Why Should NRIs File Tax Returns in India? A Complete Guide

As Non-Resident Indians (NRIs) continue to build ties with India through investments, properties, and family connections, they also need to navigate tax regulations to ensure compliance and avoid potential legal issues. While NRIs are not required to file income tax returns in India under all circumstances, there are several scenarios where doing so becomes essential or beneficial.

In this guide, we’ll explain the circumstances under which NRIs should file tax returns in India, the advantages of doing so, and how filing a return can help NRIs secure their assets and financial interests back home.

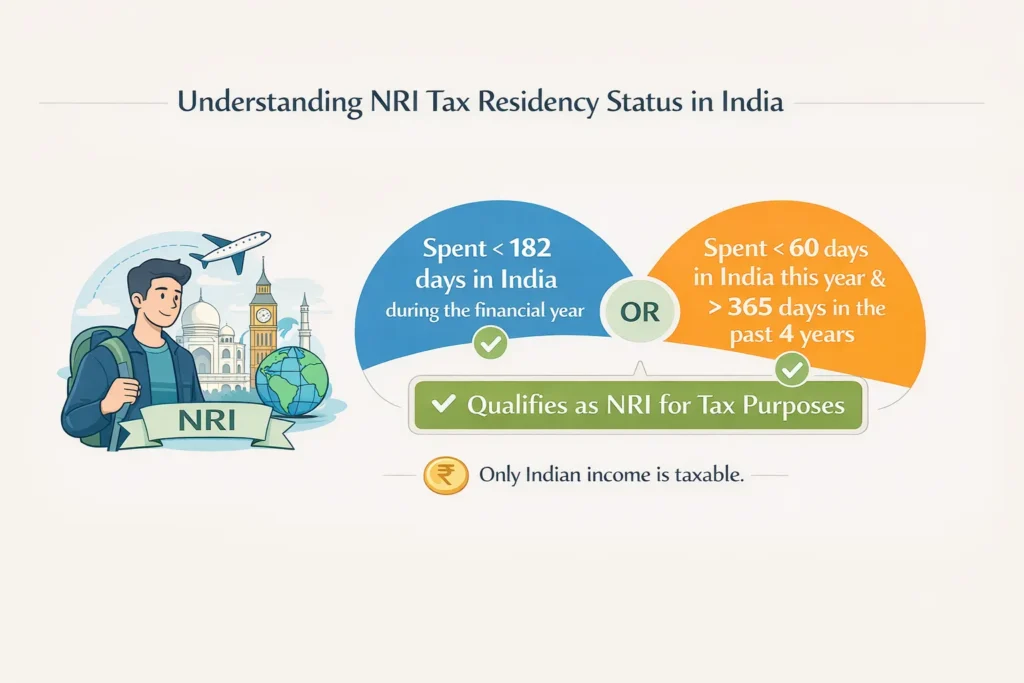

1. Understanding NRI Tax Residency Status in India

Before diving into the reasons for filing tax returns, it’s crucial to understand how the tax residency status of an NRI is determined.

According to Indian tax laws, an individual qualifies as an NRI if they:

- Spend less than 182 days in India during the financial year, OR

- Have spent more than 365 days in India over the past four years but less than 60 days in the current financial year.

If you meet either of these conditions, you are classified as an NRI for tax purposes, and only your income earned or received in India is taxable in India. However, despite limited tax liability, NRIs still have situations where filing tax returns in India is essential.

2. Scenarios When NRIs Must File Tax Returns in India

NRIs are legally required to file an income tax return in India under specific conditions:

a) If Taxable Income Exceeds the Basic Exemption Limit

As with resident Indians, NRIs are required to file an income tax return if their total income in India exceeds the basic exemption limit. As of the current financial year:

- The exemption limit for individuals under 60 is INR 2.5 lakh.

- For senior citizens (60 to 80 years old), the exemption is INR 3 lakh.

- For super senior citizens (over 80), the limit is INR 5 lakh.

