TDS Rules for NRIs When Selling Property in India

The sale of property in India by Non-Resident Indians (NRIs) is subject to several tax implications, with Tax Deducted at Source (TDS) being one of the most significant. Understanding these rules is essential for NRIs to ensure compliance and avoid any legal issues. Let’s dive into a comprehensive guide on TDS rules for NRIs when selling property in India.

Understanding TDS:

Tax Deducted at Source (TDS) is a mechanism of collecting income tax in India. Under this system, the payer (the buyer of the property) deducts a certain percentage of the payment and remits it to the government on behalf of the payee (the NRI seller). This ensures that tax is collected at the source of income, making the process transparent and straightforward.

TDS Rates for NRIs:

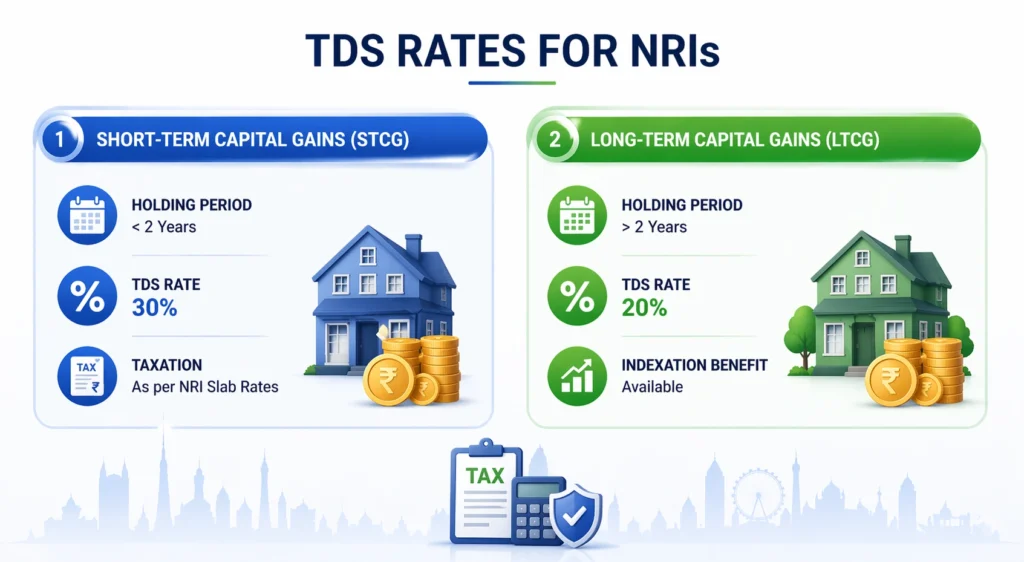

1. Short-Term Capital Gains (STCG):

-

- Definition: If the property is held for less than two years before selling, it is classified as a short-term capital asset.

- TDS Rate: The applicable TDS rate for short-term capital gains is 30% of the sale consideration. This rate may be higher when including surcharge and cess.

- Taxation: The gains are taxed at the applicable slab rates for NRIs, which might result in a higher overall tax liability.

2. Long-Term Capital Gains (LTCG):

-

- Definition: If the property is held for more than two years before selling, it is classified as a long-term capital asset.

- TDS Rate: The applicable TDS rate for long-term capital gains is 20% of the sale consideration, plus applicable surcharge and cess.

- Indexation Benefit: Long-term capital gains can benefit from indexation, which adjusts the purchase price for inflation, potentially reducing the taxable amount.

Role of the Buyer in TDS Deduction:

The buyer of the property is responsible for deducting TDS and depositing it with the Indian government. Here are the steps involved:

-

- Obtain TAN: The buyer must obtain a Tax Deduction and Collection Account Number (TAN) to deduct TDS. This number is required to remit TDS to the government.

- Deduct TDS: The buyer should deduct TDS at the applicable rate (30% for STCG or 20% for LTCG) from the sale consideration at the time of making the payment to the NRI seller.

