For many people in India, the words “income tax” bring stress. Forms. Deadlines. Notices. Numbers that do not seem to add up. This fear usually comes from not knowing how the system works.

The Income Tax Act, 1961 is the main law that governs how income tax works in India. It decides who has to pay tax, how much tax is payable, and when it has to be paid. The good part is this. You do not need to understand the entire law. Not even close.

If you are a salaried employee, freelancer, or small business owner, only a small part of the Act applies to you. Understanding those basics can save you money, help you plan better, and reduce the chances of getting tax notices.

This guide explains the Income Tax Act 1961 in simple language for Indian taxpayers. No legal words. No complex sections. Just clear explanations, examples, and practical clarity.

Think of this like learning basic traffic rules. You do not need to know how roads are built. You just need to know how to drive safely.

What Is the Income Tax Act 1961?

The Income Tax Act, 1961 is a law passed by the Indian Parliament. It came into force on 1 April 1962. Since then, it has been the backbone of India’s income tax system. In simple terms, this Act answers three basic questions.

Who has to pay tax? On what income tax is charged?

How tax is calculated, collected, and enforced? The Act applies to almost everyone who earns income in India. This includes individuals, salaried employees, freelancers, professionals, business owners, and companies.

The law is administered by the Income Tax Department. They handle tax collection, processing of returns, refunds, and assessments. While the Act is detailed, its purpose is straightforward. It ensures the government collects revenue in a structured and fair way.

Objectives of the Income Tax Act 1961

Every law is created with a purpose. The Income Tax Act is no different.

One major objective is to collect revenue for the government. This money is used to run the country. Roads, hospitals, schools, defence, and welfare schemes all depend on tax collections.

Another objective is fair distribution of the tax burden. People who earn more are expected to pay more tax. This is why India follows a progressive tax system. The Act also encourages savings and investments. Sections like 80C, 80D, and others reward people who save or insure themselves.

Preventing tax evasion is another key goal. Clear rules, penalties, and reporting systems exist to reduce misuse. Finally, the Act supports economic growth by guiding how income is taxed and how businesses operate.

Key Features of the Income Tax Act 1961

One important feature is that the Act applies to the whole of India. Income earned anywhere in India comes under its scope. Tax is based on income. If you earn, you pay. If you do not earn beyond a basic limit, you do not pay.

India follows a progressive tax system. Higher income attracts higher tax rates. Lower income is taxed lightly or not at all. Tax is assessed annually. Every financial year is reviewed separately.

The Act treats residents, non-residents, and companies differently. Rules change based on who you are and where you live. Most importantly, the Act allows deductions, exemptions, and rebates. These are legal ways to reduce tax liability.

Structure of the Income Tax Act 1961 in Simple Terms

The Act is divided into sections and chapters. Sections are numbered rules. For example, Section 80C or Section 139. Chapters are groups of related sections. The government also issues rules and notifications to clarify how sections work. These are updated from time to time.

Every year, changes are introduced through the Finance Act, which is part of the Union Budget. This is why tax rules change almost every year.

Think of the Act as a textbook. Sections are individual lessons. Chapters are units. The Budget updates the syllabus.

Who Has to Pay Income Tax in India?

Income tax applies to different types of taxpayers.

Individuals form the largest group. This includes salaried employees, freelancers, and self-employed professionals. There are also Hindu Undivided Families, commonly known as HUFs. These are family units treated separately under tax law.

Firms, LLPs, companies, trusts, and associations also come under the Act. Residential status plays a big role. A person can be a resident, non-resident, or resident but not ordinarily resident. This status decides which income is taxable in India. In simple words, where you live and where you earn both matter.

Heads of Income Under the Income Tax Act 1961

The Act divides income into five broad categories called heads of income. This makes taxation organized and predictable.

Income from Salary: includes salary, bonus, allowances, pension, and perks received from an employer. If you have an employer-employee relationship, this head applies.

