Imagine this. You’ve filed your income tax return. You feel good about claiming deductions, including a neat one under Section 80GGC for your political donation. And then… a few weeks later… an email drops in.

It’s from the Income Tax Department. Notice issued. Mismatch in 80GGC claim. Suddenly, the relief of saving tax is replaced with confusion and worry.

If this sounds familiar, you’re not alone. Section 80GGC is one of those areas where a simple mistake can quickly attract scrutiny. And with political donations under the scanner more than ever, it’s crucial to get it right.

This guide will walk you through everything:

- The difference between 80GGA and 80GGC (a common confusion).

- What the 80GGC deduction really means.

- Whether NRIs can claim 80GGC.

- Why are notices for political donations increasing?

- What to do if your 80GGC claim is disallowed.

- And most importantly, how to avoid these mistakes in the first place.

Think of this as your one-stop explainer. By the end, you’ll know exactly what’s allowed, what’s risky, and how to respond if the taxman comes knocking.

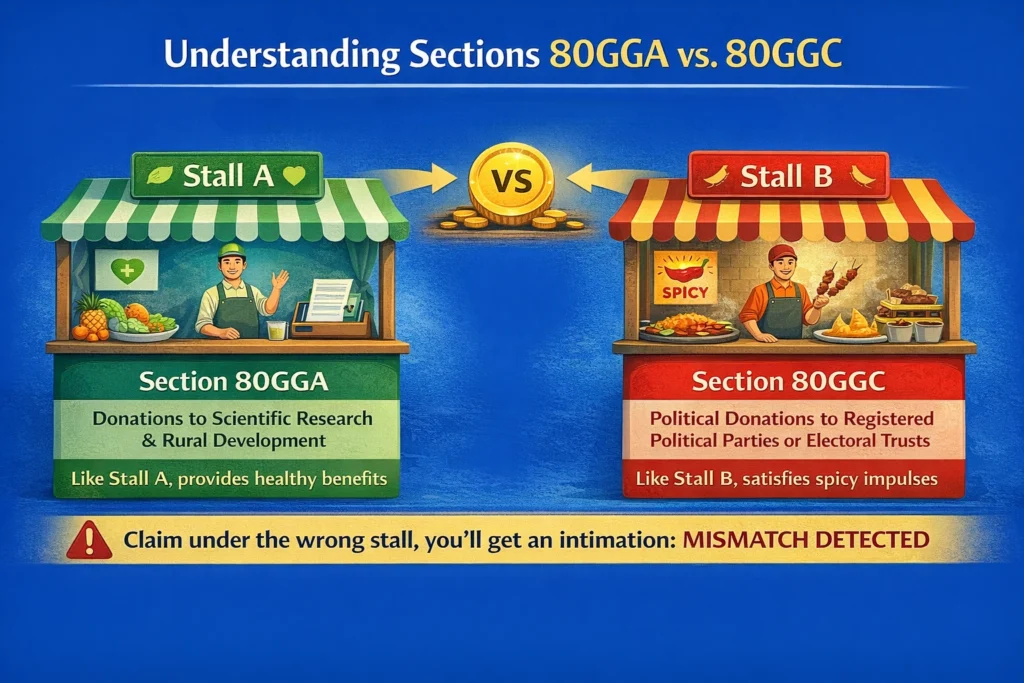

Understanding Sections 80GGA vs. 80GGC

Let’s start with a common mix-up that often occurs. Many taxpayers confuse 80GGA with 80GGC. They look similar, but they’re completely different.

- Section 80GGA is about donations to scientific research or rural development. Think of contributing to innovation or helping rural projects.

- Section 80GGC is about political donations. It gives you a 100% deduction for contributions to registered political parties or electoral trusts.

Here’s a simple analogy. Imagine you’re at a food court. Stall A sells healthy food. Stall B sells spicy street food. Both take your money, but they serve very different purposes. That’s 80GGA and 80GGC in a nutshell. They’re both “donation deductions,” but to totally different stalls.

The problem? If you claim under the wrong stall, the Income Tax Department is quick to notice. And they won’t hesitate to send you an intimation saying, “Mismatch detected.”

What is the 80GGC Deduction?

Alright, let’s zoom in on Section 80GGC. What exactly is it?

In simple words: 80GGC lets you deduct the full amount you donate to a political party or electoral trust from your taxable income. It’s a 100% deduction. Sounds generous, right? But there are conditions. And they’re strict.

- No cash allowed. Donations must be made electronically. That means cheque, bank transfer, debit card, credit card, or UPI.

- Only to registered entities. The political party has to be registered under Section 29A of the Representation of the People Act, 1951.

- Available only under the old tax regime. If you’ve switched to the new regime, you can’t claim it.

Think of it like this. It’s like using a discount coupon at a store. The coupon gives you 100% off. But it only works if you buy from the right shop, swipe your card, and shop on the valid date. Miss any condition, and the cashier simply says, “Sorry, not valid.”

