Which Type of Bank Account Should an NRI Open in India? A Complete Guide

As globalization continues to reshape the world, more Indians are choosing to live, work, and settle abroad. However, Non-Resident Indians (NRIs) often maintain strong ties with India, whether it’s for investment, family, or property management. To facilitate these connections, India offers specialized bank accounts designed to help NRIs manage their finances effectively while residing outside the country.

Choosing the right type of bank account can make a significant difference in managing funds and handling foreign exchange, repatriation, and taxation. This guide will walk you through the various bank accounts available to NRIs and help you choose the one that best fits your needs.

Understanding the Basics: Who Qualifies as an NRI?

Before diving into the account types, it’s essential to understand who qualifies as an NRI. Under Indian law, an NRI is an Indian citizen who has lived outside of India for employment, business, or any other purpose for more than 182 days in a financial year. If you fall under this category, you’re eligible to open an NRI-specific bank account in India.

Types of Bank Accounts for NRIs in India

India offers three main types of bank accounts tailored specifically for NRIs: Non-Resident External (NRE) Account, Non-Resident Ordinary (NRO) Account, and Foreign Currency Non-Resident (FCNR) Account. Each type of account has unique features, benefits, and tax implications. Let’s explore each of these in detail:

1. Non-Resident External (NRE) Account

- The Non-Resident External (NRE) Account is one of the most popular choices for NRIs, especially those looking to manage income earned outside India. Here’s what you need to know about the NRE account:

Key Features of NRE Account:

- Currency: The NRE account is maintained in Indian Rupees (INR).

- Deposit Source: Only funds originating from outside India can be deposited into an NRE account, including foreign earnings from employment, business, or investments abroad.

- Repatriation: The principal and interest in an NRE account are fully and freely repatriable, which means you can transfer funds (in foreign currency) to your home country or any other country without restrictions.

- Tax Benefits: Interest earned on the NRE account is completely tax-free in India, making it a tax-efficient choice.

- Types of NRE Accounts: NRIs can open an NRE Savings Account, Current Account, Fixed Deposit, or Recurring Deposit.

Pros of NRE Account:

- Allows you to repatriate both principal and interest freely.

- Tax-free interest earnings in India.

- Ideal for managing income earned outside India.

Cons of NRE Account:

- Deposits are limited to foreign currency; you cannot deposit Indian rupees earned in India.

- Exchange rate fluctuations can impact the value of funds when converting from foreign currency to INR.

Who Should Open an NRE Account?

An NRE account is ideal for NRIs who:

- Earn their income outside India and want to remit it back to India.

- Prefer tax-free interest on their Indian bank accounts.

- Intend to repatriate funds back to their foreign account frequently.

2. Non-Resident Ordinary (NRO) Account

The Non-Resident Ordinary (NRO) Account is designed for NRIs who have income sources within India. This can include rental income, pension, dividends, or any other earnings within the country.

Key Features of NRO Account:

- Currency: The NRO account is also maintained in Indian Rupees (INR).

- Deposit Source: Both Indian and foreign sources of income can be deposited in an NRO account. You can use this account to hold income from property rental, dividends, pension, and more.

- Repatriation: Repatriation is allowed up to USD 1 million per financial year (including principal and interest), subject to compliance with tax regulations.

- Tax on Interest: Interest earned on an NRO account is taxable in India at a rate of 30% (plus applicable surcharge and cess), though tax treaties with certain countries can help reduce the tax burden.

- Types of NRO Accounts: Similar to the NRE account, the NRO account can be a Savings Account, Current Account, Fixed Deposit, or Recurring Deposit.

Pros of NRO Account:

- Allows deposits from both domestic (Indian) and foreign sources.

- Suitable for managing income earned in India while living abroad.

- Convenient for NRIs with family, investments, or properties in India.

Cons of NRO Account:

- Repatriation is limited to USD 1 million per financial year.

- Interest income is subject to tax in India.

Who Should Open an NRO Account?

An NRO account is suitable for NRIs who:

- Have income sources in India, such as rent, dividends, or pension.

- Do not need complete repatriability of the principal.

- Are comfortable managing tax obligations on interest earned.

3. Foreign Currency Non-Resident (FCNR) Account

The Foreign Currency Non-Resident (FCNR) Account is a specialized type of account for NRIs who wish to hold their deposits in foreign currency. This account is primarily offered as a fixed deposit account and can be held in multiple currencies.

