Every year, thousands of NRIs make the same mistake. They file their income tax return in India using the wrong form. And then the notices start arriving.

Here's the thing. The Indian tax system has multiple ITR forms. Each one is meant for different types of taxpayers. If you pick the wrong form, your return gets rejected. Or worse, you get a defective return notice.

I've seen NRIs panic when this happens. They thought everything was fine. After all, they paid their taxes. TDS was deducted. What could go wrong?

Turns out, everything. This guide will help you understand exactly which ITR form you need to file. No confusion. No guesswork. Just clear answers based on your income type.

Who Is Considered an NRI for Income Tax Purposes?

Before you pick an ITR form, you need to know your residential status.

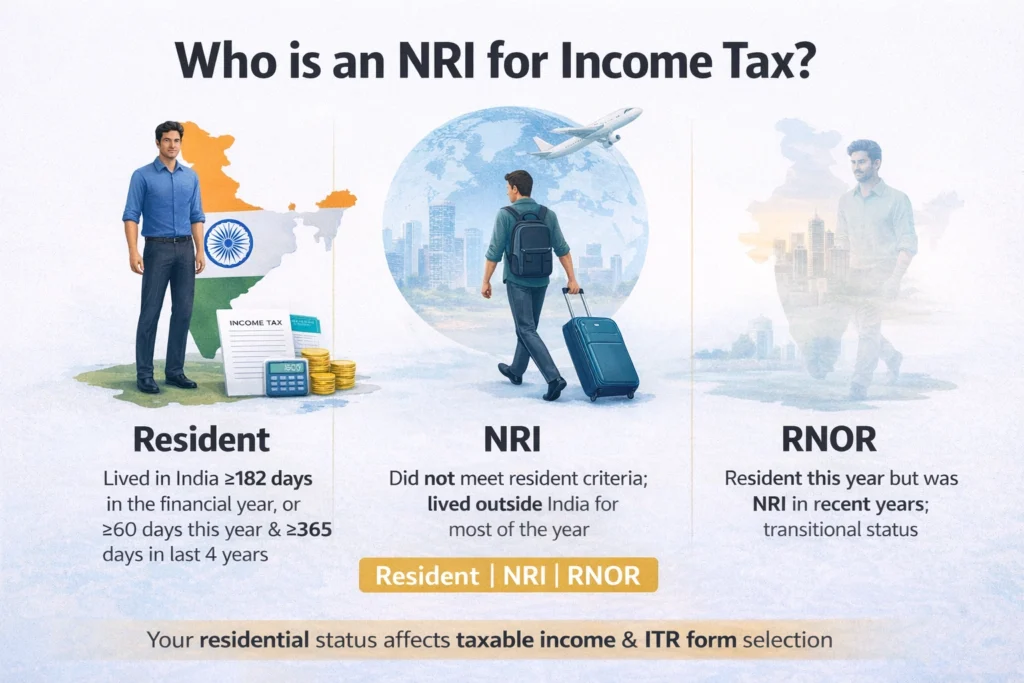

The Income Tax Act divides people into three categories:

Resident: You lived in India for 182 days or more during the financial year. Or you were in India for 60 days in that year AND 365 days in the previous four years.

Non-Resident (NRI): You don't meet the resident criteria. You lived outside India for most of the year.

RNOR (Resident but Not Ordinarily Resident): You're technically a resident this year, but you were an NRI in recent years. This is a transition status.

Your residential status decides two critical things. First, what income gets taxed in India. Second, which ITR form you can use. Most people who work abroad and have some income from India fall into the NRI category. If you're not sure about your status, check the Income Tax Department's residential status calculator online.

Here's why this matters. The ITR form you can file depends entirely on whether you're a resident or non-resident. Some forms are completely off-limits for NRIs.

Income Tax for NRIs in India – What Income Is Taxable?

As an NRI, you don't pay tax in India on your global income. You only pay tax on income that is earned or received in India.

Here are the common sources of taxable income for NRIs:

Rental income from Indian property: You own a flat in Mumbai that you're renting out. That rental income is taxable in India.

Interest on NRO accounts: Your NRO (Non-Resident Ordinary) account earns interest. That interest is taxable.

Capital gains: You sold shares in an Indian company. Or mutual funds. Or property. The profit from these sales is taxable in India.

