If you’re an NRI filing your income tax return in India, you’ve likely faced this dilemma:

Should I choose the old tax regime or the new one?

It’s a simple question, but the answer isn’t.

Since India introduced the dual-tax-regime system, the confusion has only grown — especially for NRIs. With Budget updates over the years, the new regime has now become the default option. But that doesn’t necessarily mean it’s the better one for you.

Think of it like choosing between two flight tickets — one cheaper but without baggage allowance, and the other slightly costlier but packed with benefits. Both get you to your destination. The difference is how much value you get along the way.

For NRIs, the stakes are even higher. Deductions, rebates, and exemptions differ for resident taxpayers. Pick the wrong one, and you might end up paying more than you should.

And remember — the ITR filing deadline for FY 2024–25 is 31 July 2025. Filing early avoids errors, penalties, and last-minute panic.

What Is the Old Tax Regime?

The old tax regime is India’s traditional income-tax system. It allows taxpayers to claim multiple deductions and exemptions that reduce taxable income.

If you’ve ever saved in ELSS, bought life insurance, or paid home loan interest, you’ve probably benefited from this regime.

It’s flexible, but also detailed. You need to track investments, collect proofs, and plan carefully.

For NRIs, this system works beautifully if you have a consistent Indian income or investments that qualify for tax benefits.

Key Features of the Old Regime

- Lets you reduce taxable income using Section 80C, 80D, 80E, 80G, 24(b), and others.

- Suitable for NRIs with Indian property, dependents, or investment portfolios.

- Encourages disciplined tax-saving habits through eligible schemes.

- Slightly higher tax rates — but lower effective tax after deductions.

In short, you pay tax only on what’s left after deductions.

Common Deductions for NRIs under the Old Regime

| Section | Deduction Type | Limit / Note |

|---|---|---|

| 80C | ELSS, life insurance, tuition fees | ₹1.5 lakh |

| 80D | Medical insurance | ₹25,000 – ₹50,000 |

| 80E | Education loan interest | Full interest |

| 80G | Donations | 50% – 100% deduction |

| 80TTA | Savings account interest | ₹10,000 |

| 24(b) | Home loan interest | ₹2 lakh |

| 80EE | Additional home loan benefit | ₹50,000 |

Example: If you pay ₹1 lakh towards ELSS and ₹25,000 for medical insurance, you reduce your taxable income by ₹1.25 lakh.

What Is the New Tax Regime in India?

The new tax regime, introduced in 2020, was designed to simplify taxation.

The idea was simple — lower tax rates, no complicated deductions. You pay on what you earn, not on what you save.

Over the years, the government has tweaked it further. By Budget 2023, the new regime became the default, meaning if you don’t actively choose the old regime, the new one applies automatically.

Key Features of the New Regime

- Six tax slabs, starting with ₹3 lakh as the basic exemption limit.

- Lower tax rates compared to the old regime.

- No major deductions — 80C, 80D, HRA, LTA, etc. are gone.

- Standard deduction of ₹50,000 applies only to residents, not NRIs.

- Simplicity over savings — ideal for those who want fewer calculations.

Think of it like choosing a fixed-price buffet. You don’t get to mix and match dishes (deductions), but it’s quick and straightforward.

The Trade-Off: Simplicity vs. Flexibility

Under the old regime, you can design your tax plan like a custom suit — fitted to your life, income, and family.

The new regime, on the other hand, is like ready-to-wear clothing — convenient but one-size-fits-most.

For NRIs, this trade-off matters because many deductions that reduced tax in the old regime simply don’t exist in the new one.

Old vs New Tax Regime – Key Differences for NRIs

| Aspect | Old Regime | New Regime |

|---|---|---|

| Tax Rates | Higher, but deductions lower taxable income | Lower, but limited deductions |

| Deductions | Multiple sections (80C–80U) available | Very few allowed |

| Complexity | Requires calculation & proofs | Simple and clean |

| Flexibility | Full tax planning possible | Rigid, no customization |

| NRI Benefits | Full access to eligible deductions | Very limited |

| Best For | NRIs with Indian income & investments | NRIs with minimal or fixed income |

If you’re the type who actively manages investments or owns a property in India, the old regime often results in higher tax savings.

If your only Indian income is small — say, NRO savings or rent — the new regime could be simpler and easier.

