Living abroad as a Non-Resident Indian comes with a unique set of joys and challenges. You are building a life across two worlds. But with that comes a complex web of financial responsibilities, especially when it comes to US taxes. One form that consistently causes confusion is the FBAR.

It sounds official. It sounds intimidating. But what is it, really? And more importantly, does it apply to you?

This guide is designed to cut through the legal jargon. We will walk you through everything you need to know about FBAR in plain English. We will cover what it is, who needs to file it, and how to do it correctly, all with a specific focus on the accounts you likely hold in India.

What Is FBAR?

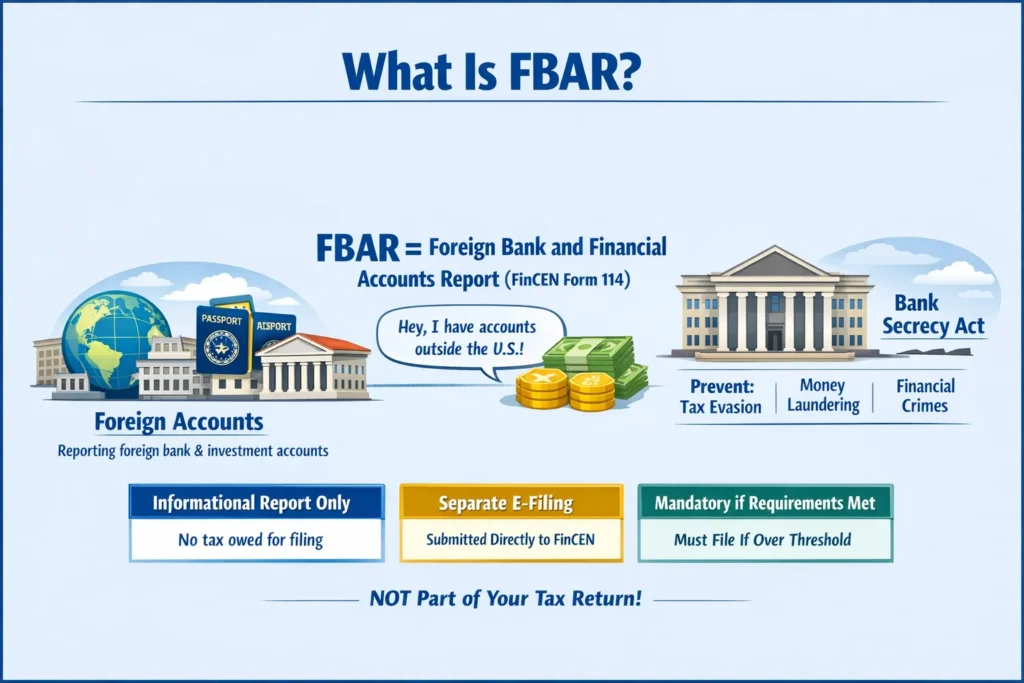

Let us start with the basics. FBAR stands for Foreign Bank and Financial Accounts Report.

Think of it as a simple financial headcount you give to the US government. It is you telling the US Treasury Department, "Hey, I have these savings and investment accounts outside the United States."

The official name for this report is FinCEN Form 114. FinCEN is the Financial Crimes Enforcement Network, a bureau of the US Treasury Department. This is a key point to remember. The FBAR is not filed with the IRS with your tax return. It is a separate, electronic-only filing sent directly to FinCEN.

This requirement exists under the Bank Secrecy Act. The goal is not to tax these accounts, but to prevent tax evasion, money laundering, and other hidden financial crimes. It is about transparency.

You do not owe any money by simply filing an FBAR. It is an informational return. The important thing to know is that filing is mandatory if you meet the requirements. It does not matter if you already paid taxes on the interest in India or if the accounts are tax-free. The filing requirement is separate.

Who Needs to File FBAR?

This is the most critical question for every NRI. The rules are specific, and it is easy to get them wrong.

You must file an FBAR if you are a US person and the total value of all your foreign financial accounts exceeded $10,000 at any point during the calendar year.

Let us break that down.

First, who is a "US person"?

- A US citizen, even if you live full-time in India.