If your taxable Indian income—such as rental income, capital gains, or business earnings—exceeds these limits, filing a tax return is mandatory.

b) To Claim Tax Refunds on Withheld Tax (TDS)

Many NRIs receive income in India that is subject to Tax Deducted at Source (TDS), especially on fixed deposits, property rent, dividends, or other earnings. Often, TDS is deducted at the highest slab rate (typically 30% for NRIs) regardless of the individual’s actual tax liability.

If you are eligible for a lower tax rate or exemption, filing a tax return allows you to claim a refund of the excess tax withheld. For instance, if your taxable income falls below the basic exemption limit, you can get a refund of the entire TDS amount deducted by filing a return.

c) For Offset of Capital Losses

If an NRI has capital gains or losses from investments in India, filing a tax return is essential to record these gains and losses for future benefit:

- Offset Capital Losses: NRIs can offset capital losses against capital gains in the same year, which can help reduce overall tax liability.

- Carry Forward Losses: Filing a tax return allows NRIs to carry forward capital losses for up to eight years, which can be offset against future gains to reduce tax liability in the coming years.

d) For Holding Assets Worth Over INR 1 Crore

The Indian tax authorities require anyone, including NRIs, to file a tax return if they hold assets worth over INR 1 crore. This includes property, deposits, and investments in India. Filing helps document ownership and ensures transparency with the Indian tax authorities.

e) For High-Value Transactions

NRIs are required to file tax returns if they engage in high-value transactions in India, even if their income is below the taxable limit. These transactions include:

- Deposits of more than INR 1 crore in a bank account.

- Spending over INR 2 lakh on foreign travel.

- Payments exceeding INR 1 lakh toward electricity bills.

Engaging in such high-value transactions can attract scrutiny from the tax authorities, and filing a return helps to avoid any red flags or potential notices.

3. Benefits of Filing Tax Returns as an NRI

In addition to legal compliance, there are several benefits that NRIs can enjoy by filing tax returns in India:

a) Building a Financial Profile in India

Filing regular tax returns helps NRIs build a financial profile, which is particularly valuable if they plan to take loans, open bank accounts, or invest in India. A tax return record makes it easier to avail of loans or credit cards from Indian banks, as it demonstrates financial discipline and compliance with tax regulations.

b) Repatriation of Funds

To transfer money from the sale of assets or investments in India back to their home country, NRIs often need to show proof of tax payment and file relevant forms with the Reserve Bank of India (RBI). Filing tax returns helps establish that taxes have been duly paid, easing the repatriation process.

c) Avoiding Penalties and Legal Complications

By filing a tax return, NRIs reduce the risk of scrutiny, penalties, or legal complications that can arise from unfiled returns. If the Indian tax authorities detect taxable income without corresponding filings, penalties and interest can accumulate. Filing ensures compliance and peace of mind.

d) Simplifying Tax Refunds

Filing a return is essential for NRIs to claim refunds on excess TDS deductions. For example, if your income doesn’t reach the taxable threshold but TDS has been deducted from your earnings, filing a return allows you to receive this amount back as a refund, avoiding unnecessary tax costs.

e) Documenting Asset Ownership and Transactions

NRIs who own multiple assets or conduct high-value transactions in India can use tax returns to document ownership and legitimate sources of funds. In the event of scrutiny, a clear record of filed returns can help prevent complications and clarify any questions the tax authorities may have.