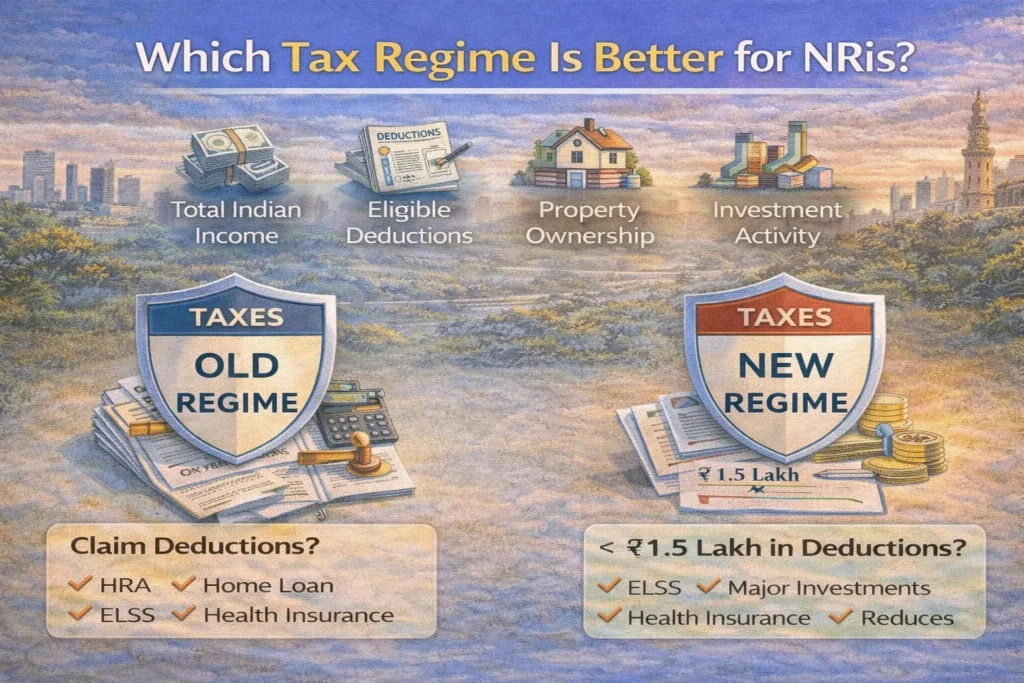

Which Tax Regime Is Better for NRIs?

There’s no one-size-fits-all answer here.

It depends on four factors:

- Your total Indian income

- Eligible deductions

- Property ownership

- Investment activity

Choose the new regime if your deductions are below ₹1.5 lakh or if you have no major investments.

Stick with the old regime if you’re claiming HRA, home loan benefits, ELSS, or health insurance deductions.

A useful tip — if you don’t have business income in India, you can switch regimes every year while filing your ITR. That gives you flexibility to adapt annually.

Scenarios Where the Old Tax Regime Works Better for NRIs

1. Investment in Tax-Saving Instruments (80C)

If you invest in ELSS, life insurance, or NPS, you can claim up to ₹1.5 lakh deduction under Section 80C.

Example: An NRI investing ₹1.5 lakh in ELSS saves ₹30,000 in tax (20% slab).

2. Home Loan Interest (Section 24 + 80EE)

Own a house in India? The old regime lets you claim:

- ₹2 lakh under Section 24(b)

- Plus ₹50,000 extra under Section 80EE

That’s ₹2.5 lakh off your taxable income.

3. Medical Insurance Premiums (80D)

You can claim up to ₹25,000 (self/family) or ₹50,000 (senior citizen parents) for health insurance.

4. Education Loans & Donations (80E, 80G)

If you’ve taken an education loan or donated to registered charities, these deductions reduce your taxable income further.

👉 Calculate your savings with our 80C & 80D Planner. (Coming Soon)

Scenarios Where the New Tax Regime Works Better for NRIs

1. Minimal Indian Income

If your income is limited to NRO interest or a small rent, deductions won’t matter much. The new regime’s lower slabs could save you time and effort.

2. You Prefer Simplicity

No need to collect receipts or calculate deductions. Just file, pay, and move on. Perfect for busy professionals abroad.

3. No 80C or 80D Eligible Investments

If you’ve shifted most investments abroad or don’t maintain insurance/policies in India, there’s little use sticking with the old system.

For many such NRIs, the new regime provides peace of mind — even if the savings are slightly lower.