Income from House Property: covers rental income from property. Even if a property is vacant, notional or deemed rent may apply in some cases.

Profits and Gains from Business or Profession: includes income from business, freelancing, consulting, or professional services.

Capital Gains: arise when you sell assets like property, shares, or mutual funds at a profit.

Income from Other Sources: is a residual category. Interest, dividends, gifts, and winnings fall here.

Every rupee you earn fits into one of these heads.

Income Tax Act 1961 for Salaried Individuals

For salaried employees, the Act is relatively simple once broken down.

Salary includes basic pay, allowances, bonuses, and perquisites. Certain deductions like the standard deduction reduce taxable salary. Allowances such as House Rent Allowance and Leave Travel Allowance may be partly exempt if conditions are met.

Employers deduct tax at source, known as TDS. This is not final tax. It is only an advance payment. Form 16 is issued by the employer. It shows salary paid and tax deducted.

Even if TDS is deducted fully, filing an income tax return is still important. It acts as proof of income and compliance.

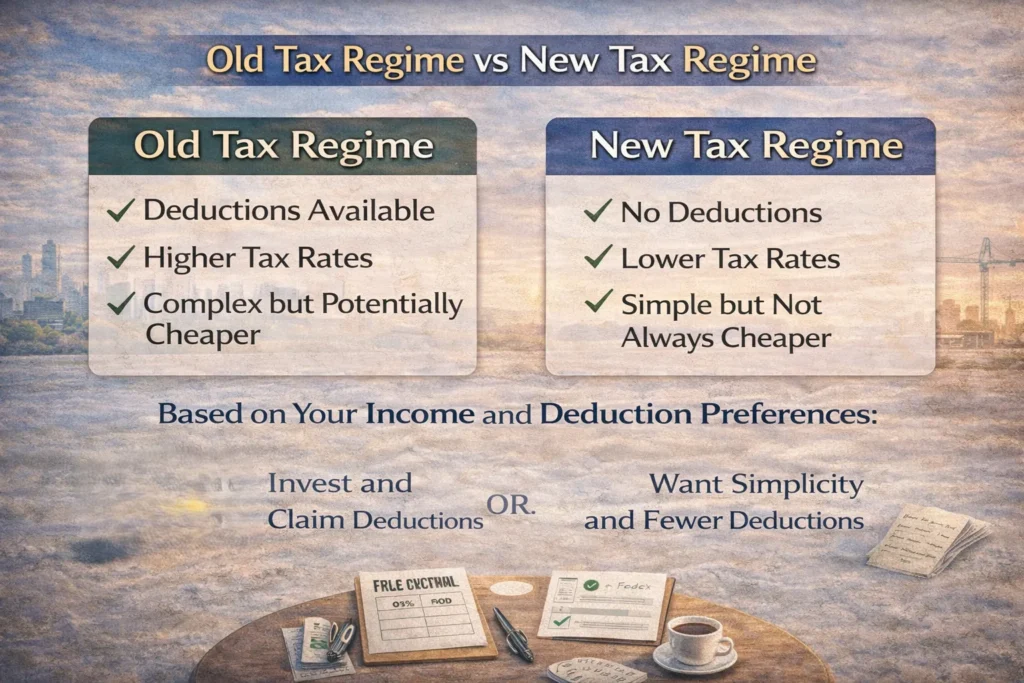

Old Tax Regime vs New Tax Regime

India currently offers two tax regimes.

The old tax regime allows various deductions and exemptions. Tax rates are higher, but deductions like 80C, 80D, and HRA reduce taxable income. The new tax regime offers lower tax rates but removes most deductions and exemptions. It is simpler but not always cheaper.

The choice depends on your income structure. If you invest and claim deductions, the old regime may suit you. If you prefer simplicity and have fewer deductions, the new regime may work better. Choosing the right regime is like choosing between cooking at home or ordering food. One gives control. The other gives convenience.

