You've spent 10, maybe 15 years abroad. Built a life. Saved well. And now you're finally coming home.

The first question most returning NRIs ask is simple: "Will I have to pay Indian tax on my foreign income the moment I land?"

Most assume the answer is yes. From day one.

The reality is different. And far more generous than most people realise.

There is a transitional tax status called RNOR (Resident but Not Ordinarily Resident) that can legally keep your foreign income out of Indian tax for 2 to 3 full financial years after you return. It exists specifically for people in your situation. Most returning NRIs either don't know about it, or don't plan around it well enough to use it fully.

This guide explains what RNOR status is, who qualifies, how long it lasts, and how to actually make the most of it before the window closes.

What Is RNOR Status and Why Does It Exist?

Think of RNOR like a grace period. A buffer zone between your life abroad and your full tax life in India.

Under Indian tax law, once you become a resident, you're normally taxed on your global income. Every rupee, every dollar, every pound. But the law also recognises something important: someone who spent 12 years in Dubai or London cannot be treated the same as someone who's lived in Chennai their whole life. That wouldn't be fair.

So RNOR exists as a middle ground.

RNOR, or Resident but Not Ordinarily Resident, is a transitional tax status that allows returning NRIs to keep their foreign income tax-free in India for 2 to 3 financial years after returning, provided they meet the eligibility conditions under Section 6 of the Income Tax Act.

During this period, only your Indian income is taxable. Your foreign salary, your overseas rental income, your capital gains from foreign assets none of it is touched by Indian tax. It stays yours.

The Three Tax Residency Statuses Every Returning NRI Must Understand

Before diving deeper, let's get clarity on the three statuses. Most people only know two: NRI and Resident. The middle one is where the opportunity lives.

| NRI | RNOR | ROR (Resident and Ordinarily Resident) | |

|---|---|---|---|

| Who qualifies | Stays less than 182 days in India in a financial year | Meets specific non-residency history conditions | Does not meet RNOR or NRI conditions |

| Indian income taxable? | Yes | Yes | Yes |

| Foreign income taxable? | No | No | Yes |

| Foreign assets disclosure (Schedule FA)? | No | Yes | Yes |

The sweet spot is RNOR. You're technically a resident. You're back home. But your foreign income still stays protected, just like when you were an NRI.

Once you become ROR, the full global income taxation kicks in. That's the point of no return, so to speak. The RNOR window is what stands between your first day back and that moment.

Who Qualifies for RNOR Status: The Eligibility Conditions

This is where people get confused. But it's actually straightforward once you see it clearly.

Under Section 6 of the Income Tax Act, you qualify as RNOR if you meet either of the following two conditions:

Condition 1: You were a non-resident in 9 out of the 10 financial years immediately before the current year.

Condition 2: You were in India for 729 days or less during the 7 financial years immediately before the current year.

You only need to satisfy one. Not both.

Now, what determines whether you were a "non-resident" in any given financial year? The standard rule is: if you were in India for less than 182 days in a financial year, you're a non-resident for that year. There are also amended rules involving 120-day and 60-day thresholds for specific cases, such as Indian citizens with high foreign income, but the 182-day rule covers most returning NRIs.

The key insight: if you've genuinely lived abroad for the past several years, you'll almost certainly qualify. You don't need to calculate this to the day to know that.

A Simple Example to Check Your RNOR Eligibility

Let's say Priya moved to the UK in 2013 and returned to India in April 2024.

For FY 2024-25, we look back at the 10 preceding financial years: FY 2014-15 through FY 2023-24.

During each of those 10 years, Priya was based in the UK and visited India only for a few weeks annually. She was a non-resident in all 10 of those years. That clearly satisfies Condition 1 (non-resident in 9 out of 10 preceding years).

So for FY 2024-25, Priya is RNOR.

For FY 2025-26, we re-check. The look-back window now includes FY 2015-16 through FY 2024-25. She was still non-resident in 9 of those 10 years (she became resident only in FY 2024-25). Condition 1 still satisfied.

For FY 2026-27, she was non-resident in 8 of the preceding 10 years. Condition 1 no longer holds. Condition 2 needs to be checked. If her total India days across the preceding 7 years exceed 729, she becomes ROR.

In most cases like Priya's, the RNOR window covers 2 full financial years. Sometimes 3, depending on the return timing and travel history.

How Long Does the RNOR Window Last?

Here's the honest answer: typically 2 financial years, sometimes 3.

It depends on two things. First, how strong your NRI history is. Second, when in the financial year you return.

The financial year in India runs from April 1 to March 31. This matters more than most people realise.

If you return in April 2024 (start of FY 2024-25), you get the benefit of RNOR for potentially FY 2024-25 and FY 2025-26. That's two full years of tax-free foreign income.

