Filing taxes in the U.S. is confusing enough. Now imagine doing it from another country. The forms are different. The rules are different. And a simple mistake can lead to letters from the IRS.

If you are a non-resident alien with income from the United States, you have probably heard of Form 1040-NR. This is not the regular 1040 form that U.S. citizens use. This is your form.

This guide will walk you through everything you need to know. We will explain what the form is, who must file it, and how to fill it out step by step. We will break down its complicated schedules and deadlines. Let us demystify the 1040-NR together.

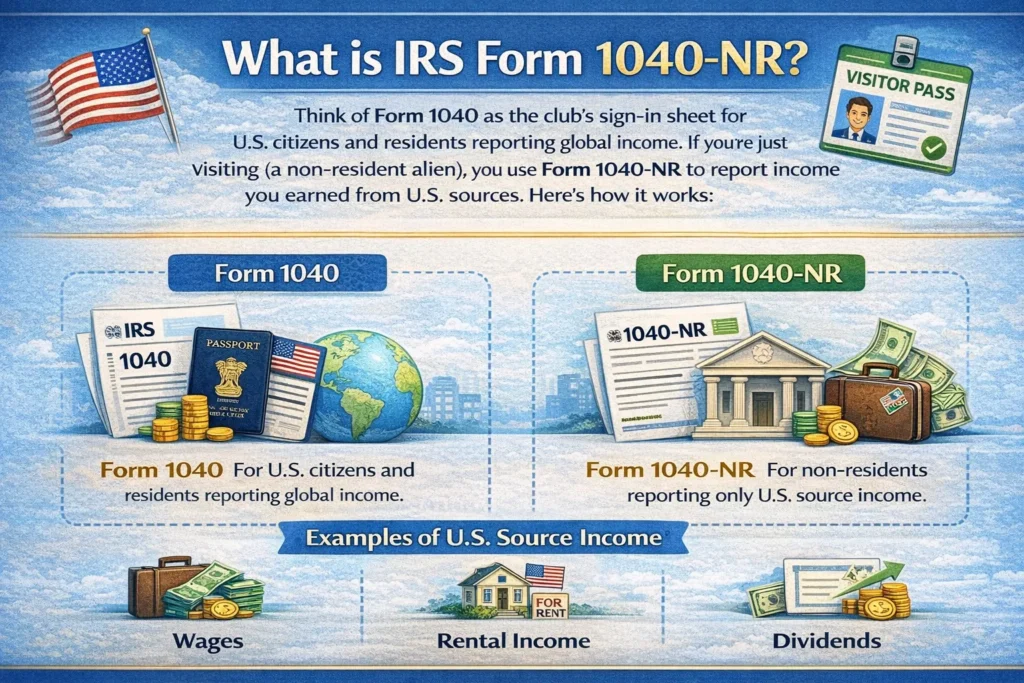

What is IRS Form 1040-NR?

Think of the United States tax system as an exclusive club. If you are a member (a U.S. citizen or resident), you use Form 1040 to tell the club about all the money you made, no matter where in the world you earned it.

But if you are just a visitor to the club (a non-resident alien), you use a different form. You use IRS Form 1040-NR. This form has one main job: to report the income you earned from within the United States.

The IRS does not tax non-resident aliens on their worldwide income. It only cares about the money connected to the U.S. This includes things like wages from a U.S. company, rental income from a U.S. property, or dividends from U.S. stocks.

In simple terms:

- Form 1040: For U.S. citizens and residents reporting global income.

- Form 1040-NR: For non-residents reporting only U.S.-source income.

This form is crucial for many people. International students on F-1 or J-1 visas use it. Non-Resident Indians (NRIs) with U.S. investments use it. Even professionals on H-1B or L-1 visas who have left the U.S. but still have American income need to file it.

You can always find the official Form 1040-NR PDF directly on the IRS website.

Who Must File Form 1040-NR?