Deductions and Exemptions Explained Simply

- Deductions reduce taxable income. Exemptions remove certain income from tax completely.

- Section 80C allows deductions for investments like provident fund, ELSS, life insurance, and tuition fees.

- Section 80D gives deductions for health insurance premiums.

- Section 24 allows deduction of interest paid on home loans.

- Section 80CCD supports contributions to the National Pension System.

- Section 10 lists incomes that are exempt, such as certain allowances and benefits.

- Using these provisions legally can lower tax significantly.

Step-by-Step Guide to Compute Taxable Income

Tax calculation follows a fixed order.

- First, calculate income under each head. Salary. House property. Capital gains. Others.

- Next, add all incomes to get gross total income.

- Then, subtract eligible deductions.

- This gives taxable income.

- Apply tax slabs to calculate tax.

- Add health and education cess.

- Reduce TDS and advance tax already paid.

- The final result is either tax payable or refund due.

- This step-by-step approach avoids confusion.

Important Sections Every Taxpayer Should Know

- Some sections appear often.

- Section 10 covers exemptions.

- Section 80C and 80D cover popular deductions.

- Section 87A provides rebate for low-income taxpayers.

- Section 139 deals with filing of income tax returns.

- Section 143 relates to assessment.

- Sections 234A, 234B, and 234C deal with interest for delays or defaults.

You do not need to memorize them. Just recognize their purpose.

Income Slabs Explained for Beginners

- Tax slabs divide income into ranges. Each range is taxed at a different rate.

- Only the income within a slab is taxed at that slab rate. This is important.

- For example, if part of your income falls into a higher slab, only that part is taxed at the higher rate.

- The effective tax rate is usually lower than the highest slab rate.

- This system ensures fairness.

Common Myths About the Income Tax Act 1961

Many people believe only rich people pay tax. This is false. Anyone earning above the basic exemption limit may have to pay.

Some think filing returns is optional. It is not, in many cases.

Others believe TDS is final tax. It is only an advance.

Many think a CA is mandatory. It is not. Many people file returns on their own.

Understanding the law clears these myths.

Conclusion

The Income Tax Act, 1961 is not something to fear. It is a framework that explains how income is taxed in India. For most taxpayers, understanding the basics is enough.

When you know how income is classified, how deductions work, and how tax is calculated, you make better decisions. You save money legally. You avoid stress. You stay compliant.

A basic understanding of the Income Tax Act 1961 empowers every Indian taxpayer to stay informed, compliant, and financially confident.

Is the Income Tax Act 1961 still relevant today?

Yes, the Income Tax Act 1961 is very much relevant today. It continues to be the foundation of India’s income tax system. Although the law was introduced decades ago, it is updated regularly through annual budgets, amendments, and notifications. These updates ensure that the Act keeps pace with changes in the economy, income patterns, and technology.

Do I need to read the full Act?

No, most taxpayers do not need to read the entire Act. The law is long and detailed, and much of it applies only to specific situations. Salaried employees and small taxpayers usually need to understand only the basic concepts, income heads, common deductions, and filing requirements. Knowing the relevant parts is enough for practical compliance.

What happens if I do not follow the Act?

If you do not follow the Income Tax Act, you may face consequences such as interest on unpaid tax, monetary penalties, or notices from the tax department. In serious cases, prolonged non-compliance can lead to scrutiny or legal action. Most issues can be avoided by filing returns on time and paying the correct tax.

How often does the Act change?

The Income Tax Act changes frequently, usually once every year through the Union Budget. These changes may include new tax slabs, revised deductions, or procedural updates. In addition, clarifications and rules may be issued during the year. This is why tax rules you followed last year may not be exactly the same this year.

Where can I check official updates?

Official updates can be checked on the website of the Income Tax Department. Budget announcements, government notifications, and press releases are also reliable sources. Referring to official platforms helps ensure that the information you rely on is accurate and up to date.

0 Comments