That’s how 80GGC works. Follow the rules exactly, and you get the deduction. Slip up, and you invite trouble.

Can an NRI Claim Deduction 80GGC?

This is where it gets interesting. Yes, NRIs can claim 80GGC deduction. But again, conditions matter.

If you’re an NRI and you donate to a registered Indian political party or electoral trust, and you do it electronically, you’re eligible. The law doesn’t exclude you.

But here’s the catch. NRIs are often under higher scrutiny. Why? Because your donations flow from foreign accounts, foreign exchanges, and sometimes even via intermediaries. This makes the Income Tax Department extra alert.

I remember chatting with a friend who lives in Dubai. He donated ₹50,000 to a major Indian political party. All legal, all electronic. Yet, he still got a notice. Why? The IT department wanted to cross-check whether the party was registered and whether his payment was directly from his NRO account.

So yes, as an NRI you can claim it. But expect questions if something doesn’t match neatly in their database.

The Rising Scrutiny: Income Tax Notice for Political Donation

Over the past few years, political donations have been in the spotlight. With electoral bonds and donation transparency debates, the government has tightened its watch.

That’s why many taxpayers, including NRIs, are receiving IT notices under Section 143(1). This is basically a mismatch alert. The department’s system compares your claim with the data reported by political parties. If there’s a difference, it sends you an intimation.

Common reasons?

- You donated in cash (not allowed).

- You donated to an unregistered or unrecognized party.

- You claimed a deduction without valid proof.

- The donation amount you claimed in your return doesn’t match what the party reported.

- Or you simply exceeded your total income.

Picture it like airport security. If your bag doesn’t match the scanner image, they’ll pull you aside. Doesn’t always mean you did something wrong. But it does mean you need to explain.

Fraudulent Parties and the Cash-Back Trap

One of the biggest reasons the Income Tax Department has stepped up scrutiny is the cash-back scam. Here’s how it usually works:

You “donate” money to a small or unknown political party. On paper, it looks like a clean digital donation, eligible under Section 80GGC. The party gives you an official-looking receipt. But behind the scenes, they quietly hand most of that money back to you in cash — often after deducting a commission.

So you get:

- A receipt for a large political donation.

- A 100% deduction under Section 80GGC in your tax return.

- And your cash safely returned, minus a small cut.

On the surface, it looks like a win-win. In reality, it’s a serious tax offence.

The IT Department calls these “accommodation entries.” And they’re cracking down hard. In fact, Registered Unrecognized Political Parties (RUPPs) have been under intense investigation precisely for this practice. Many of them exist only on paper to launder money back to donors.

Here’s the risk if you fall into this trap:

- The deduction will be disallowed the moment the party’s books are scrutinized.

- You’ll face a 200% penalty for misreporting under Section 270A.

- The donation can be treated as bogus expenditure, opening the door for prosecution.

- If you accepted the cash back, you’re also in violation of the Benami Transactions Act.

I once met a businessman in Pune who thought he was being clever by “donating” ₹5 lakh to a little-known outfit. He proudly claimed the deduction and pocketed ₹4.5 lakh back in cash. A year later, the party’s accounts were audited. His name popped up. He ended up paying double the tax saved, penalties, and faced months of legal harassment.

The lesson? If a deal looks too good to be true, it usually is.

Always donate only to well-known, registered parties. If someone offers you cash back, walk away. That’s not tax planning. That’s fraud.

What to Do if Your 80GGC Claim is Disallowed or You Receive a Notice

So what happens if you’re one of the unlucky ones who gets the dreaded notice? First, don’t panic. Many notices are just intimations, not accusations.

Here’s how to handle it step by step:

- Stay calm. The first notice is usually just asking for clarification.

- Collect your proof. Pull out your political donation receipt. It should clearly show the party’s name, PAN, address, registration number, and your donation details.

- Check the party’s registration. Go to the Election Commission of India’s website. Confirm that the party was indeed registered at the time of your donation.

- Respond online. Log in to the income tax portal. Go to “Pending Actions” or “e-Proceedings.” Upload your receipt and give a written explanation.

- File an ITR-U if needed. If you realize you actually made a wrong claim—say you donated to a party that wasn’t registered—own up early. File an updated return (ITR-U). Yes, you’ll pay extra tax. But it’s better than facing penalties.

Here’s a personal anecdote. A client of mine once claimed 80GGC for a ₹1 lakh donation. The party turned out to be an unregistered one. He got a notice. Instead of fighting, he filed an ITR-U, paid the extra tax and a small fee. He avoided a penalty that could have been ₹2 lakh. His relief was worth every rupee.

Important: Ignoring the notice is the worst move. That’s how you end up with a full scrutiny assessment under Section 143(2). And penalties under Section 270A can go up to 200% of the tax. In severe cases, even prosecution is possible. Don’t let it get that far.

