Life as an NRI is a mix of two worlds. You are building a future in a new country. Yet, a part of your heart and your financial dreams remain tied to India. You hear stories about India's booming economy. You see the potential for growth. But you are also busy. Managing a career and life overseas is demanding. The question lingers. How do you invest in India from thousands of miles away? The process seems complicated. The rules are confusing. You worry about taxes in two countries.

What if you could ignore the noise? What if there was a simple, almost automatic way to build wealth back home? There is. For millions of savvy NRIs, the answer is a Systematic Investment Plan (SIP) in Indian mutual funds.

Think of a SIP as your personal financial assistant in India. It works while you sleep. It invests for you while you focus on your career abroad. You do not need a large lump sum. You do not need to time the market. A SIP builds your future one small, regular step at a time. This guide will walk you through the five biggest reasons a SIP is a perfect fit for you. We will also break down the process into three simple steps. Let us get started.

Ride the Wave of India’s Economic Boom

Imagine you could have invested in America during its major industrial growth. Or in China during its manufacturing explosion. The opportunity was not just in companies. It was in the entire country's rise. Today, many experts see a similar story unfolding in India.

India is not just growing. It is sprinting. It is consistently one of the fastest-growing major economies in the world. This is not just a headline. It is a reality powered by millions of people.

Think about the young population. Over half of India is under thirty. These are people who are getting their first jobs. They are buying their first homes and cars. They are using smartphones to order food and shop online. This creates a massive wave of consumption. Companies that sell everything from soap to software are growing to meet this demand.

Then there is the digital revolution. UPI payments have changed how people transact. A farmer in a village can now receive payment directly on his phone. A street vendor accepts digital payments. This formalizes the economy and creates vast amounts of data. This data helps businesses understand their customers better than ever before.

Your SIP in an Indian mutual fund is your ticket to this growth story. You are not just buying a fund. You are buying a small piece of hundreds of these growing companies. As they succeed, the value of your investment grows with them. You are harnessing the energy of a nation on the move, all from the comfort of your home abroad.

Rupee Cost Averaging” Be Your Superpower

The stock market goes up and down. This is a fact. For many investors, this volatility is scary. They buy when everyone is optimistic and prices are high. They panic and sell when prices fall. This is how people lose money.

A SIP uses this market volatility to your advantage. It is a beautiful concept called Rupee Cost Averaging.

Here is how it works in simple terms. You invest a fixed amount of money at a fixed interval. Let us say you invest ₹10,000 every month. When the market is down, your ₹10,000 buys more units of the mutual fund. When the market is up, the same ₹10,000 buys fewer units. Over time, this averages out the price you pay for each unit. Your average cost is often lower than the average market price.

Let me show you with a real example. Imagine you start a SIP for three months.

| Month | SIP Amount (₹) | NAV (Price per Unit) | Units Bought |

|---|---|---|---|

| January | 10,000 | 50 | 200.0 |

| February | 10,000 | 40 | 250.0 |

| March | 10,000 | 60 | 166.7 |

| Total | 30,000 | Avg. Cost: ₹46.15 | 616.7 |

Look at what happened. The average NAV for the three months was ₹50. But because of your SIP, your average cost per unit was only ₹46.15. You bought most of your units when the price was low. This is the magic of rupee cost averaging. It is a disciplined, mathematical approach that removes emotion from investing. It turns market fear into your financial gain.

Effortless Discipline from Anywhere in the World

I know how busy life can get. Between work deadlines, family responsibilities, and settling into a new culture, managing investments in India can fall to the bottom of your list. You tell yourself, "I'll transfer money and invest next month." And then next month becomes next year.

A SIP solves this problem permanently. It is the ultimate "set it and forget it" financial tool.

Once you set up your SIP, an instruction is sent to your bank. Every month, on a date you choose, a fixed amount is automatically transferred from your NRI bank account to the mutual fund. The fund house then uses that money to buy units for you. The entire process is automatic.

You do not have to remember to log in. You do not have to write checks or initiate transfers manually. Your investment plan runs on autopilot. This automation builds financial discipline without any effort. It ensures you are consistently investing towards your goals, whether that is buying a house in India, saving for your child's education, or building a retirement corpus.

It protects you from your own emotions. When the market is crashing and your instincts tell you to sell, your SIP quietly continues to buy. When the market is soaring and you feel tempted to invest a huge amount, your SIP sticks to the plan. This steady, disciplined approach is the bedrock of long-term wealth creation.

Diversify Instantly, Without the Headache

Maybe you have thought about buying stocks directly. You read about a tech company doing well. You consider investing in it. But then you think, what if that one company has a problem? What if its new product fails? Putting all your money in one or two stocks is risky. It is like betting on a single horse to win the race.