Key Features of FCNR Account:

- Currency: FCNR accounts are maintained in foreign currencies such as USD, GBP, EUR, AUD, and others.

- Deposit Source: Only foreign currency deposits from abroad can be used to fund an FCNR account.

- Repatriation: Both the principal and interest in an FCNR account are fully repatriable, making it easy to transfer funds abroad without restrictions.

- Tax Benefits: Interest earned in an FCNR account is tax-free in India.

- Types of FCNR Accounts: FCNR accounts are generally offered as fixed deposits with terms ranging from 1 to 5 years.

Pros of FCNR Account:

- Allows NRIs to hold deposits in foreign currency, avoiding exchange rate risks.

- Interest income is tax-free in India.

- Both principal and interest are fully repatriable.

Cons of FCNR Account:

- Limited to foreign currency fixed deposits; it’s not available as a savings account.

- Fixed deposit rates can vary based on the currency and bank.

Who Should Open an FCNR Account?

An FCNR account is a good choice for NRIs who:

- Want to avoid currency fluctuation risks by holding deposits in a foreign currency.

- Prefer tax-free interest on fixed deposits in India.

- Intend to repatriate their funds back to their home country without any restrictions.

Comparison Table: NRE vs. NRO vs. FCNR Accounts

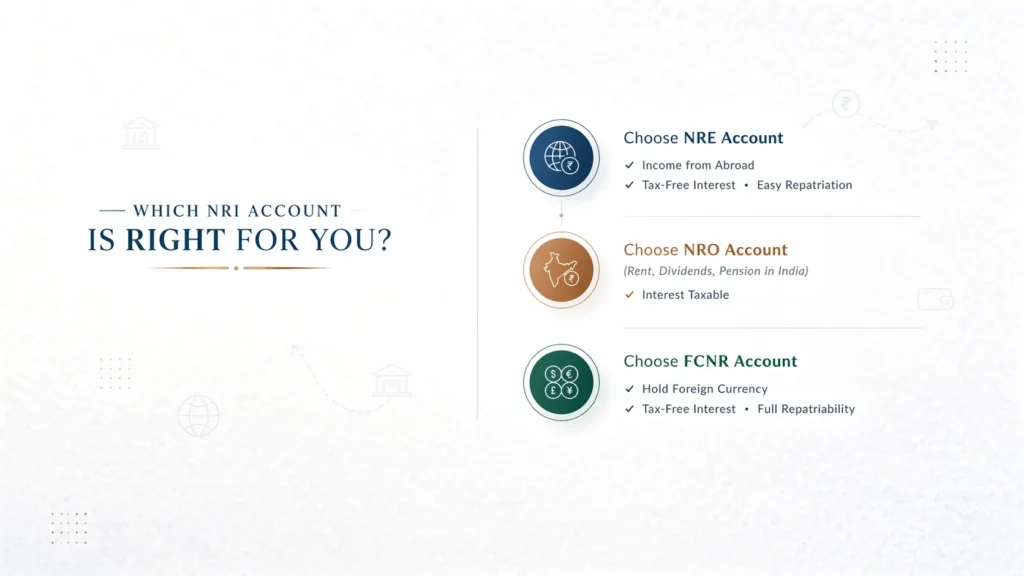

Which NRI Account is Right for You?

The right type of bank account depends on your income sources, financial goals, and repatriation needs. Here’s a quick summary to help you decide:

- Choose an NRE Account if your primary income source is abroad, you want tax-free interest, and you need to repatriate funds easily.

- Choose an NRO Account if you have income in India (such as rental income or dividends) and don’t mind paying taxes on interest earned.

- Choose an FCNR Account if you want to avoid currency exchange risk by holding funds in a foreign currency and need full repatriability with tax-free interest.

Conclusion:

Opening an NRI-specific bank account in India is a smart way to manage your finances effectively, whether for saving, investing, or supporting family back home. Take the time to consider your needs, evaluate the tax implications, and choose an account type that best supports your financial goals.

Remember, managing your finances as an NRI doesn’t have to be complex if you’re equipped with the right knowledge and resources. Choose the right account, stay compliant with regulations, and make the most of your financial journey in India!

0 Comments