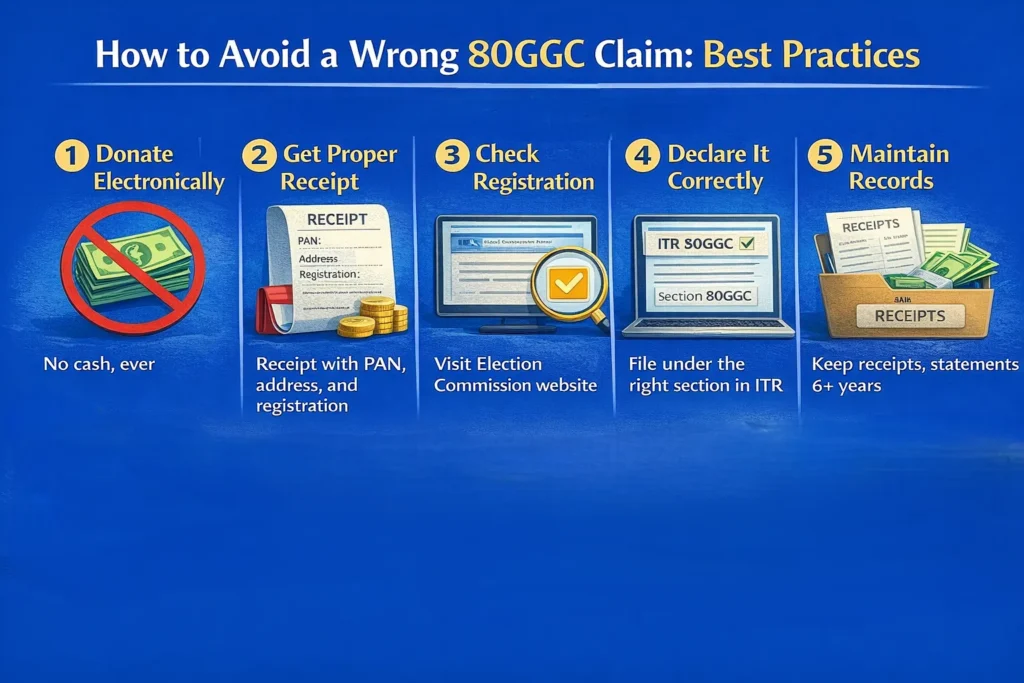

How to Avoid a Wrong 80GGC Claim: Best Practices

Like they say, prevention is better than cure. Avoiding a notice is far easier than dealing with one.

Here are best practices:

- Always donate electronically. No cash, ever.

- Insist on a proper receipt. Don’t just rely on an acknowledgment SMS. Get a receipt with the party’s PAN, address, and registration number.

- Double-check registration. Spend 2 minutes on the Election Commission website before donating.

- Declare it correctly. File the deduction under the right section in your ITR.

- Maintain records. Keep receipts and bank statements for at least six years.

Think of it like driving. If you follow traffic rules—seatbelt, signals, speed limit—you’re less likely to get pulled over. Same with tax compliance.

Penalties and Consequences of Wrong 80GGC Claims

Let’s get real about the risks. If your wrong claim goes uncorrected, penalties can be steep.

- 200% penalty: For under-reporting or misreporting of income under Section 270A.

- Interest charges: Extra tax owed comes with interest, often 1% per month.

- Prosecution: In extreme cases of deliberate fraud, criminal proceedings can start.

Example: Suppose you falsely claimed ₹50,000 under 80GGC. The IT Department disallows it. Tax payable rises by, say, ₹15,000. The penalty could then be ₹30,000—double the misreported tax. Suddenly, your small “saving” costs you way more.

That’s why it’s always smarter to correct early rather than wait.

Real-World Example: How a Wrong Claim Played Out

A colleague once shared a story about his uncle in Canada. He proudly donated ₹2 lakh to a political outfit in India and claimed 80GGC. But he missed two details: the outfit wasn’t registered, and he paid in cash while visiting India.

Months later, he got a notice. He panicked, ignored it, and thought it would “go away.” It didn’t. The IT Department escalated the case. He ended up paying not just the disallowed amount but a penalty close to ₹3.5 lakh. All because he ignored the first letter.

It’s like ignoring a small leak in your roof. A few drops today, a collapsed ceiling tomorrow.

Conclusion: Get It Right, Stay Safe

The 80GGC deduction is a solid way to reduce your tax liability while supporting political parties. But it’s not free money. It comes with strings attached.

If you’re an NRI, yes, you can claim it. But check twice before donating. If you’re a resident, the same rules apply: donate electronically, keep your receipts, and make sure the party is registered.

And if you ever get an income tax notice? Stay calm, gather your proof, and respond on time. Correcting early is far better than ignoring and facing penalties later.

At the end of the day, tax deductions are like sharp tools. Use them correctly, and they make your job easier. Use them carelessly, and you risk cutting yourself.

So file wisely. Donate responsibly. And stay on the right side of the taxman.

0 Comments