You open the invoice. Your eyes scan down the page, past the itemized charges and the total amount due. Then you see it. A small box with a seemingly simple instruction: “Remit To.”

Your brain freezes for a second. Is this your address? Is it their office? Where exactly are you supposed to send this check?

If this has ever happened to you, you are not alone. The term “Remit to Address” is one of those formal financial phrases that can cause confusion. But understanding it is crucial for making sure your payments arrive safely and on time.

In this guide, we will break down everything you need to know. We will explain what a remit to address is, why it matters, and how to use it without a hitch. Let us clear up the confusion for good.

Remit to Address: A Simple Definition

Let us start with the basics.

A Remit to Address is the official address where you should send a payment. You will also hear it called a Remittance Address. Think of it as a set of GPS coordinates for your money. It tells you, the payer, the exact destination for your check, bank transfer, or money order.

This address is almost always provided by the company or person you are paying. You will find it on invoices, bills, and payment slips. The word “remit” simply means “to send.” So, “remit to” literally means “send payment to.”

In simple terms: It is the specific mailbox or bank where the recipient wants to receive payments to ensure they are processed quickly and correctly.

Remit Address Meaning

In contrast to the company’s general mailing address, a remit address (also known as a remittance address) is the precise physical or electronic location where you send payments (such as checks or bank transfers) for goods or services. This ensures that payments go directly to the accounts/finance department for quicker processing. Frequently found on invoices, it serves as a designated mailbox for your money, indicating precisely where to “send to” (remit) funds.

Why the Remit to Address Matters So Much

You might wonder why a simple address deserves so much attention. The truth is, getting it right has a direct impact on your finances and your relationship with the vendor.

For businesses receiving payments, a clear remit to address is the backbone of their accounts receivable process. It ensures that all payments are funneled to the right department, often a locked P.O. Box or a specific bank for processing. This prevents checks from getting lost in a generic mailroom or sitting on the wrong desk. It helps them track incoming funds efficiently and reconcile their books without a nightmare of chasing down missing payments.

For you, the person or business making the payment, using the correct address is just as critical.

Sending a payment to the wrong address can lead to frustrating delays. Your payment could be returned to you, or worse, it could be lost in the system. This often results in late fees, service interruptions, and hours spent on the phone with customer service to resolve the issue. I once saw a client’s payment get delayed by three weeks because they used the company’s public office address instead of the dedicated “Remit To” P.O. Box listed on the invoice. Those three weeks came with a late fee and a lot of unnecessary stress.

Using the remit to address is the easiest way to ensure your payment is posted the moment it is received.

Remit to Address vs Billing Address: The Crucial Difference

This is where most of the confusion happens. People often think the “Billing Address” and the “Remit to Address” are the same thing. In many cases, they can be identical. But when they are different, using the wrong one causes major problems.

Let us break down the key differences.

| Feature | Remit to Address | Billing Address |

|---|---|---|

| Purpose | This is where the payment should be sent. | This is the address of the person or company making the payment. |

| Who Owns It | It belongs to the vendor or payee (the one receiving money). | It belongs to the buyer or payer (the one sending money). |

| Where You See It | In the payment instructions section of an invoice or bill. | Usually in the header of an invoice, often under “Bill To.” |

| Common Use | Mailing checks, directing wire transfers. | Verifying your identity, generating tax documents, and general correspondence. |

Imagine you buy a laptop for your office in Seattle from a large company headquartered in Texas. The “Bill To” address on the invoice will be your Seattle office. This is for their records. However, the “Remit To” address might be a P.O. Box for their payment processing center in Ohio. Sending your check to the Texas headquarters would only slow things down.

The “Bill To” address is about who is being billed. The “Remit To” address is about where the money goes.

Where You Will See “Remit to Address”

This term is not just for business-to-business invoices. You will encounter it in many areas of your financial life. Recognizing it is the first step to using it correctly.

- Vendor and Supplier Invoices: This is the most common place. Any company you have a formal account with will include a remit to address on their invoices.

- Utility and Telecom Bills: Your electricity, water, and phone bills almost always have a specific “Remit Payment To” address, which is often a P.O. Box.

- Loan and Mortgage Statements: Your monthly loan statement will clearly indicate where to send your payment.

- Tax Forms and Government Payments: When you owe money to tax authorities, they provide a very specific remittance address for different types of payments.

- Bank Remittance Instructions: This is especially important for international wire transfers. The “remit to” address here is often the beneficiary bank’s address.

Here is a typical example from an invoice:

Invoice #: INV-1001

Bill To:

Global Solutions Inc.