Business income from India: If you run a business in India or have income from a partnership firm, that's taxable here.

Now, here's what's NOT taxable in India:

Foreign salary: If you work in Dubai and earn a salary there, India doesn't tax that income.

Interest on NRE and FCNR accounts: These special NRI accounts have tax-free interest. The government gives you this benefit to encourage foreign deposits.

Many NRIs assume that because TDS (Tax Deducted at Source) was already deducted, they don't need to file a return. That's wrong. You still need to file if your income exceeds the basic exemption limit. And you might need to file even below that limit if you want to claim a refund.

NRI Which ITR Form to File – Overview

Here's the most important rule upfront.

NRIs cannot file ITR-1 (Sahaj).

I'll say it again because this is where most mistakes happen. If you're an NRI, ITR-1 is not allowed for you. Period.

Most NRIs need to file either ITR-2 or ITR-3. The choice depends on your income sources.

ITR-2 is for NRIs with salary, rental income, capital gains, or interest income. ITR-3 is for NRIs with business or professional income.

There's also ITR-4, but that's generally not applicable to NRIs. We'll get to that later.

For now, remember this. Your default options are ITR-2 and ITR-3. Everything else we'll discuss builds on this foundation.

Can NRIs File ITR-1? (Most Common Confusion)

This deserves its own section because it's the biggest source of mistakes.

ITR-1 is called Sahaj. It's the simplest form. Residents with salary income, one house property, and interest income can use it.

Sounds perfect for NRIs with simple income, right?

Wrong.

The form clearly states at the top: "Not applicable for Non-Residents."

But here's why people still make this mistake. They look at their income. Maybe it's just salary and some interest. The amount is small. They think, "My situation is simple, so I should use the simple form."

That logic doesn't work with tax forms.

Even if your income is tiny. Even if you have just one source. Even if everything seems straightforward. If you're an NRI, you cannot use ITR-1.

What happens if you file ITR-1 anyway?

The return gets marked as defective under Section 139(9). You'll receive a notice asking you to file the correct form. Your original filing date won't be considered valid. This can create problems with refunds, carry-forward of losses, and your compliance record.

I know someone who filed ITR-1 for three years in a row. They didn't realize the mistake until they tried to claim a refund. The tax department rejected all three returns. They had to file revised returns, which took months to process.

Don't be that person.

ITR-2 for NRIs – When Should You Use It?

ITR-2 is the workhorse form for most NRIs.

You should file ITR-2 if you have:

Rental income from property in India. You own a house or flat that generates rent. Use ITR-2.

Capital gains. You sold shares, mutual funds, or property during the year. The profit (or loss) from these sales goes into ITR-2.

Interest income from NRO accounts. Banks deduct TDS on this interest. Report it in ITR-2.

Foreign assets to disclose. If you have bank accounts, investments, or property outside India, ITR-2 has a schedule (Schedule FA) for this disclosure.

No business or professional income. If you don't run a business or practice a profession in India, ITR-2 is your form.

Let me give you an example.

Rajesh works in Singapore. He earns a salary there (not taxable in India). But he owns two flats in Pune that he rents out. He also has an NRO account that earns interest. Last year, he sold some mutual funds and made a profit.

Rajesh needs to file ITR-2. His rental income, interest, and capital gains all fit into this form. His Singapore salary doesn't need to be reported in his Indian return.

Another example.

Priya lives in London. She doesn't have any property in India. But she invests in Indian stocks through her NRI account. Last year, she sold some shares and made 3 lakh rupees in profit.

Priya should file ITR-2 to report this capital gain.

The key thing about ITR-2 is that it's comprehensive. It covers most income situations that NRIs face. If you're not running a business, ITR-2 is probably your form.

ITR-3 for NRIs – Who Needs It?

ITR-3 is for NRIs with business or professional income.

You must file ITR-3 if you have:

Business income in India. You run a business. Maybe a shop, a manufacturing unit, or an import-export business. This income goes into ITR-3.

Professional income. You're a consultant, doctor, lawyer, or architect earning fees in India. Use ITR-3.

Income from a partnership firm. You're a partner in a firm operating in India. Your share of profit is reported in ITR-3.

Here's an important restriction. NRIs generally cannot use presumptive taxation schemes. These are simplified calculation methods available under Section 44AD and 44ADA. The tax law restricts these benefits for non-residents in most cases.

