You open your email. There it is. "Income Tax Notice" in the subject line.

Your heart sinks. Your mind races. What did I do wrong? Am I being audited? Will there be penalties?

Take a deep breath. Here's the truth. Most income tax notices are not as scary as they seem. Many are routine requests for information. Some are just confirmations that your return was processed.

The problem? The language is formal. The section numbers are confusing. And nobody explains what you actually need to do. This guide will walk you through the most common income tax notices. Especially Section 142(1), which causes the most panic. By the end, you'll know exactly what the notice means. And what steps to take next.

Let's start by understanding what these notices actually are.

What Is an Income Tax Notice?

An income tax notice is formal communication from the Income Tax Department.

Think of it like this. You filed your tax return. The tax department reviews it. Sometimes they have questions. Sometimes they need clarification. Sometimes they just want additional documents.

That's when they send a notice.

Notices are issued for several reasons:

Missing information. You forgot to report some income. Or you didn't attach required documents.

Data mismatch. What you reported doesn't match what banks or employers reported to the tax department.

Request for clarification. Something in your return needs explanation. Maybe a large deduction. Or an unusual expense.

Processing intimation. Your return was processed. This notice tells you the result. Refund, demand, or no change.

Here's what most people don't realize. A notice is different from an intimation. And both are different from a demand.

A notice asks you to do something. Provide information. Submit documents. Explain a discrepancy.

An intimation informs you of something. Usually that your return was processed. It might include a refund or a small demand.

A demand is a bill. You owe money. It tells you how much and why.

Understanding this difference removes half the panic.

Common Types of Income Tax Notices in India

The tax department has different sections for different situations. Here are the most common ones:

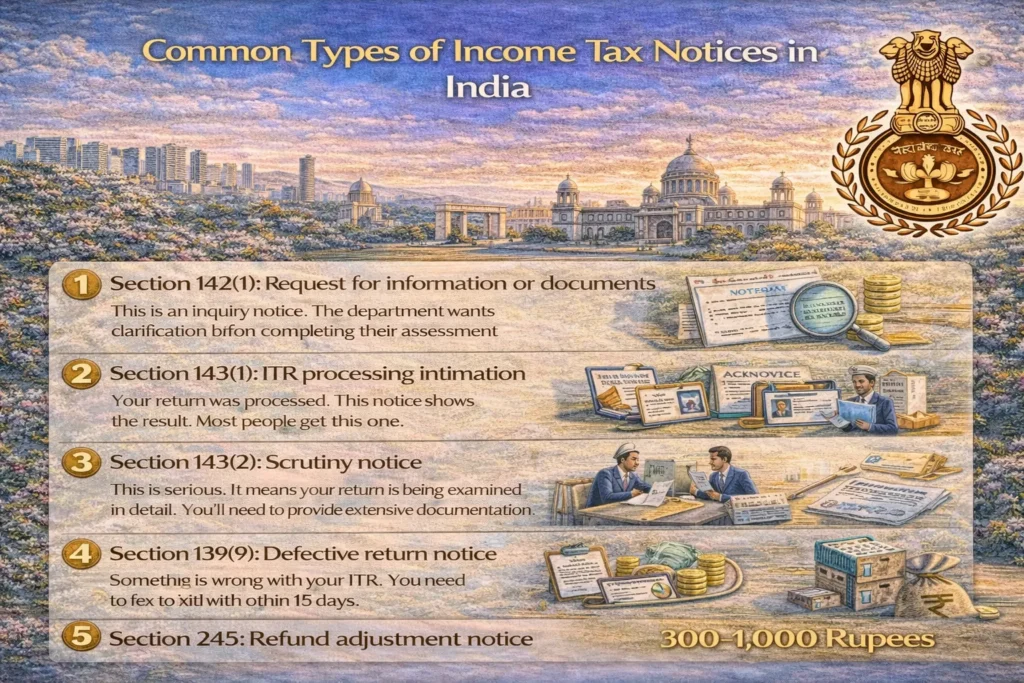

Section 142(1): Request for information or documents. This is an inquiry notice. The department wants clarification before completing their assessment.