If you return in February 2025 (near the end of FY 2024-25), you've already burnt most of that first financial year. You might still get two years total, but FY 2024-25 is nearly gone.

RNOR status is re-evaluated every financial year. It's not a one-time stamp on your passport. Each year, the eligibility conditions are checked fresh. The moment you stop meeting either condition, you become ROR. And from that year, your global income is fully taxable in India.

The window is real. But it doesn't wait for you to get organised.

What Income Is Tax-Free During the RNOR Period and What Is Not

Let's be very specific here, because this is where the money actually lives.

Income that is NOT taxable in India during RNOR:

- Foreign salary or employment income earned abroad

- Rental income from property located outside India

- Capital gains from selling foreign assets (stocks, property, mutual funds abroad)

- Interest earned on NRE and FCNR deposits (this continues to be tax-free)

- Any other income that is both earned and received outside India

Income that IS taxable in India during RNOR:

- Salary earned in India or for services rendered in India

- Rental income from Indian property

- Capital gains from selling Indian assets

- Interest on NRO accounts

- Any foreign income that is received directly into an Indian bank account

That last point is critical. Where the money lands matters.

If your foreign employer sends your salary directly into your Indian savings account, it may be treated as income received in India. And that can make it taxable even during RNOR. This is one of the most common traps returning NRIs walk into without realising it.

Keep your foreign income in overseas accounts or in an RFC (Resident Foreign Currency) account in India. Don't let it touch your regular Indian savings account during the RNOR period.

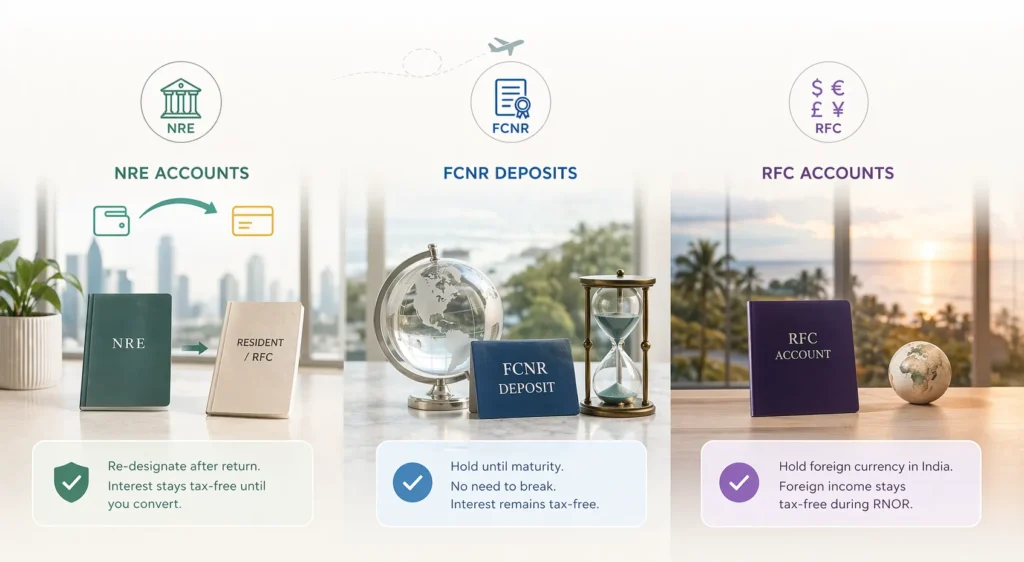

What Happens to Your NRE, FCNR, and RFC Accounts When You Return?

This is the part most returning NRIs handle badly. Not because they're careless. But because nobody told them there was a right and wrong way to do it.

NRE Accounts

Your NRE (Non-Resident External) account must be re-designated to either a resident savings account or an RFC account once you return to India permanently. Under FEMA regulations, you cannot continue operating an NRE account as an NRI once you've become a resident.

However and this is important the interest on your NRE account continues to be tax-free until you actually re-designate it. So don't rush. Converting it the day you land costs you nothing legally, but can reduce your tax-free benefit window if there's a large balance earning interest.

FCNR Deposits

Good news here. Your FCNR (Foreign Currency Non-Resident) deposits can be held until maturity even after you return. You do not have to break them. And the interest earned on these deposits remains tax-free during the RNOR period.

Let them run. Don't break them early just because you're back in India.

RFC Accounts

This is the most underused tool for returning NRIs. An RFC (Resident Foreign Currency) account can be opened once you return. It lets you hold foreign currency in India. And during the RNOR period, income in this account is tax-free.

If you're receiving ongoing foreign income let's say, rent from an overseas property, or dividends from foreign investments - routing it to your RFC account keeps it clean and outside India's tax net during RNOR.