- A US Green Card holder (Permanent Resident).

- Someone who meets the "US Resident" test for tax purposes.

Second, what does "$10,000 at any point" mean? This is the part that trips up many people. We are not talking about the year-end balance. We are talking about the maximum value each account held at any single moment in the year. And we are talking about the combined total of all your foreign accounts.

Imagine this scenario. You have two accounts in India:

- Your NRE savings account had a maximum balance of $6,000 in July.

- A joint fixed deposit with your father, where you have signing authority, had a maximum value of $5,000 in November.

Even though neither account alone crossed $10,000, their aggregate highest balance is $11,000. This means you have an FBAR filing requirement.

This rule applies to a wide range of accounts you might hold:

- NRE and NRO savings accounts

- Indian fixed deposits (FDs)

- Indian mutual fund accounts

- Indian stock trading accounts

- Life insurance policies with a cash surrender value

- Any joint accounts where you have financial interest or signature authority

FBAR Filing Thresholds Explained

The $10,000 threshold is the cornerstone of FBAR. It is crucial to understand it fully to know when you need to take action.

| Criteria | Requirement |

|---|---|

| Threshold Amount | $10,000 aggregate balance |

| Who Must File | US citizens, residents, and certain entities |

| Filing Frequency | Annually (by April 15, automatic extension to Oct 15) |

| Form | FinCEN Form 114 |

| Filing Mode | Electronic via BSA E-Filing website |

The key phrase is "at any time during the year." If the combined value of your foreign accounts touched $10,001 for even one day, you must file.

A common question is about currency conversion. You must convert your foreign account balances into US dollars. The rules state you should use the US Treasury's Financial Management Service rate for the last day of the year. Alternatively, you can use a reasonable, consistent exchange rate that applies on the day of the highest balance.

What does not count? Generally, accounts where you cannot access the funds, like the Indian Public Provident Fund (PPF) before maturity, do not need to be reported. Funds held in a foreign retirement plan or a foreign social security scheme also typically do not need to be reported. However, always double-check with a professional if you are unsure.

Types of Accounts to Report on FBAR

As an NRI, your financial life in India is diverse. It is important to know which of your Indian assets need to be declared on the FBAR. The rule is broad: if it is a financial account held with a foreign financial institution, it likely needs to be reported.

Here is a list of common accounts for NRIs:

- NRE (Non-Resident External) Savings Accounts: These are the most common. The foreign currency nature does not exempt them.

- NRO (Non-Resident Ordinary) Savings Accounts: These are also fully reportable.

- Fixed Deposits (FDs): Both NRE and NRO fixed deposits must be reported. Their maximum value during the year is what counts.

- Recurring Deposits (RDs): Same as FDs.

- Mutual Fund Accounts: Any holdings with an Indian asset management company (like HDFC MF, SBI MF, etc.) are reportable.

- Stock Trading Accounts: Your Demat and trading accounts with Indian brokers are considered financial accounts.

- PPF Accounts? This is a gray area. Since access is restricted, many experts do not recommend reporting it. However, if it has a withdrawal facility and you have used it, you may need to include it. Consult a tax advisor.

- Life Insurance Policies: Only if the policy has a cash value that you can access (like a ULIP). Term insurance with no cash value is not reportable.

- Joint Accounts and Accounts with Signature Authority: This is critical. If you have the authority to control the assets in an account, even if it is not yours (like a parent's account where you are a signatory), you must report it.

The underlying principle is financial interest or signature authority. If you have either over a foreign account, it belongs on your FBAR.

Step-by-Step: How to File FBAR Online

Filing an FBAR can feel daunting, but the process is actually quite straightforward once you have your information ready. It is an entirely electronic process.

Step 1: Collect Your Account Information

Before you log in, gather details for every foreign account you held during the year. You will need:

- The name and address of the bank or financial institution (e.g., State Bank of India, Mumbai branch).

- The account number.

- The type of account (e.g., savings, checking, mutual fund).

- The maximum value in the account during the year, converted to US dollars.

Step 2: Visit the BSA E-Filing Website

Go to the official FinCEN BSA E-Filing system website. Do not search for "file FBAR with IRS." It has its own dedicated portal.