To build a safe portfolio, you need to spread your money across many companies and sectors. This is called diversification. But for an NRI, researching and buying 50 different stocks is a nightmare. It is time-consuming and complex.

This is where mutual funds shine. A mutual fund pools money from thousands of investors like you. A professional fund manager then takes this large pool of money and invests it in a wide basket of stocks or bonds. By investing just ₹5,000 in a single mutual fund, you could own a small piece of 50 or 100 different companies.

You get instant diversification. You are invested in technology, banking, healthcare, and consumer goods all at once. If one company or sector has a bad year, the others can balance it out. Your risk is spread out and significantly reduced.

And you are not doing this alone. You have a team of experts working for you. The fund manager and their analysts spend their entire day researching companies. They read financial reports. They meet with company management. They make informed decisions about where to invest. You are essentially hiring the best financial brains in India to manage your money. All for a very small fee.

Smart Tax Planning with the DTAA Advantage

Taxes are often the biggest worry for NRIs. The fear of being taxed twice, both in India and your country of residence, is very real. This is the section that makes this guide truly valuable for you. Because as an NRI, you have a special tool to handle this: the DTAA.

First, let us understand the basic tax rules in India for mutual funds.

- Equity Funds (Investing mainly in stocks):

- If you sell your units within 1 year, it is called Short-Term Capital Gains (STCG). The tax rate is 15%.

- If you sell after 1 year, it is Long-Term Capital Gains (LTCG). Gains up to ₹1,00,000 in a year are tax-free. Gains above ₹1,00,000 are taxed at 10%.

- Debt Funds (Investing mainly in bonds):

- The gains are added to your income and taxed according to your income slab.

Now, here is the key part for you as an NRI. India has signed Double Taxation Avoidance Agreements (DTAAs) with over 85 countries, including the USA, UK, Canada, UAE, and Australia.

What does the DTAA do? It ensures that the same income is not taxed twice. In most cases, you will pay capital gains tax in India first. Then, when you report this income in your country of residence, you can show the tax you already paid in India. You can then claim a credit for that amount, reducing your tax burden there.

Let me give you an example. Suppose you are an NRI in the USA. You make a long-term capital gain of ₹1,50,000 on your SIP. You will pay 10% tax on ₹50,000 (the amount above ₹1 Lakh) in India. That is ₹5,000. When you file your taxes in the USA, you declare this gain. But you also show that you have already paid ₹5,000 in taxes to India. The US tax authorities will very likely give you a credit for this ₹5,000.

This mechanism prevents double taxation. It makes investing in India a tax-efficient endeavor. I strongly recommend you discuss your specific situation with a cross-border tax advisor. They can help you optimize your investments under the DTAA rules of your resident country. This one step can save you a significant amount of money and worry.

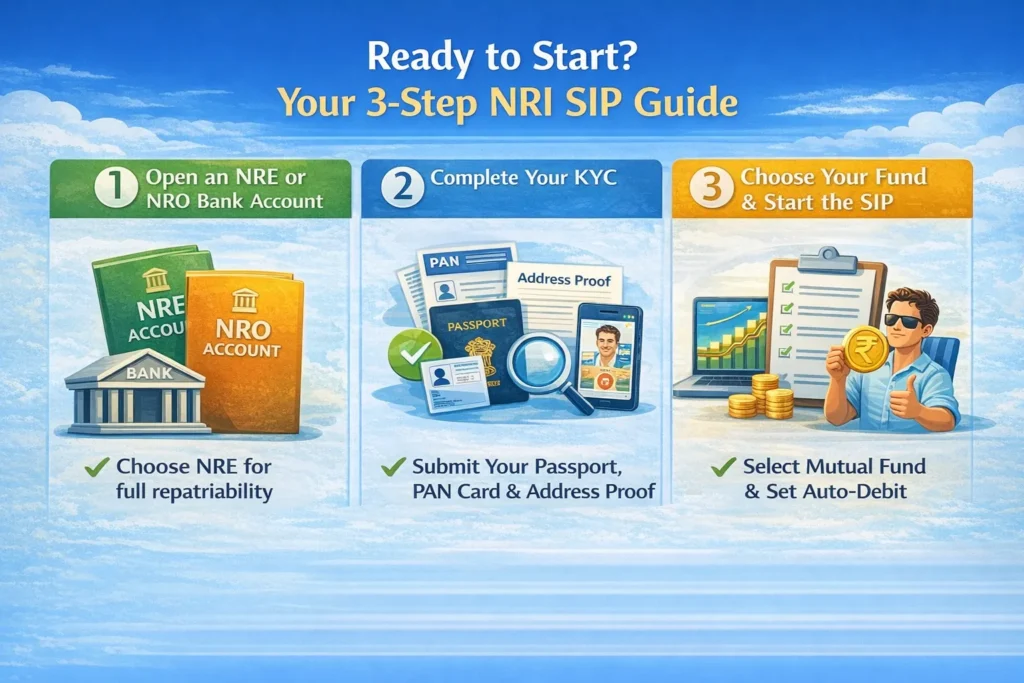

Ready to Start? Your 3-Step NRI SIP Guide

By now, the benefits should be clear. You might be wondering about the process. The good news is, it is much simpler than you think. Here is your straightforward, three-step action plan.