Section 143(1): ITR processing intimation. Your return was processed. This notice shows the result. Most people get this one.

Section 143(2): Scrutiny notice. This is serious. It means your return is being examined in detail. You'll need to provide extensive documentation.

Section 139(9): Defective return notice. Something is wrong with your ITR. You need to fix it within 15 days.

Section 245: Refund adjustment notice. The department is adjusting your refund against some other demand.

In this guide, we're focusing mainly on Section 142(1) and ITR processing notices. These are what salaried employees typically receive.

What Is Income Tax Notice Under Section 142(1)?

Section 142(1) is an inquiry notice.

The Income Tax Department is asking you questions. They want additional information before they finalize their assessment of your income and taxes.

This notice can ask for:

Additional information about your income, expenses, or deductions.

Documents like bank statements, salary slips, investment proofs, or property papers.

Clarification on specific entries in your ITR.

Here's something important. Section 142(1) notices can be sent before OR after you file your ITR.

Sometimes the department sends it before filing. They're reminding you to file. Or asking why you haven't filed yet. More commonly, they send it after you file. They reviewed your return and have questions. Many people think Section 142(1) means penalty or prosecution. It doesn't.

It's simply a request. "Hey, we need more information about this. Can you explain?" The problem starts only if you ignore it.

Why You May Receive a Section 142(1) Notice

There are several common triggers.

You didn't file ITR for a particular year. Maybe you thought your income was too low. Or you forgot. The department has information suggesting you should have filed.

Mismatch between your ITR and Form 26AS or AIS. Your employer reported salary of 10 lakhs. You reported 9 lakhs. The department notices this difference.

High-value transactions. You bought property. Or sold shares worth significant amounts. Or made large investments. The department wants to verify you reported these correctly.

Missing income details. You have multiple bank accounts. Interest from one account wasn't reported. The department caught it.

Incomplete disclosures. You claimed exemptions but didn't provide adequate details.

For salaried employees specifically, here are the usual reasons:

Multiple employers in one year. You changed jobs mid-year. You received Form 16 from two companies. Did you combine both salaries in your ITR? If not, that's a red flag.

Interest income not reported. Your savings account earned 45,000 rupees in interest. You didn't report it because it was below the 50,000 rupee disclosure limit. But if your total income exceeded the basic exemption, you should have reported it.

Incorrect deduction claims. You claimed 1.5 lakhs under Section 80C. But Form 26AS shows only 1.2 lakhs in eligible investments. The department wants to know about the 30,000 rupee difference.

I know someone who received a Section 142(1) notice for this exact reason. They had claimed LIC premium deduction. But they stopped paying after three months. The actual eligible deduction was much lower than claimed.

Is Section 142(1) Notice Serious?

Let's be clear about this.

Section 142(1) itself is not a penalty notice. It's not automatic prosecution. It's not even scrutiny yet. It's a request for information. Think of it like a teacher asking you to explain your answer. They're not saying you're wrong. They just want to understand your working.

The seriousness depends entirely on how you respond. If you provide the requested information promptly and accurately, the matter usually closes. The department is satisfied. They complete the assessment. You move on.

Problems arise only if:

You ignore the notice. The deadline passes. You don't respond. Now the department will complete the assessment without your input. This is called "best judgment assessment." It's almost always against your interest.

You provide incorrect information. You fabricate documents. Or give contradictory explanations. This raises red flags and can lead to deeper investigation.

The information you provide reveals bigger issues. Maybe your explanation shows you underreported income. Or claimed wrong deductions. Now you're in more trouble than before.

So yes, take Section 142(1) seriously. But don't panic. Just respond properly.

What Should You Do After Receiving Income Tax Notice?

Let's walk through this step by step.

Step 1: Don't panic

Seriously. Read that again. Don't panic.

Most notices are routine. They're part of the normal tax administration process. Take a breath before you do anything else.

Step 2: Check the section number and assessment year

Look at the notice carefully. What section is it under? 142(1)? 143(1)? Something else?

Also check which assessment year it relates to. Sometimes you get notices for previous years. Make sure you're looking at the right year's documents.