Step 3: Register or Log In

You have two main options. You can file as an individual, which requires creating an account and password. Alternatively, a tax professional can file it on your behalf.

Step 4: Fill Out FinCEN Form 114

The form itself is a series of screens. You will enter your personal information first. Then, you will add each financial account one by one. You will input the bank details, the maximum value, and specify your ownership type (e.g., sole ownership, joint ownership).

Step 5: Submit Electronically and Get Confirmation

Once you have entered all accounts and reviewed the information, you submit the form. The system will generate a confirmation number immediately. Save this number. It is your proof that you filed on time.

I recently helped a client file his FBAR. He was worried it would take hours. Once he had his bank statements ready, we logged in and completed the entire process in about 20 minutes. The relief on his face was palpable. Having your data organized is 90 percent of the work.

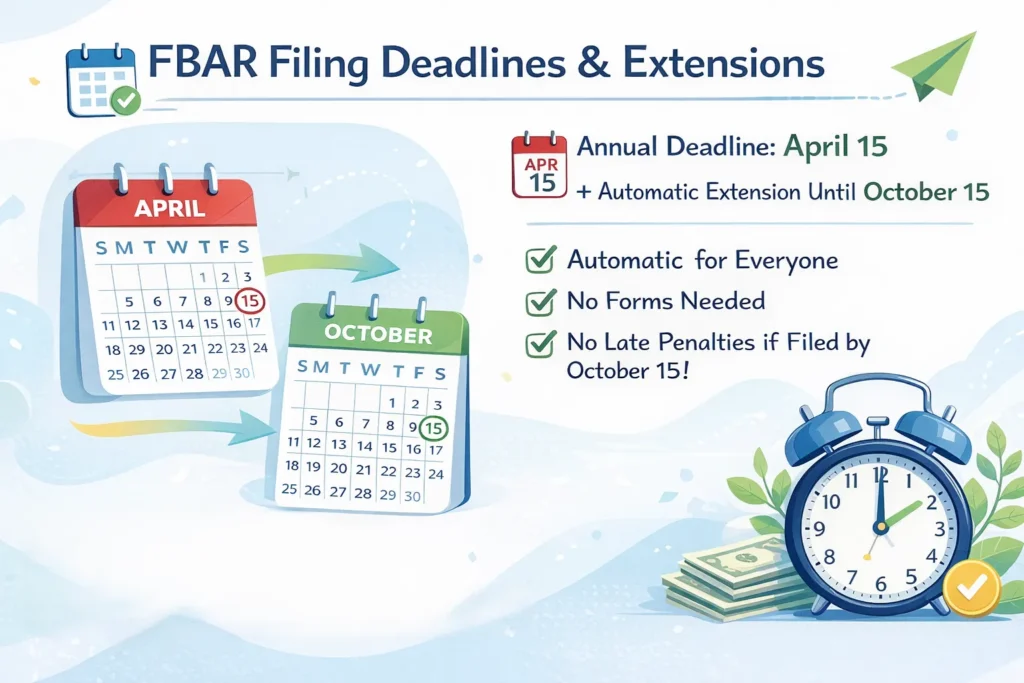

FBAR Filing Deadlines & Extensions

Staying on top of deadlines is crucial to avoid any potential penalties.

The annual FBAR deadline is April 15, which aligns with the US tax filing deadline. However, you get a generous automatic extension until October 15.

This is a key benefit. You do not need to file any forms to request this extension. It is granted to everyone automatically. If you miss the April 15 date, you have until October 15 to file without being considered "late" by the system.

This gives you extra time to gather information from your Indian banks, especially for accounts you may not check frequently.

FBAR Penalties: What Happens If You Don’t File

This is the section that causes the most anxiety. The penalties for not filing an FBAR when required can be severe. The government distinguishes between two types of failure: non-willful and willful.

| Type of Violation | Potential Penalty |

|---|---|

| Non-willful | Up to $10,000 per violation |

| Willful | Greater of $100,000 or 50% of the account balance |

| Criminal | Fines up to $500,000 and/or up to 10 years in prison |

Non-willful means you didn't know about the requirement or made a mistake. Even here, the penalties can add up quickly if you have multiple accounts over multiple years.