123 Main Street

Chicago, IL 60601

Remit To:

XYZ Corporation

P.O. Box 45678

Omaha, NE 68102

In this case, you must send your payment to the P.O. Box in Omaha, not the Chicago address.

Real World Examples of a Remit to Address

Let us make this even clearer with some concrete, real world scenarios.

Example 1: The Standard Business Invoice

You run a small bakery and receive an invoice from your flour supplier.

=== INVOICE FROM FLOUR POWER CO. ===

Bill To:

The Daily Bread Bakery

45 Oak Avenue

Portland, OR 97205

Remit To:

Flour Power Co.

Lockbox 1234

567 Payment Center Drive

Phoenix, AZ 85001

Items:

50 lbs Organic Flour - $100.00

Total Due: $100.00

What you do: You write a check for $100 to “Flour Power Co.” and mail it to the Lockbox in Phoenix, Arizona. You do not send it to their corporate office in another state. The lockbox is a secure mailbox managed by their bank, ensuring speedy processing.

Example 2: The International Bank Remittance

You are in the United States and need to send money to a friend’s bank account in London. Your bank provides you with wire transfer instructions that include:

Beneficiary Name: Jane Doe Beneficiary Bank: Barclays Bank PLC Remit to: Barclays Bank PLC, 1 Churchill Place, London, E14 5HP, UK SWIFT/BIC: BARCGB22 Account Number: 12345678

What you do: In this context, the “Remit to” address is the specific bank branch address where the beneficiary holds their account. Your bank uses this information to route the international payment correctly through the SWIFT network. Providing the wrong bank address could misroute the entire transfer.

How to Use a Remit to Address Correctly

Now that you can spot a remit to address, let us talk about how to use it properly. The rules are slightly different depending on whether you are paying a bill or receiving payments.

For Payers (The Customers):

- Always Double Check: Before you seal the envelope or submit an online payment, always look for the “Remit To” or “Payment Address” section. Do not assume it is the same as the company’s contact address.

- Copy it Exactly: Accuracy is non-negotiable. Copy the address exactly as it is written. A missing “Suite” number or a typo in the city name can be enough to delay your payment.

- Follow the Method: If the remit to address is a P.O. Box, they almost certainly want a check or money order mailed there. Do not try to send a courier package to a P.O. Box.

- For Electronic Payments: Even with online bill pay, your bank will often use this address to generate and mail a check on your behalf. Ensure the details in your bank’s system match the remit to address.

For Businesses (The Vendors):

- Make it Obvious: Design your invoices with a clear, well-labeled “Remit To” section. Do not hide it in the fine print.

- Be Specific: If your payment address is different from your corporate office, make that very clear. You can even add a note: “Please send all payments to the P.O. Box address below.”

- Provide Complete Banking Details: For international clients, your “Remit To” information must include your bank’s name, its physical address, and the necessary codes like SWIFT/BIC and IBAN. This eliminates guesswork for your customers.

- Keep it Updated: If your payment processing changes, update your invoice template immediately. Sending out old invoices with an obsolete remit to address is a recipe for lost revenue.