This means you need to maintain proper books of accounts. And you need to calculate your business income using the regular method.

An example will help.

Vikram lives in the US. He owns a small manufacturing business in India. His brother manages it day-to-day. The business made a profit of 8 lakh rupees last year.

Vikram must file ITR-3. His business income doesn't fit into ITR-2.

Another scenario.

Meera is a software consultant based in Canada. She has two clients in India who pay her consulting fees. She earned 12 lakh rupees from these projects.

Meera needs ITR-3 for her professional income.

The difference between ITR-2 and ITR-3 is simple. If you're earning from business or professional activities, go with ITR-3. For all other income types (salary, rent, capital gains, interest), use ITR-2.

ITR-4 for NRIs – Is It Allowed?

ITR-4 is called Sugam. It's designed for small businesses and professionals who opt for presumptive taxation.

But here's the catch. NRIs generally cannot use ITR-4.

Why? Because the presumptive taxation schemes (Section 44AD for business, 44ADA for professionals) have specific restrictions for non-residents.

Section 44AD says you can use this scheme only if you're a resident individual. NRIs don't qualify.

There might be very specific situations where an NRI could technically use ITR-4. But these are rare edge cases. For 99% of NRIs, ITR-4 is not an option.

If you have business income as an NRI, plan to file ITR-3. Don't try to squeeze into ITR-4.

Quick Table – Which ITR Form for NRI?

| NRI Income Type | Correct ITR Form |

|---|---|

| Rent plus interest | ITR-2 |

| Capital gains (shares, mutual funds, property) | ITR-2 |

| Salary from Indian employer | ITR-2 |

| Business income | ITR-3 |

| Professional income (consultant, doctor, lawyer) | ITR-3 |

| Foreign assets to disclose | ITR-2 or ITR-3 |

| Previously filed ITR-1 by mistake | File revised return with ITR-2 |

Keep this table handy. It answers the most common "which form" questions in one place.

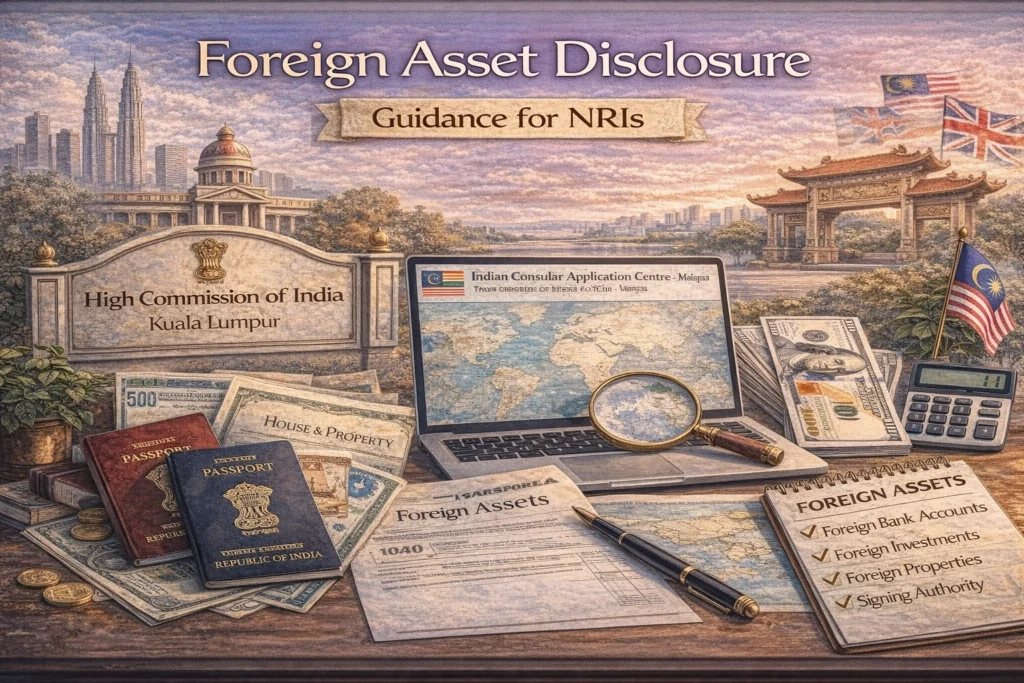

Foreign Asset Disclosure for NRIs

This is critical. And often overlooked.

