws.

Final Thoughts: What Should NRIs Do?

Here’s the takeaway.

If you’re an NRI—or becoming one soon—you must review all your post office investments. Don’t wait. Don’t assume.

- Close ineligible accounts.

- Continue what’s allowed—like old PPF or NSC—until maturity.

- Never make new investments unless rules clearly permit it.

It’s not about being cautious. It’s about being compliant.

If you’re still unsure, talk to a compliance consultant or CA familiar with NRI regulations. The laws may look harmless now, but the consequences show up years later.

0 Comments