Willful means you knowingly and intentionally hid the accounts. The penalties here are designed to be punitive.

The good news is that the system understands people make mistakes. If you have unfiled FBARs from previous years, you should strongly consider using the IRS's Delinquent FBAR Submission Procedures. This is a voluntary disclosure program that often allows you to file the past-due forms without any penalties, as long as you were not willfully avoiding the law and you have already paid any taxes due on the income.

Do not let the fear of penalties paralyze you into inaction. The worst thing you can do is to continue not filing once you know about the requirement.

FBAR vs FATCA: What’s the Difference?

Many NRIs get confused between FBAR and FATCA. They are related, but they are two completely different reporting requirements. You may have to file both, one, or neither.

| Feature | FBAR | FATCA (Form 8938) |

|---|---|---|

| Form | FinCEN Form 114 | IRS Form 8938 |

| Threshold | $10,000 aggregate | Much higher ($50,000 - $600,000+) |

| Filed With | FinCEN (Treasury) | IRS (with your tax return) |

| Purpose | Anti-money laundering | Tax compliance |

Think of it this way. FBAR is for the US Treasury to track where your money is. FATCA is for the IRS to ensure you are paying the correct tax on the income it generates.

The biggest practical difference for you is the threshold. The FATCA filing thresholds are significantly higher and depend on your filing status and whether you live in the US. For example, a single NRI living in India only needs to file Form 8938 if their specified foreign financial assets exceed $200,000 on the last day of the year, or $300,000 at any time during the year.

It is very common for an NRI to have an FBAR filing requirement but no FATCA requirement. However, you must check both every year.

Common FBAR Mistakes NRIs Make

After years of working with the NRI community, I have seen the same simple mistakes happen again and again. Avoiding these can save you a lot of trouble.

- Ignoring NRE/NRO Accounts: "But it's an Indian account, and I live in India!" This is the most common misconception. The rules are based on your status as a US person, not your location.

- Reporting the Year-End Balance: Remember, you must report the maximum value during the year, not the balance on December 31.

- Forgetting Fixed Deposits and Mutual Funds: People often remember their savings accounts but forget their FDs and mutual fund investments. These are absolutely reportable.

- Overlooking Joint or Authority Accounts: You must report an account you co-own with your spouse or parents. You must also report an account you manage for an elderly parent, even if the money is not yours.

- Confusing FBAR with FATCA: As we just discussed, they are different. You must check your requirements for each, every year.

Here is a quick checklist to run through each year:

- Did I add up the highest balance from all my Indian bank accounts?

- Did I include my fixed deposits and mutual funds?

- Did I check any joint accounts or accounts where I am a signatory?

- Did the total cross $10,000 at any time?

- If yes, I need to file an FBAR.

FAQs on FBAR for NRIs

What does FBAR stand for?

It stands for Foreign Bank and Financial Accounts Report. Its official name is FinCEN Form 114.

Do I need to file FBAR if I have less than $10,000?

No, you do not. But remember, it is the aggregate total of all your foreign accounts. If the combined highest balance of all your accounts is $10,000 or less, you do not need to file.

What is the FBAR filing deadline?

The deadline is April 15, with an automatic extension to October 15. You do not need to request this extension.

Can I file FBAR for previous years?

Yes, you can and should. Use the BSA E-Filing system and select the correct year for which you are filing. If you have multiple missed years, you should look into the Delinquent FBAR Submission Procedures to potentially avoid penalties.

Is FBAR mandatory for NRE/NRO accounts?

Yes, absolutely. NRE and NRO accounts are foreign financial accounts and must be included in your FBAR calculation.

How is the maximum balance calculated?

Look at your monthly or quarterly account statements for the entire year. Find the highest value the account held in the local currency. Then, convert that amount to US dollars using the appropriate exchange rate for that specific date.

What happens if I miss the FBAR deadline?

If you miss the October 15 extension deadline, you should file as soon as possible. The sooner you file, the less likely you are to face penalties, especially if your failure was non-willful. The key is to act now.

0 Comments