If you're an NRI filing ITR-2 or ITR-3, you must fill Schedule FA (Foreign Assets).

Schedule FA is where you disclose:

Foreign bank accounts. Every account you hold outside India. Even if the balance is zero.

Foreign investments. Stocks, bonds, mutual funds, pension funds in other countries.

Foreign properties. If you own a house or land outside India.

Signing authority. Even accounts where you're just a signatory (like a joint account with a spouse) need to be disclosed.

Many NRIs skip this section. They think, "My foreign income isn't taxable in India, so why report it?"

Here's why. The Black Money Act requires this disclosure. It's not about taxation. It's about transparency.

If you don't disclose foreign assets and the tax department finds out later, penalties can be harsh. We're talking about 10 lakh rupees per asset, per year.

I know that sounds extreme. But this is a serious compliance requirement.

The good news? Reporting is straightforward. You just need the country name, account number, and peak balance during the year. You don't need to convert amounts to rupees or pay tax on them.

Just make sure you fill Schedule FA completely and accurately.

TDS Rules for NRI Income

When you're an NRI, TDS rates are generally higher than for residents.

For example:

Rent: TDS is 31.2% (including surcharge and cess) for NRIs, compared to 10% for residents.

Interest on fixed deposits: 30% plus surcharge and cess for NRIs.

Capital gains on property: 20% (for long-term gains) or 30% (for short-term gains) plus surcharge and cess.

The person or entity paying you is responsible for deducting this TDS. They then deposit it with the government.

You can check all TDS deducted on your behalf in Form 26AS. This is available on the income tax e-filing portal.

There's also a new system called AIS (Annual Information Statement). It shows even more details than Form 26AS. Including your bank interest, stock transactions, mutual fund purchases, and more.

Before filing your ITR, download both Form 26AS and AIS. Make sure all the TDS credits are showing correctly. If there's a mismatch, you might not get credit for the tax already paid.

Many NRIs are entitled to refunds. Because the TDS rate is high, and your actual tax liability after deductions might be lower. But you only get that refund if you file the correct ITR form and claim it properly.

DTAA Relief & Which ITR Form Supports It

DTAA stands for Double Taxation Avoidance Agreement.

India has these agreements with many countries. The purpose is simple. If you pay tax on the same income in two countries, you can claim relief in one of them.

For example, let's say you're an NRI living in the UK. You earn rental income from a property in India. India taxes this income. The UK also wants to tax it (because you're a UK resident and they tax global income).

Under the India-UK DTAA, you can claim relief. Usually, you pay tax in one country and claim a credit in the other.

Both ITR-2 and ITR-3 have sections where you can claim DTAA relief.

You need to provide:

- The country where you paid tax

- The nature of income

- The amount of foreign tax paid

- Details of the tax payment

If you have income that's potentially taxable in two countries, research the relevant DTAA. It can save you from paying double tax.

The key is to file the right ITR form that has the DTAA disclosure section. ITR-1 doesn't have it. Another reason why NRIs can't use ITR-1.

Common ITR Filing Mistakes Made by NRIs

Let's talk about what goes wrong.

Mistake 1: Filing ITR-1. We've covered this already. But it's worth repeating because it's so common.

Mistake 2: Ignoring foreign asset disclosure. People skip Schedule FA thinking it's optional. It's not. It's mandatory.

Mistake 3: Not reporting interest income. Some NRIs think bank interest below a certain amount doesn't need to be reported. Wrong. All income must be reported if your total income exceeds the basic exemption.

Mistake 4: Assuming TDS means compliance. Just because TDS was deducted doesn't mean you're done. You still need to file a return if your income is above the threshold. Or if you want a refund.

Mistake 5: Using resident tax slabs. NRIs don't get the benefit of the basic exemption limit that residents get. NRI taxation starts from the first rupee for certain income types. Make sure you're using the correct tax rates.

Mistake 6: Not reconciling Form 26AS. File your return based on your actual income, not just what shows in Form 26AS. But do reconcile. If TDS credits are missing, follow up with the deductor.

Mistake 7: Missing the deadline. The ITR filing deadline is usually July 31st for individuals. Missing it means late filing fees. And you can't carry forward losses if you file late.

