If you left the UAE amid economic turbulence and found yourself back in India longer than expected, your tax residency may have quietly changed — here's how to stay on the right side of the law.

The global uncertainty following the Dubai real estate and credit crisis has forced many Indian professionals to return home unexpectedly — often without realising that an extended stay in India can trigger full tax residency and liability on their worldwide income.

For years, Indian passport holders working in Dubai have enjoyed one of the most tax-efficient arrangements available to any professional: zero personal income tax in the UAE, combined with non-resident status in India that shields their foreign earnings from the Indian tax net. But that carefully balanced equation depends entirely on a single number — 182 days.

With the economic disruption sweeping through Dubai since mid-2025, thousands of Indian nationals have found themselves temporarily back in India — and some are approaching, or have already crossed, that critical threshold without realising the consequences.

The 182-day rule, explained

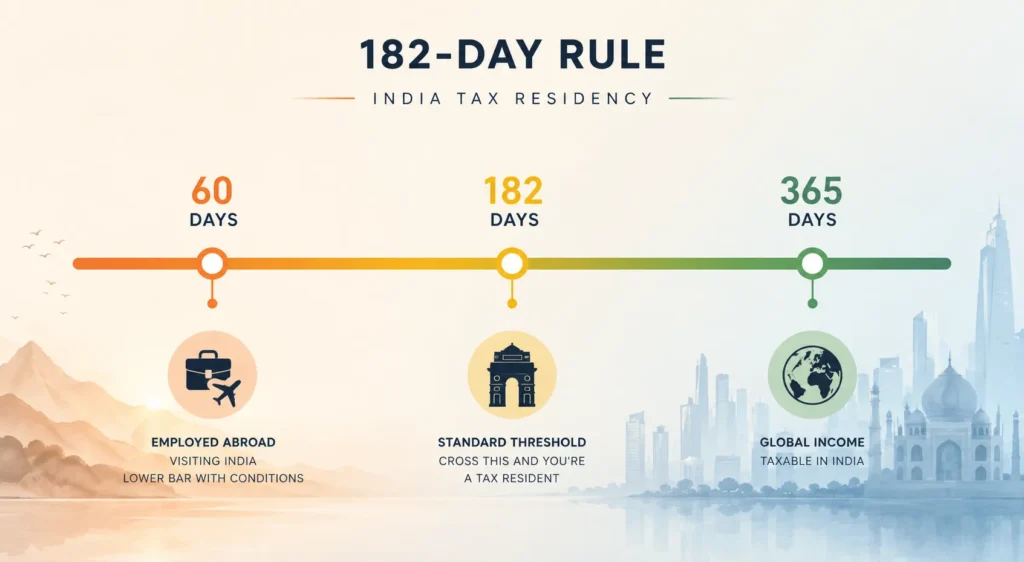

Under Section 6 of India's Income Tax Act, 1961, an individual is considered a tax resident of India for any financial year (April to March) in which they are present in India for 182 days or more. Once you cross that line, India can tax your global income — not just money earned or received in India.

60 Days

Threshold if employed abroad visiting India — lower bar with conditions

182 Days

Standard threshold — cross this and you're a tax resident

365 Days

Across four preceding years: relevant to the 60-day exception test

The relaxation that may not save you

Under a special provision, a lower 60-day threshold applies to Indian citizens who leave India for employment. But there is an important condition: if you stayed in India for 182 days or more in the preceding financial year, or if your total stay in India exceeds 365 days across the four preceding years, this relaxation does not apply.

When the 60-day relaxation applies

- You left India for employment abroad (the Dubai job qualifies)

- Your stay in India in the current year is below 182 days

- Your stay in India did not exceed 182 days in the preceding financial year

- Your total stay in India across the four preceding years was under 365 days

The critical problem for many Dubai-returned NRIs in FY 2025–26 is that the relaxation threshold is already being tested. If you returned to India in September 2025 and are still here — with no confirmed departure date because of the crisis — you may have already crossed 182 days without realising it.

What “resident” means for your taxes

Becoming a resident doesn't simply mean paying tax on Indian income. Once you cross the residency threshold, your employer's salary from the UAE, your rental income from an apartment in Dubai, interest on foreign accounts, and capital gains from overseas investments all become taxable in India — in the same year.

Important: There is no legal mechanism under the Income Tax Act to extend the 182-day limit on grounds of personal circumstances, such as economic hardship or an employer's financial collapse. The Central Board of Direct Taxes (CBDT) issued a general relaxation during the Covid-19 pandemic, but such relief is only available in officially declared exceptional circumstances — and is granted on a limited, case-by-case basis.

Can you claim the India–UAE tax treaty?

India and the UAE have a Double Taxation Avoidance Agreement (DTAA). In principle, this prevents the same income from being taxed twice. However, the treaty is not a blanket shield — it applies to specific income categories and requires you to demonstrate genuine tax residency in the UAE and actual tax paid there. If you have been physically absent from Dubai for months and have no active employment income from the UAE during your India stay, relying on the DTAA becomes legally precarious.

"Relief under the DTAA must be examined on the specific facts of each individual's case. The courts have consistently held that treaty benefits are not automatic — they must be claimed and substantiated."

The Delhi High Court ruling in the Suresh Nanda case underlines this: treaty protection depends on the actual facts of residency and income sourcing, and courts will look through arrangements that appear structured solely to claim treaty benefits.

What you should do right now

Practical steps for Dubai-returned NRIs

- Count your days precisely. Use your passport stamps and boarding passes to construct an exact count of days spent in India from April 1, 2025.

- Check the four-year look-back. Total up your India stay across FY 2021–22 to FY 2024–25. If it exceeds 365 days, the 60-day relaxation may not protect you.

- Document your UAE employment status. Even if your employer is facing difficulties, maintain correspondence, contracts, and salary records as evidence of ongoing foreign employment.

- Consult a tax advisor before March 31. If you are close to or over 182 days, a chartered accountant can help you assess the actual tax liability and plan for disclosure.

- Do not seek CBDT relief speculatively. Applications for relief due to exceptional circumstances typically require a formal representation and are not guaranteed. Seek advice before applying.

The bottom line

India's tax residency rules are mechanical and date-based. They do not accommodate good intentions, economic misfortune, or the difficulty of returning to Dubai. If you have spent more than 182 days in India this financial year, the law considers you a resident — and the obligation to declare and pay tax on worldwide income follows automatically.

The Dubai crisis has created genuine hardship for tens of thousands of Indian professionals. But navigating it without understanding the tax implications could create a second, entirely avoidable crisis when income tax filings come due. Get ahead of it now.

0 Comments