- Deposit TDS: The deducted TDS must be deposited with the Income Tax Department using Form 26QB. This deposit should be made within 30 days from the end of the month in which the TDS was deducted.

- Issue TDS Certificate: After depositing the TDS, the buyer should issue a TDS certificate (Form 16A) to the NRI seller within 15 days of depositing the TDS. This certificate is proof of the TDS deduction.

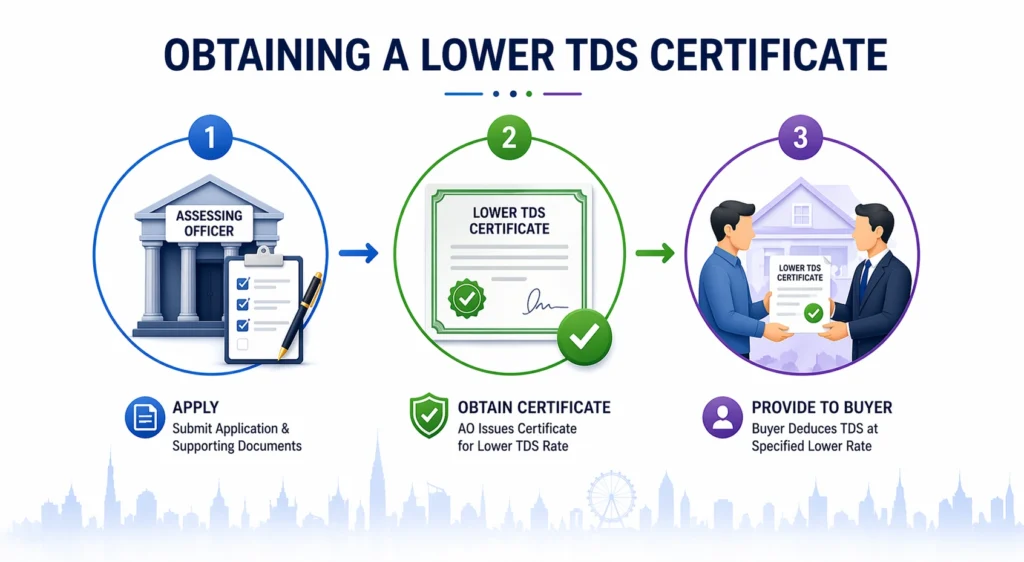

Obtaining a Lower TDS Certificate:

NRIs can apply for a lower TDS certificate if they believe that their overall tax liability is lower than the TDS being deducted. Here’s how they can do it:

- Apply to the Assessing Officer: Submit an application to the assessing officer in India, along with supporting documents such as the sale agreement, purchase details, and computation of capital gains.

- Obtain Certificate: If approved, the assessing officer will issue a certificate specifying a lower TDS rate. This certificate reduces the burden of upfront tax deduction.

- Provide to Buyer: Submit the lower TDS certificate to the buyer, who will then deduct TDS at the specified lower rate. This ensures compliance with the reduced TDS requirement.

Repatriation of Sale Proceeds:

NRIs can repatriate the sale proceeds of a property to their home country, subject to certain conditions:- Certificate from Chartered Accountant: Obtain a certificate in Form 15CB from a chartered accountant. This certificate verifies that taxes have been duly paid and compliance with Indian tax laws has been maintained.

- Submit Form 15CA: Upload Form 15CA online on the Income Tax Department’s website, along with the Form 15CB certificate. This step ensures proper documentation of the repatriation process.

- Bank Approval: Submit the forms and required documents to the bank for approval. The bank will facilitate the repatriation process, allowing the NRI to transfer the sale proceeds to their home country.

Conclusion:

Understanding TDS rules is essential for NRIs to ensure compliance and avoid penalties when selling property in India. By being aware of the applicable TDS rates, the role of the buyer, and the process for obtaining a lower TDS certificate, NRIs can smoothly navigate the sale process. Additionally, ensuring proper documentation and compliance with repatriation norms will help in transferring the sale proceeds to their home country without any issues.

0 Comments