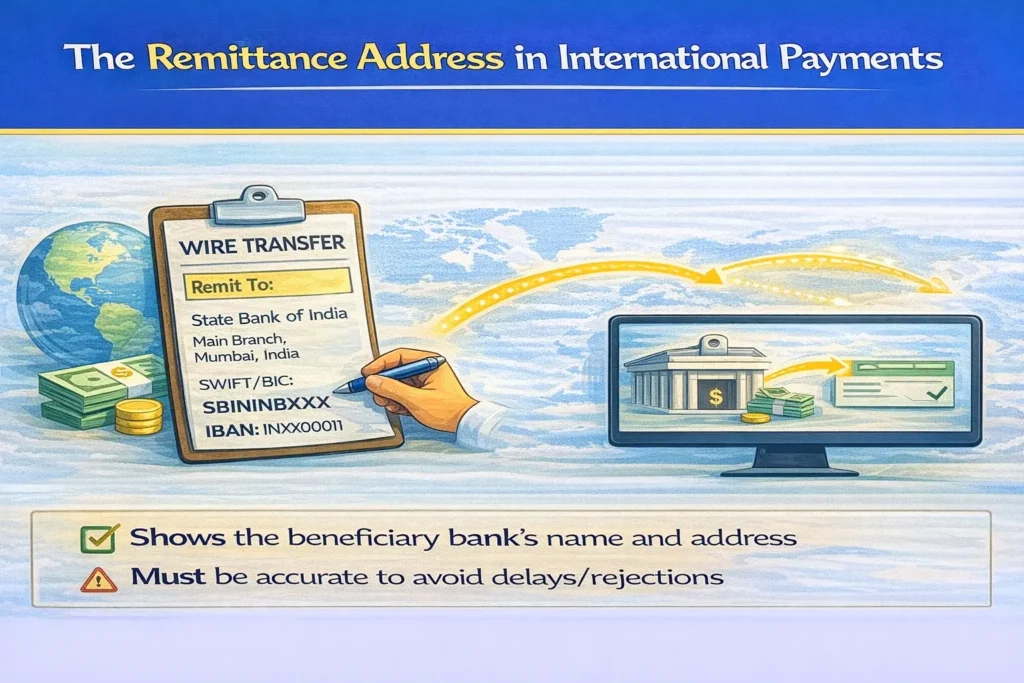

The Remittance Address in International Payments

This deserves its own section because the stakes are higher. When you are sending money across borders, the “remit to address” takes on a new level of importance.

In international wire transfers, the remittance address is typically the beneficiary bank’s address. This is not a suggestion. It is a core requirement for the global messaging system that banks use to communicate.

Banks need the beneficiary bank’s address to correctly identify the receiving institution and route the money through the proper channels. An incorrect or missing address is a common reason why international wires get held up or even rejected. The money can end up in a holding account at an intermediary bank, waiting for someone to provide the correct details.

For example, if you are an NRI sending money back to India, the instructions might say “Remit to State Bank of India, Main Branch, Mumbai.” Providing this address ensures your money reaches the correct banking system in India before being credited to your family’s individual account.

Common Confusions Around Remit to Address

Let us tackle some of the most frequent questions and misunderstandings head on.

- “Is the remit to address my address?” No. It is the address of the person or business you are paying. It is their destination for your payment.

- “Is it always the bank’s address?” Not always. On a local utility bill, it is probably just a P.O. Box for their payment processing. On an international wire instruction, it almost always is the bank’s address.

- “Can I just use the company’s billing address if I cannot find the remit to address?” This is a risky shortcut. You should always make an effort to find the correct remit to address. If it is missing from the invoice, contact the company’s accounts receivable department and ask for it. Using the billing address might work, but it could also lead to a delay.

- “What if the remit to address is a P.O. Box? Is that safe?” Yes, absolutely. Large companies use P.O. Boxes precisely because they are secure, efficient, and dedicated only to receiving payments. It is often the safest and most reliable place to send a check.

Frequently Asked Questions About Remit to Address

What does “Remit to” mean on an invoice?

On an invoice, “Remit to” is a direct instruction. It tells you the exact address where you need to send your payment. It is the location designated by the seller to receive checks, money orders, or sometimes even the payment stub for a bill.

Is remit to address the same as billing address?

Not necessarily. While they can be the same, they often are not. The billing address is your address, used for record-keeping. The remit to address is the vendor’s payment collection address. You should always default to using the remit to address for sending payments.

Where can I find the remittance address on a bill?

Look for a box or section labeled “Remit To,” “Payment Address,” “Make Check Payable to,” or “Pay This Amount To.” It is usually located in the bottom left or right corner of the bill or invoice, separate from the “Bill To” section.

Can a remit to address be a P.O. Box?

Yes, it is very common. Many businesses use Post Office Boxes as their official remittance address. This provides security and streamlines their mail and payment processing. You can safely mail your payment to a P.O. Box.

Is a remit to address required for bank transfers?

For domestic transfers, often not. You usually just need the account and routing numbers. For international wire transfers, yes, the beneficiary bank’s address (the remit to address) is almost always a mandatory field to ensure the wire is routed correctly through the SWIFT network.

How is a remit to address used in international payments?

In international payments, the remit to address is used to identify the specific branch of the beneficiary’s bank. This information is included in the wire transfer message to help intermediary banks direct the funds along the correct path to the final destination account.

Conclusion

The term “Remit to Address” might seem like just another piece of financial jargon. But as we have seen, it is a simple and powerful instruction. It is the key that ensures your payments are processed smoothly, efficiently, and without error.

The next time you look at an invoice or set up a payment, take that extra second to find the “Remit To” box. Copy the address carefully. By doing this one simple thing, you protect yourself from late fees, prevent headaches, and build a reputation as a reliable payer. It is a small step that makes a very big difference.

Also Read: US–India Income Tax Treaty: Benefits, DTAA Rules & How to Claim Relief

Also Read: PAN-Aadhaar Linking and Other Mandatory Disclosures for NRIs

0 Comments