If you work outside a traditional job, chances are you’ve come across the term Form 1099. Maybe you’ve heard it mentioned but never really knew what it meant or why it matters. Or maybe you received one and wondered what to do next. Either way, this guide will break it down simply. You’ll learn what a 1099 form is, who should get one, the common types, and how it affects your taxes.

Think of a 1099 form as a way the IRS keeps tabs on income that isn’t part of a regular paycheck. It helps make sure everyone reports the money they earn, no matter how or where they earn it.

Let’s unpack it all, step by step.

What Is a 1099 Form?

Imagine you do some freelance work, sell investments, or rent out a room. The money you get doesn’t come from an employer who withholds taxes each paycheck. Instead, it’s income from other sources. A Form 1099 reports this kind of income to the IRS.

It’s different from a W-2, which tracks wages and salaries. The W-2 comes from your employer and already includes taxes taken out. But a 1099 shows money paid to you without taxes withheld upfront. This means you’re responsible for reporting it and paying taxes later.

The IRS uses the 1099 to ensure people pay taxes on all income — not just paychecks. So if you get a 1099, it means the IRS knows someone paid you money, and they expect you to report it when you file your tax return.

Why Does the IRS Use Form 1099?

Think of the IRS as a watchdog making sure no income slips through the cracks. When you work a job, taxes get taken out automatically. But when you earn money as a freelancer, investor, or from other sources, that money might fly under the IRS’s radar.

Form 1099 creates a paper trail. It tells the IRS, “Hey, this person got paid this amount.” Businesses and financial institutions file 1099s when they pay people or entities above certain amounts.

This system helps keep everything fair. Everyone pays their share. The IRS matches the income you report on your tax return against the 1099s they receive. If there’s a mismatch, it raises a flag.

In short, 1099s keep the tax system honest.

Who Receives a 1099?

If you’re wondering, “Am I going to get a 1099?” the answer depends on the money you made and who paid you.

Most often, 1099s go to:

- Freelancers and contractors: If you did work for a business and got paid $600 or more, you’ll probably get a 1099-NEC.

- Investors: Dividends and interest you earned might be reported on 1099-DIV or 1099-INT.

- Landlords: Rental income over $600 can trigger a 1099-MISC.

- Winners of prizes or awards: If you won something with cash value, a 1099 might be coming your way.

- Businesses paying for services outside traditional employment: They have to report certain payments to keep things transparent.

If you earned money but didn’t get a 1099, you still have to report the income. The form is a tool for the IRS, but it doesn’t replace your responsibility to file accurately.

Common Types of 1099 Forms

Form 1099 isn’t just one form. The IRS has many versions, each tracking different income. Here’s a quick look at the most common ones you’ll see:

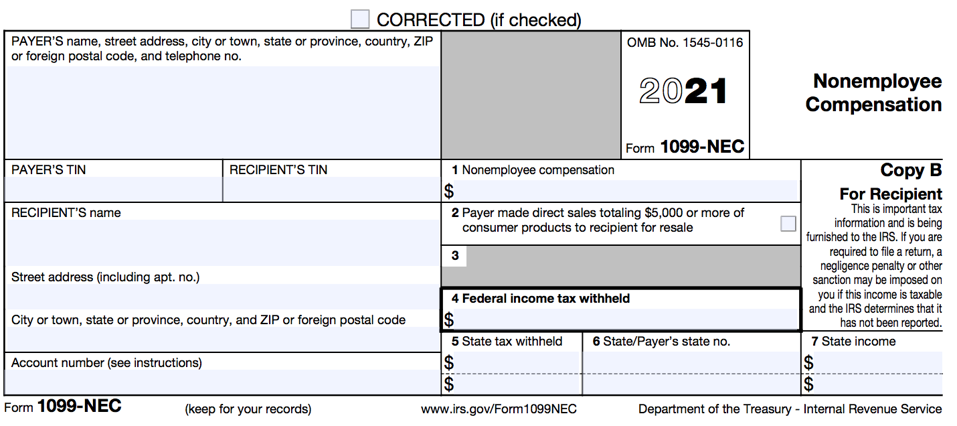

1099-NEC: Nonemployee Compensation

This one’s all about freelancers, contractors, and gig workers. If a business pays you $600 or more for services, they send you this form. It shows how much you earned as a non-employee.

1099-MISC: Miscellaneous Income

This is a catch-all form. It reports income like rent, royalties, prizes, awards, and some other payments not covered by 1099-NEC. For example, if you rented a property and earned over $600, you might get a 1099-MISC.

1099-INT: Interest Income

Earned interest from your bank account, bonds, or other investments gets reported here. It helps you track income from your savings or investments.

1099-DIV: Dividends & Distributions

If you own stocks or mutual funds, dividends paid to you come on this form. It also reports capital gains distributions.

1099-K: Payment Card & Third-Party Network Transactions

Have you sold things online or taken payments via platforms like PayPal? If you process more than a threshold amount (usually $600 or $5,000, depending on rules), you’ll get a 1099-K. This form tracks transactions made through cards or third-party networks.

Other Important 1099s

There are plenty more 1099 variations, such as:

- 1099-R: For retirement plan distributions

- 1099-B: For brokerage transactions

- 1099-S: For real estate transactions

Each covers specific income types and has its own reporting rules.

How Does a 1099 Work?

Here’s a simple way to think about it: If someone pays you and the IRS needs to know about it, they fill out a 1099 form. They send a copy to you and the IRS.

When you file your tax return, you use the information from the 1099 to report your income. The IRS uses their copy to cross-check your return.