Each of these mistakes can trigger notices, penalties, or rejection of your return. Be careful.

What Happens If NRI Files Wrong ITR Form?

Let's say you already filed. And you used the wrong form. What now?

The tax department will send you a notice under Section 139(9). This notice says your return is defective.

You'll typically get 15 days to fix it. You need to file a revised return using the correct ITR form.

Here's the problem. Until you file the correct form, your original return is not considered valid. This means:

- Refunds (if any) won't be processed

- Loss carry-forward won't be allowed

- Your filing date resets to when you submit the correct form

- You might face processing delays for months

If you ignore the defective return notice, the tax department can treat your return as not filed. This opens you up to penalties and interest on unpaid taxes.

The solution is simple. If you realize you filed the wrong form, don't wait for a notice. File a revised return immediately using the correct ITR form.

You can file a revised return anytime before the end of the assessment year or before the assessment is completed, whichever is earlier. For FY 2023-24 (AY 2024-25), you can typically revise until December 31, 2025.

How NRIs Can Choose the Right ITR Form – Step-by-Step

Here's a simple process to follow.

Step 1: Confirm your residential status: Use the Income Tax Department's calculator or count your days in India. Are you a resident or NRI this year?

Step 2: List all your Indian income sources: Write them down. Rent, interest, capital gains, salary, business income. Everything.

Step 3: Check if you have business or professional income: If yes, you're filing ITR-3. If no, move to step 4.

Step 4: Check if you have capital gains: From shares, mutual funds, or property. If yes, you're filing ITR-2.

Step 5: Check if you have rental income or foreign assets: If yes, ITR-2 is your form.

Step 6: Validate on the Income Tax portal: When you start filling the form online, the system will ask questions about your income. It will recommend a form. Cross-check this with your analysis.

Step 7: If in doubt, consult a CA: For complex situations (multiple income types, significant foreign assets, business income), get professional help.

This process takes 10 minutes. But it can save you from months of hassle with defective return notices.

Documents NRIs Need Before Filing ITR

Before you start filling your ITR form, gather these documents:

PAN card and Aadhaar status: Your PAN must be linked with Aadhaar. Check this on the income tax portal.

Form 26AS. Download from the e-filing portal. This shows all TDS deducted on your behalf.

AIS (Annual Information Statement): Also available on the portal. Shows comprehensive financial transactions.

Rental agreement and receipts: If you have rental income. You'll need property details and rent received.

Capital gains statements: Your broker or mutual fund company will provide this. Shows your buy price, sell price, and profit or loss.

Bank interest certificates: Banks issue Form 16A if TDS was deducted. Or they provide an interest certificate.

Foreign bank statements: For Schedule FA disclosure. You need account numbers and peak balances.

Previous year's ITR: Helpful for reference and to ensure consistency.

Having all documents ready before you start makes the filing process smooth. You won't have to stop midway to hunt for information.

FAQs

Which ITR form should NRI file this year?

Most NRIs file ITR-2 (for salary, rent, capital gains, interest) or ITR-3 (for business/professional income). NRIs cannot file ITR-1 under any circumstances.

Can NRI file ITR-1 if income is small?

No. ITR-1 is not applicable to non-residents, regardless of income amount. Even if you have very simple income, you must use ITR-2 or ITR-3.

Is it mandatory for NRIs to file ITR in India?

Yes, if your total Indian income exceeds the basic exemption limit (currently 2.5 lakh rupees for those under 60). You should also file if you want to claim a refund or carry forward losses.

What if TDS is already deducted on NRI income?

TDS deduction doesn't eliminate the need to file. You must still file an ITR if your income exceeds the threshold. Filing also helps you claim refunds if excess TDS was deducted.

Can NRI revise ITR after filing wrong form?

Yes. You can file a revised return using the correct ITR form. Do this as soon as you realize the mistake. Don't wait for a defective return notice.

Is foreign income reported in Indian ITR?

Foreign income (like salary earned abroad) is generally not taxable for NRIs in India. But if it's taxable (due to DTAA or specific situations), it must be reported in ITR-2 or ITR-3.

Do NRIs need to disclose foreign bank accounts?

Yes. Schedule FA (Foreign Assets) is mandatory in ITR-2 and ITR-3. You must disclose all foreign bank accounts, investments, and properties, even if the income from them is not taxable in India.

0 Comments