This is the most important question. Filing this form when you do not have to is a waste of time. But not filing it when you are required to can lead to penalties and interest.

You generally must file a Form 1040-NR if you are a non-resident alien and any of the following are true:

- You engaged in a trade or business in the United States during the tax year.

- You have U.S. source income that is subject to income tax, even if no tax was withheld.

- You have to file a return for a special reason, like to claim a refund of overwithheld tax.

Let us put this into real world scenarios. You probably need to file a 1040-NR if you are:

- An international student who worked an on-campus job or received a taxable scholarship. Your university likely gave you a W-2 form.

- A non-resident alien who earned rental income from a property you own in Florida or New York.

- An NRI investor who sold U.S. stocks and had capital gains.

- A researcher or professional who earned honoraria for a speech or consultation in the U.S.

- Anyone who did not pass the Substantial Presence Test and has any of the income types mentioned above.

The Substantial Presence Test is the IRS’s method for determining your residency for tax purposes. If you do not meet this test, you are considered a non-resident alien and likely need the 1040-NR.

1040 vs 1040-NR: Key Differences

It is easy to get these two forms mixed up. Using the wrong one is a very common mistake. Here is a clear breakdown of the main differences.

| Feature | Form 1040 (For Residents) | Form 1040-NR (For Non-Residents) |

|---|---|---|

| Income Reporting | Reports worldwide income. | Reports only U.S.-source income. |

| Filing Status | Can file as “Married Filing Jointly.” | Cannot typically file jointly with a non-resident spouse. |

| Standard Deduction | Eligible for a standard deduction. | Generally not eligible for the standard deduction. |

| Tax Treaties | Treaty claims are less common. | Heavily relies on tax treaties to lower tax rates. |

| Key Schedules | Uses Schedules A, B, C, D, etc. | Uses Schedule OI and Schedule NEC. |

The biggest takeaway? Your global income is safe. You only need to report and pay U.S. tax on what you earned from American sources. And you cannot use the same filing statuses or deductions as your U.S. resident friends.

Important Schedules: OI and NEC

The main 1040-NR form is just the beginning. It comes with two special sidekicks that confuse many people: Schedule OI and Schedule NEC. Think of them as mandatory questionnaires that give the IRS the specific details it needs to process your return correctly.

Schedule OI (Other Information)

Schedule OI is the IRS’s background check. Its purpose is to collect information about your personal situation that affects your tax liability.

This schedule asks questions like:

- What type of visa do you hold? (F-1, J-1, H-1B, etc.)

- Did you enter the U.S. under a tax treaty?

- What country are you a resident of for tax purposes?

- Are you claiming a tax treaty benefit that exempts your income?

Filling this out is not optional. It is required for almost everyone filing a 1040-NR. It is how you formally tell the IRS, “I am a student from India under the U.S.-India tax treaty, and I am claiming an exemption for my scholarship.” Without Schedule OI, the IRS has no context for your return.

Schedule NEC (Tax on Income Not Effectively Connected With a U.S. Trade or Business)

Schedule NEC has a very specific job. It reports a category of income called Fixed, Determinable, Annual, Periodical (FDAP) income. That is a mouthful, so let us simplify.

FDAP income is typically passive income. Think dividends from U.S. companies, interest from U.S. bank accounts, or royalties from a patent.

Here is the key part: this type of income is usually taxed at a flat 30% rate. No questions asked.

But there is a way to lower that rate. This is where tax treaties come in. For example, the U.S.-India tax treaty might reduce the tax on dividend income from 30% to 15% or even 10%. You use Schedule NEC to report the income and to claim that lower treaty rate.

So, if you are an NRI earning dividends from Google stock, you would report that on Schedule NEC and use the treaty to pay less tax.

How to Fill IRS Form 1040-NR: Step by Step

The official instructions can feel like reading a legal textbook. Let us break it down into a clear, actionable process.