If you earned $10,000 freelancing, but only report $5,000, the IRS will notice the difference. This can trigger questions or audits.

That’s why keeping good records is important. It also helps if you think a 1099 form is wrong or missing.

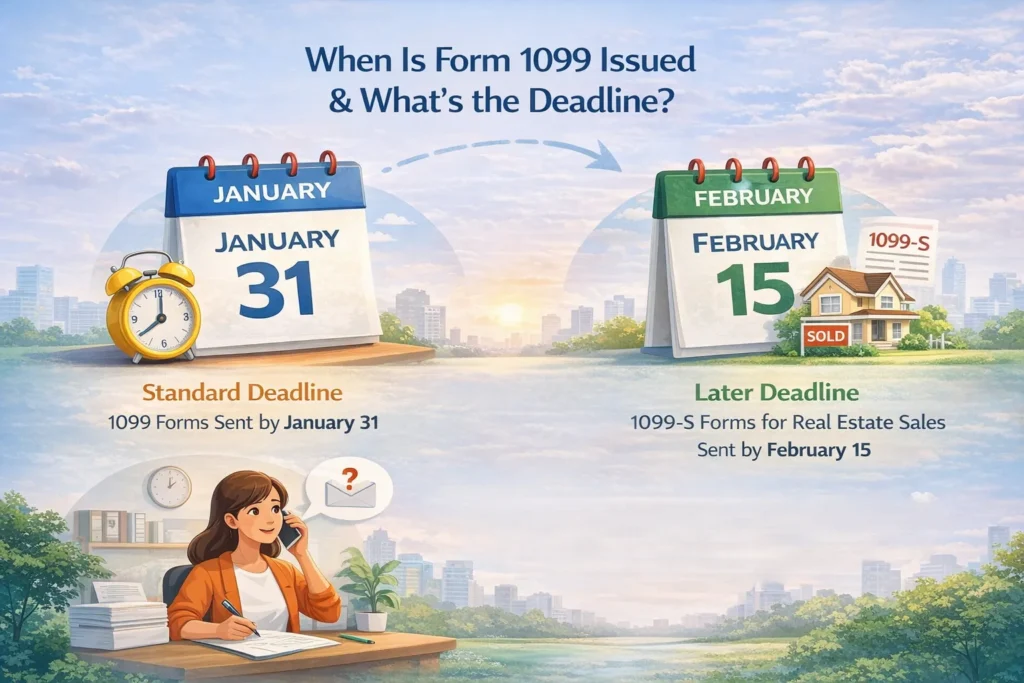

When Is Form 1099 Issued & What’s the Deadline?

Timing matters. Payers must send 1099 forms to recipients and the IRS by January 31 after the tax year ends. This gives you plenty of time to prepare your taxes.

Some forms, like 1099-S for real estate sales, have a later deadline, usually February 15.

If you don’t get your form by early February, check in with the payer. It might be lost in the mail or sent electronically. Keeping your address updated helps prevent delays.

Filing & Reporting 1099 Income on Your Tax Return

Receiving a 1099 means you have income to report. But how you report it depends on the form and your situation.

- 1099-NEC income: Usually reported on Schedule C as business income. You may owe self-employment tax on this.

- 1099-INT and 1099-DIV income: Go on Schedule B or directly on Form 1040 for interest and dividends.

- Other 1099 income: Can go on different forms depending on what it is — rental income, retirement distributions, and so forth.

Pay close attention to the numbers on your 1099. They should match what you put on your tax return.

If they don’t, you risk penalties or audits.

Common FAQs About Form 1099

What if I don’t receive a 1099 but earned income?

Not getting a 1099 doesn’t mean you don’t owe taxes. The IRS expects you to report all income, regardless of whether you receive a form. Use your bank records, invoices, or payment histories to track what you earned.

If a 1099 is missing, contact the payer early in the year. Keep notes on your communication in case you need to explain later.

Do I need to pay taxes on 1099 income?

Most 1099 income is taxable. Since taxes aren’t withheld upfront, you’ll need to set aside money and possibly pay quarterly estimated taxes. Self-employment income also includes Social Security and Medicare taxes, which add to your bill.

What’s the difference between a W-2 and a 1099?

A W-2 is for employees. Taxes get taken out before you see the money. Your employer sends it.

A 1099 is for income earned outside employment. Taxes usually aren’t withheld. You’re responsible for reporting and paying taxes yourself.

Tips for Businesses Issuing 1099s

If you run a business, here’s what you should keep in mind when issuing 1099s:

- Get Form W-9 from contractors to collect correct tax info.

- Track payments throughout the year to know who crosses the $600 threshold.

- File 1099s on time — late forms can mean fines.

- Consider filing electronically if you have many forms to submit.

- Keep clear communication with payees so they know what to expect.

Conclusion

Form 1099 is a key part of tax reporting for anyone earning income outside a regular job. It keeps the tax system fair and transparent. If you get one, it means you need to report that income on your tax return.

Mistakes happen, but you can avoid penalties by staying organized and proactive. Keep good records, ask for missing forms, and reach out to tax professionals if you’re unsure.

Here’s what you can do now:

- Keep all payment records and invoices.

- Watch out for your 1099 forms after January 31.

- Report all income on your tax return, even if you don’t get a form.

- Download our free “1099 Types & Deadlines” cheat sheet to stay on track.

- Use a tax calculator to estimate what you owe.

- Need guidance? Talk to a tax expert who can help you navigate the process.

0 Comments