Step 3: Log in to the Income Tax e-Filing portal

Go to the official income tax website. Log in with your credentials.

Navigate to e-Proceedings. This is where all notices and communications appear.

Step 4: Read the notice carefully

Download the PDF. Read every line.

What exactly are they asking for? Documents? Explanation? Clarification on specific items?

Don't skim. Don't assume. Read carefully.

Step 5: Note the response deadline

Every notice has a deadline. It's usually mentioned clearly.

Mark this date in your calendar. Set reminders. Missing the deadline creates unnecessary problems.

Step 6: Gather the required information

Start collecting whatever the notice asks for. Documents, statements, explanations.

Step 7: Respond through the portal

Don't email. Don't mail physical documents (unless specifically asked).

Use the e-Proceedings section to submit your response online. Upload documents there. This creates a proper record.

How to Reply to Section 142(1) Income Tax Notice Online

Here's the exact process.

Step 1: Access e-Proceedings

Log in to the income tax e-filing portal. Click on "e-Proceedings" in the dashboard.

Step 2: Find your notice

You'll see a list of all proceedings. Find the Section 142(1) notice for the relevant assessment year.

Click on it to open details.

Step 3: Read the requirements

The notice will specify what information or documents are needed.

Make a checklist. Ensure you have everything before you start uploading.

Step 4: Prepare your response

If documents are asked, scan them clearly. PDFs are usually preferred.

If explanation is needed, type it out clearly. Use simple language. Be factual.

Step 5: Upload documents

There will be an option to "Submit Response" or similar. Click it.

Upload each document. Label them clearly. "Salary_Slips_FY_2023-24" is better than "Document1."

Step 6: Add explanation if needed

There's usually a text box for additional explanations. Use it if you need to provide context for your documents.

Step 7: Submit and save acknowledgement

Once everything is uploaded, submit the response.

Download and save the acknowledgement. This is proof you responded on time.

This entire process takes 15-30 minutes if you have all documents ready.

The key is accuracy. Don't rush. Double-check everything before submitting.

Documents Commonly Asked in Section 142(1) Notices

Here's what the department typically asks for:

For salary income:

- Form 16 from employer(s)

- Salary slips for the year

- Appointment letter or offer letter

- Bank statements showing salary credits

For interest income:

- Bank statements showing interest

- Interest certificates from banks

- Fixed deposit receipts

For investments and deductions:

- LIC premium receipts

- PPF deposit receipts

- ELSS mutual fund statements

- Housing loan interest certificate

- Rent receipts for HRA claim

- Children's tuition fee receipts

For capital gains:

- Purchase and sale documents

- Broker statements

- Working calculation of gains

- Proof of indexed cost (for property)

For business income:

- Books of accounts

- Purchase and sale invoices

- Bank statements

- GST returns

General:

- PAN card copy

- Aadhaar card copy

- Address proof

- Previous year's ITR and acknowledgement

Keep all documents organized by financial year. This makes responding to notices much faster.

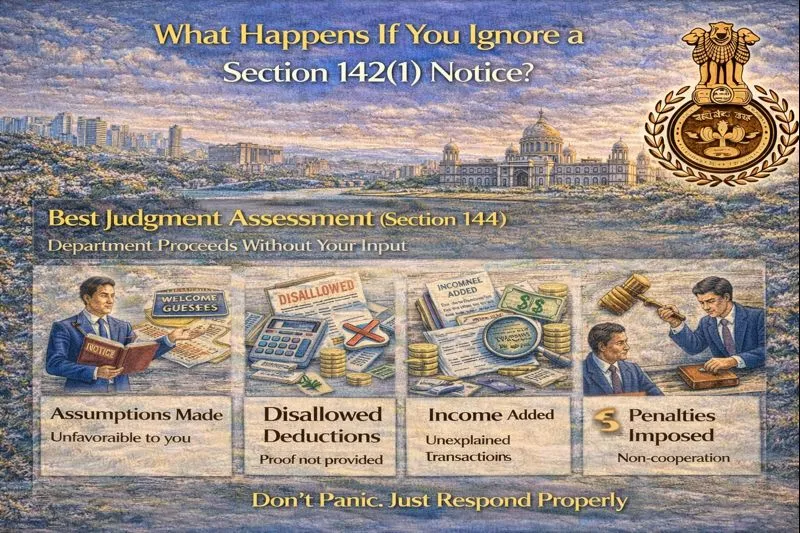

What Happens If You Ignore a Section 142(1) Notice?