Step 1: Gather Your Documents

Before you touch the form, get all your papers in one place. You will need:

- Your W-2 forms from U.S. employers.

- Your 1042-S forms for scholarship or fellowship income.

- Any 1099 forms for interest or dividends.

- Your passport and visa information.

- Your U.S. Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

Step 2: Determine Your Residency Status

Be 100% sure you are a non-resident alien. Use the IRS Substantial Presence Test. If you are filing a 1040-NR, you must have failed this test. If you are unsure, double check. This is the most critical step.

Step 3: Fill Out Personal Information

This is the easy part. Carefully enter your name, address, SSN/ITIN, and filing status. For non-residents, your status will almost always be “Single,” even if you are married, unless your spouse is a U.S. resident.

Step 4: Report Your U.S. Source Income

Go through your documents and transfer the numbers to the correct lines on the 1040-NR. W-2 wages go on line 1. Taxable scholarship income from a 1042-S goes on line 1h. Be meticulous.

Step 5: Claim Your Treaty Benefits

This is where you save money. If your home country has a tax treaty with the U.S., use it. For instance, an Indian student can often claim an exemption for their scholarship under Article 21 of the U.S.-India treaty. You will note this on Schedule OI and often attach a written statement.

Step 6: Complete Schedule OI and NEC

Now, fill out the two key schedules we discussed. Schedule OI for your personal and treaty information. Schedule NEC for any passive income like dividends or interest.

Step 7: Calculate Your Tax Liability

Use the IRS tax tables for non-residents to calculate how much tax you owe. Remember to apply any reduced treaty rates from Schedule NEC. The form will walk you through adding everything up and comparing it to what was already withheld.

Step 8: Sign and File Your Return

A tax return without a signature is invalid. Sign and date it. Then, you can e-file it using approved software or mail it to the IRS address for non-resident filers, which is typically in Austin, Texas.

Filing Deadlines for 1040-NR (2025)

Mark your calendar. The deadlines are strict, but they are different depending on your situation.

| Category | Deadline |

|---|---|

| Non-residents with W-2 income | April 15, 2025 |

| Non-residents without W-2 income | June 15, 2025 |

| Extension Request (Form 4868) | October 15, 2025 |

A key point: if you are a non-resident and do not have wages subject to U.S. tax withholding (like a W-2), you get an automatic two-month extension to June 15. But if you owe tax, interest will still accrue from the original April 15 date.

If you need more time, you can file Form 4868 to get an extension until October 15, 2025. This is an extension to file, not an extension to pay. You must estimate and pay any tax you owe by the original deadline to avoid penalties.

Where and How to File Form 1040-NR

You have two main options for sending your return to the IRS.

E-Filing is the fastest, safest, and most recommended method. It reduces errors and gives you confirmation that the IRS received your return. However, not all tax software supports 1040-NR e-filing for everyone. You may need to use a platform specifically designed for non-residents.

Paper Filing is the traditional method. You print the forms, attach all your documents like your W-2 and 1042-S, sign them, and mail them to the IRS. The mailing address for most non-resident alien tax returns is: Department of the Treasury Internal Revenue Service Austin, TX 73301-0215 USA

Always double-check the IRS website for the most current mailing address before you send anything.