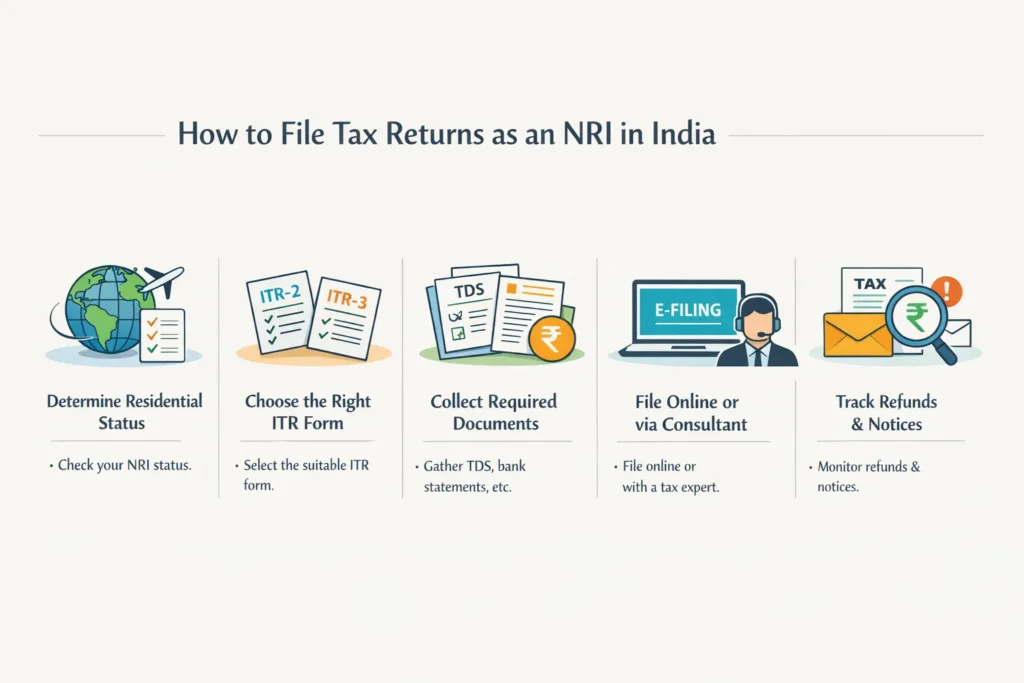

4. How to File Tax Returns as an NRI in India

The process for NRIs to file tax returns is largely similar to that of resident Indians, with a few key considerations:

a) Determine Residential Status

First, calculate your residential status for the financial year to confirm you are eligible to file as an NRI. This status determines which incomes are taxable and affects the filing process.

b) Choose the Right ITR Form

NRIs generally need to file ITR-2 if they have income from capital gains, rental income, or investments, or ITR-3 if they have income from a business or profession.

c) Collect Required Documents

Gather essential documents like Form 16A (TDS certificate), bank statements, investment proofs, and details of property or capital gains. These documents will support your filing and help you claim deductions or offsets as needed.

d) File Online or through a Tax Consultant

You can file online via the official Income Tax e-filing website or seek assistance from a tax consultant specializing in NRI filings. Consultants can help you navigate the intricacies of NRI tax law, ensuring compliance and maximizing benefits.

e) Track Refunds and Notices

After filing, check for any tax refunds due, and respond promptly if the tax department sends any notices or requests for further information.

5. Common Mistakes to Avoid When Filing as an NRI

To avoid complications and penalties, NRIs should steer clear of the following common filing errors:

- Incorrect Residential Status: Mistakenly filing as a resident instead of an NRI can lead to inflated tax liability.

- Omitting Indian Income: Even small incomes from rent, dividends, or interest in India must be reported.

- Claiming Ineligible Deductions: Some deductions available to residents are not applicable to NRIs, so check eligibility before claiming.

- Ignoring Foreign Tax Credit: If you’ve paid tax abroad on your Indian income, check if you’re eligible for relief under the Double Taxation Avoidance Agreement (DTAA).

Final Thoughts

Filing tax returns as an NRI in India may not always be mandatory, but it often proves beneficial. From securing refunds and simplifying repatriation to avoiding legal risks, tax filing can help NRIs stay compliant and manage their Indian income more effectively. Whether you have investments, property, or other financial interests in India, staying on top of tax obligations is crucial.

If you’re unsure of your tax liability or the filing process, consider consulting an expert in NRI taxation. They can provide tailored guidance, ensuring you meet compliance requirements and make the most of available benefits. With proactive tax planning, NRIs can navigate their financial lives in India smoothly, protecting their wealth and supporting their long-term goals.

Also read Expert NRI Tax Services in Pune for Hassle-Free Compliance, Simplify Your Finances with NRI Tax Services in Delhi, Everything You Need to Know About the Overseas Citizenship of India (OCI), Should NRIs/OCIs Buy Life Insurance in India or Their Home Country?

0 Comments