Step 1: Open an NRE or NRO Bank Account

This is your foundation. If you do not already have one, you will need to open an NRE (Non-Resident External) or NRO (Non-Resident Ordinary) account with a bank in India.

- NRE Account: Money in this account is fully repatriable. This means you can freely transfer both the principal and the earnings back to your country of residence. Investments made from an NRE account are also fully repatriable. This is the preferred account for most NRIs for investing.

- NRO Account: This account is for managing income you earn in India, like rent or dividends. The principal is generally not repatriable, but you can repatriate a certain amount of the income each year. You can also use an NRO account for investments.

My suggestion? Start with an NRE account for your SIPs for maximum flexibility.

Step 2: Complete Your KYC (Know Your Customer)

This is a one-time process. You need to prove your identity and address to the mutual fund company. The required documents are:

- A copy of your Passport.

- A copy of your PAN Card.

- Proof of your overseas address (like a driving license, utility bill, or bank statement from your resident country).

- A recent passport-sized photograph.

The best part? You do not need to be physically present in India. Most fund houses now offer fully paperless KYC. They use a video-based In-Person Verification (IPV) process. A representative will video call you, verify your documents, and complete the process. It is quick and convenient.

Step 3: Choose Your Fund and Start the SIP

Now for the exciting part. You need to select a mutual fund scheme that matches your financial goal and how much risk you are comfortable with. Are you saving for a long-term goal like retirement? An equity-focused fund might be suitable. Do you need the money in a few years and want less risk? A hybrid or debt fund could be better.

You can research funds on websites like Value Research or Moneycontrol. You can also consult with a SEBI-registered financial advisor. Once you have chosen, you can invest directly through the fund house's website or through a dedicated NRI investment platform.

You will fill out an application form and provide a cancelled cheque from your NRE/NRO account. Finally, you will set up an auto-debit instruction. This is the command that tells your bank to send a fixed amount to the mutual fund every month. And just like that, you are an investor. Your financial future in India is now on autopilot.

FAQ

Can I continue my existing Indian mutual fund SIP after becoming an NRI

Yes, you can. However, it is very important that you inform your mutual fund company about your change in status from 'Resident' to 'NRI'. You will also need to link your SIP to an NRE or NRO bank account. Do not continue using a resident Indian savings account.

What is the difference between investing through NRE and NRO accounts?

The key difference is repatriability. The money you invest and the returns you earn through an NRE account can be freely transferred back to your country of residence. For investments made through an NRO account, the original amount you invested is generally not repatriable. However, the returns and income generated from the investment can be repatriated, subject to certain limits and documentation.

Is the Dividend Option better for NRIs?A: Usually, it is not. The tax rules for

dividends have changed. Dividends are now added to your income and taxed at your income slab rate, which could be high. For most NRIs, the Growth Option is more tax-efficient. In this option, you only pay taxes when you sell your units. And if you hold them for the long term, you benefit from lower Long-Term Capital Gains tax.

Can I use a Power of Attorney (PoA) to manage my SIPs?A: Yes, you

absolutely can. Many NRIs grant a Power of Attorney to a parent, spouse, or sibling in India. This allows them to operate your investment and bank accounts on your behalf. Both you and the PoA holder will need to complete the KYC process with the mutual fund company.

Conclusion

Starting a SIP in Indian mutual funds is more than just an investment. It is a smart strategy designed for your life as an NRI. It connects your global earnings to India's local growth. It uses the power of discipline to smooth out market bumps. It gives you instant diversification and professional management. And with the DTAA, it becomes a tax-efficient way to build your wealth.

You have the opportunity to participate in a nation's rise. You do not need to be a financial expert. You just need a plan and the discipline to stick with it. A SIP provides both.

Your journey to building a strong financial foundation in India begins with a single step. Begin your research today. Consult with a SEBI-registered advisor to find the right funds for you. Or, explore the websites of reputable Asset Management Companies (AMCs) to see your options. The best time to start was yesterday. The second-best time is now.

0 Comments