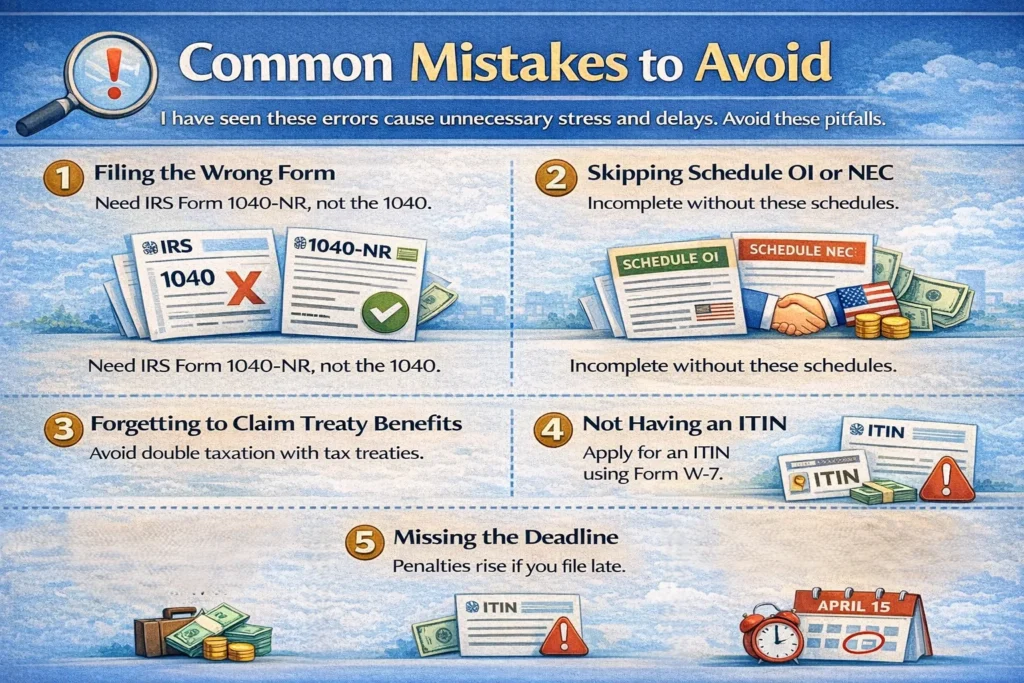

Common Mistakes to Avoid

I have seen these errors cause unnecessary stress and delays. Avoid these pitfalls.

- Filing the Wrong Form: Do not accidentally file the standard 1040. It is for residents. You need the 1040-NR.

- Skipping Schedule OI or NEC: These are not optional. Your return will be considered incomplete without them.

- Forgetting to Claim Treaty Benefits: This is like leaving money on the table. The treaties exist to prevent double taxation. Use them.

- Not Having an ITIN: If you do not have an SSN and need to file a tax return, you must apply for an ITIN using Form W-7. Do this well before the tax deadline.

- Missing the Deadline: Even if you cannot pay all the tax you owe, file the return. The penalty for late filing is much higher than the penalty for late payment.

FAQs About IRS Form 1040-NR

What is Form 1040-NR used for?

Form 1040-NR is used by non-resident aliens to report their U.S. source income to the Internal Revenue Service. It is the non-resident version of the standard Form 1040.

Who needs to file a 1040-NR?

Any non-resident alien who engaged in a U.S. trade or business or has U.S. source income that is subject to tax must file this form. This includes international students, NRIs with U.S. income, and foreign investors.

Can NRIs claim the standard deduction?

Generally, no. Non-resident aliens are not eligible for the standard deduction on Form 1040-NR. However, students from India may be able to claim a standard deduction under the U.S.-India tax treaty, which is a special exception.

What is the difference between Schedule OI and Schedule NEC?

Schedule OI collects your personal, visa, and treaty information. Schedule NEC is used to report specific types of passive income like dividends and interest, which are taxed at a flat 30% rate unless a tax treaty lowers it.

When is the Form 1040-NR deadline for 2025?

The deadline is April 15, 2025, for those with W-2 income and June 15, 2025, for those without. An extension can push the final deadline to October 15, 2025.

Can you e-file Form 1040-NR?

Yes, e-filing is possible and encouraged through certain IRS-approved software providers that support non-resident returns. It is the most efficient way to file.

What happens if I file my 1040-NR late?

Filing late can result in a failure-to-file penalty. This penalty is typically 5% of the unpaid taxes for each month your return is late, up to a maximum of 25%. It is always better to file on time, even if you cannot pay the full amount immediately.

0 Comments