This is where things get serious. If you don't respond to a Section 142(1) notice by the deadline, the department proceeds without your input. They'll complete the assessment based on whatever information they have. This is called "best judgment assessment" under Section 144.

In a best judgment assessment:

The department makes assumptions. Usually unfavorable to you.

Deductions may be disallowed. If you didn't provide proof, they won't allow the deduction.

Income may be added. If there's unexplained high-value transaction, they might add it as income.

Penalties can be imposed. For non-cooperation or concealment.

The tax demand from a best judgment assessment is almost always higher than it would have been if you'd responded. And then you're stuck. You can file an appeal. But that takes time, money, and effort. Much better to respond to the original notice.

Beyond the immediate assessment, ignoring notices creates a bad compliance record. Future scrutiny becomes more likely. Just respond. Even if you need more time, respond saying you need an extension. Don't go silent.

Common Mistakes While Responding to Income Tax Notices

People make these errors repeatedly:

Mistake 1: Missing the deadline

Life gets busy. You think you have time. Suddenly the deadline has passed.

Set multiple reminders. If you need more time, request an extension through the portal before the original deadline.

Mistake 2: Uploading incomplete documents

The notice asks for bank statements for the entire year. You upload only six months.

The notice asks for salary details. You upload Form 16 but not salary slips.

Read carefully. Provide everything requested. If you don't have something, explain why.

Mistake 3: Contradicting your earlier ITR

In your ITR, you claimed 1.5 lakhs in 80C deductions. In your response to the notice, your proof adds up to only 1.2 lakhs.

This creates more problems. The department now knows you overclaimed.

Make sure your response is consistent with what you filed. If there's an error, acknowledge it and file a revised return.

Mistake 4: Poor quality documents

Blurry scans. Photos taken in bad light. Documents where text isn't readable.

Upload clear, readable PDFs. The department needs to actually read your documents.

Mistake 5: Not seeking help when needed

Some notices are complex. Multiple years. Complicated income. Technical issues.

If you're unsure, consult a Chartered Accountant. The consultation fee is tiny compared to the cost of getting it wrong.

Mistake 6: Providing explanations that raise more questions

Keep explanations simple and factual. Don't volunteer information not asked for.

Answer the specific question. Provide the specific documents. That's it.

FAQs

Why did I receive a Section 142(1) notice after filing ITR?

The department reviewed your return and needs additional information or clarification. This is normal. It doesn't mean your return was wrong. They just need more details before completing their assessment.

Is Section 142(1) notice the same as scrutiny?

No. Section 142(1) is an inquiry or information request. Scrutiny is Section 143(2), which is more detailed and serious. 142(1) often comes before scrutiny, but responding properly can prevent scrutiny.

Can I revise my return after receiving this notice?

Yes, if you're still within the revision window. If you discovered an error, it's better to file a revised return and inform the department through the notice response.

Do salaried employees need to worry about income tax notices?

Not excessively, but yes, you should take them seriously. Salaried employees get notices for various reasons like multiple employers, unreported interest income, or data mismatches. Respond properly and you'll be fine.

How long does the department take after I submit my reply?

It varies. Usually 30 to 90 days. Sometimes longer if the case is complex or the department is backlogged. You can check the status on the e-Filing portal.

Should I consult a CA for replying to a notice?

For simple notices asking for standard documents (Form 16, salary slips), you can respond yourself. For complex notices involving multiple years, business income, or technical issues, professional help is worth it.

Also Read: How to Report Investment Income on Your Tax Return in India

Also Read: Complete Indian NRI Glossary

Also Read: Old vs New Tax Regime in India for NRIs

0 Comments