Old vs New Tax Regime – Updated Slab Comparison (FY 2024–25)

| Income (₹) | Old Regime | New Regime |

|---|---|---|

| Up to 2.5 lakh | Nil | Up to 3 lakh – Nil |

| 2.5 – 5 lakh | 5% | 3 – 6 lakh – 5% |

| 5 – 10 lakh | 20% | 6 – 9 lakh – 10% |

| 10 – 12 lakh | 30% | 9 – 12 lakh – 15% |

| 12 – 15 lakh | 30% | 12 – 15 lakh – 20% |

| Above 15 lakh | 30% | Above 15 lakh – 30% |

⚠️ Note: The standard deduction and 87A rebate are not available to NRIs.

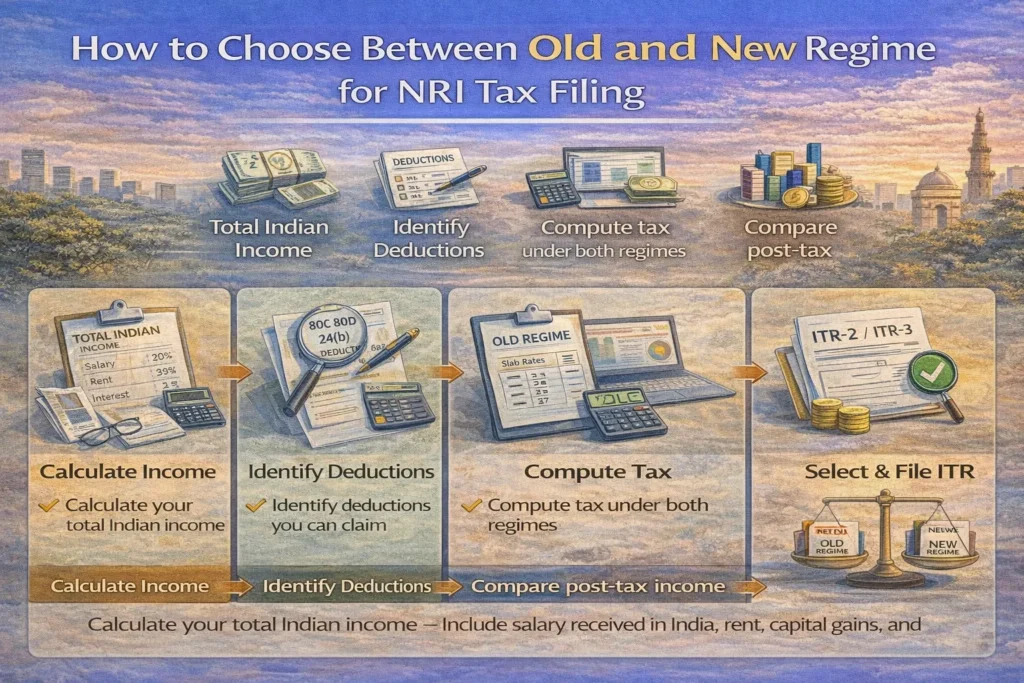

How to Choose Between Old and New Regime for NRI Tax Filing

Here’s a quick way to decide:

- Calculate your total Indian income – Include salary received in India, rent, capital gains, and NRO interest.

- Identify deductions you can claim – Check 80C, 80D, 24(b), 80G, and others.

- Compute tax under both regimes – Use the latest slab rates.

- Compare post-tax income – See where you pay less.

- Select regime in your ITR-2 or ITR-3 before submitting.

📲 Compare your NRI taxes instantly → [Launch Calculator]

Frequently Asked Questions (FAQs)

1. Which income is taxable for NRIs?

Any income earned or received in India — salary, rent, capital gains, and NRO interest.

2. When must NRIs file returns?

If your total income exceeds ₹2.5 lakh under the old regime or ₹3 lakh under the new one.

3. Do NRIs pay advance tax?

Yes, if your total tax liability exceeds ₹10,000 in a financial year.

4. Which ITR form should NRIs use?

ITR-2 (if no business income) or ITR-3 (if you have business/professional income).

5. Are deductions like 80C and 80D available to NRIs?

Yes, but only under the old regime.

6. Is foreign income taxable for NRIs?

No, unless it is received directly in India.

7. Can NRIs claim 80C in the new regime?

No. The new regime excludes major deductions.

Conclusion

Choosing between the old and new tax regimes isn’t just about slabs — it’s about strategy.

If you’re an NRI with Indian investments, home loans, or insurance plans, the old regime likely helps you save more.

If you earn small or fixed income and want a no-frills filing process, the new regime is your best friend.

The smart move? Compare both each year before you file. Use tools, talk to professionals, and make data-driven decisions.

Because every rupee saved legally is a rupee earned wisely.

0 Comments