Think of the RFC account as your tax-efficient parking spot for the RNOR years.

Practical Tips to Maximise Your RNOR Tax Window

1. Time your return for the start of a financial year

April is the best month to return. If you land in April 2025, you get all of FY 2025-26 as RNOR (assuming eligibility). Then FY 2026-27 as well. That's two full years working in your favour. A March return gives you 30 days in one financial year and then another full year. You lose an entire financial year's worth of benefit.

2. Do not receive foreign income in Indian accounts

Say it again: do not receive foreign income in Indian savings or NRO accounts during the RNOR period. Route it to overseas accounts or your RFC account. This is the single most important operational decision during the RNOR window.

3. Book capital gains from foreign assets before becoming ROR

If you have foreign stocks, overseas property, or other assets abroad that you plan to sell eventually, consider selling them during the RNOR period. Those gains won't be taxable in India then. Once you become ROR, they will be. This is basic planning, but most people miss it entirely.

4. Keep your travel and residency records clean

Your RNOR status could be questioned. Passport copies, visa stamps, travel records, overseas employment documents — keep all of these organised. If the Income Tax Department asks how many days you were in India in a given year, you want to be able to answer precisely.

5. Use DTAA and Form 67 for any cross-border tax situations

If you have income taxable in both a foreign country and India, India's DTAA (Double Taxation Avoidance Agreements) with most countries will help. You can claim foreign tax credit using Form 67 when filing your ITR, so you're not taxed twice on the same income.

The MostlyNRI team works with returning NRIs specifically on this kind of return planning. If you want a clear roadmap for your own situation, it's worth a conversation before you book your flight home.

Common Mistakes Returning NRIs Make That Cost Them Their RNOR Benefits

These mistakes are more common than you'd think. And if you've already returned without planning, this section is not here to make you feel bad. It's here to help you course-correct.

Mistake 1: Receiving foreign income in Indian bank accounts

This is the big one. The moment your overseas salary or rental income hits your Indian NRO or savings account, it looks like income received in India. Tax officers treat it that way. Keep foreign income abroad.

Mistake 2: Assuming RNOR continues automatically

RNOR is not permanent. It doesn't renew itself. Every financial year, your eligibility is tested again. Many returning NRIs assume they're still RNOR in year three without checking. By then, they may already be ROR — and filing their ITR incorrectly.

Mistake 3: Converting NRE accounts too quickly

Some people convert their NRE account to a resident savings account the week they return, thinking it's the responsible thing to do. They lose the tax-free interest benefit on the balance during a period when they didn't have to. There's no regulatory urgency to convert immediately. Take your time.

Mistake 4: Misreporting residency status in ITR

Filing as NRI when you're already RNOR, or filing as RNOR when you've crossed into ROR — both create problems. Your ITR residency status must match your actual physical presence in India for that year. Get this right every year.

Mistake 5: Ignoring Schedule FA in ITR

Once you're RNOR, you are required to disclose your foreign assets in Schedule FA of your ITR. This includes overseas bank accounts, foreign property, foreign equity. Not disclosing these is a serious compliance risk under the Black Money Act, with heavy penalties.

Frequently Asked Questions

What are the tax rules for an NRI returning to India?

When you return, you first become RNOR if you meet the eligibility conditions under Section 6 of the Income Tax Act. During RNOR, only Indian income is taxable. Foreign income stays protected. Once you become ROR (typically after 2 to 3 years), your global income becomes taxable in India. The transition is gradual, not immediate.

How can returning NRIs avoid tax on foreign income?

By qualifying for and utilising RNOR status. During the RNOR period, foreign income earned and received outside India is not taxable. The key steps are: confirm RNOR eligibility each year, keep foreign income in overseas or RFC accounts, and avoid routing foreign income into Indian bank accounts.

Do NRIs need to file an income tax return in India?

Yes, if your income in India (or total income after becoming a resident) exceeds the basic exemption limit. During RNOR, you file an ITR as RNOR and report Indian income. You also need to disclose foreign assets in Schedule FA. Even if no tax is owed, filing is advisable for documentation and compliance.

How can an NRI save tax in India?

During RNOR, the biggest saving is the foreign income exclusion itself. Beyond that, standard deductions under Sections 80C, 80D, and the basic exemption limit apply. NRIs and RNORs can also claim deductions on life insurance premiums, ELSS investments, and health insurance premiums.

What is the 4-year rule for NRIs?

This is a commonly referenced concept, not a single formal rule in Indian tax law. It broadly refers to the idea that an NRI who returns and qualifies as RNOR can expect roughly 2 to 4 financial years of transitional tax relief before becoming fully taxable as a resident. The actual duration depends on individual residency history and eligibility re-testing each year. Consult a tax advisor for your specific case.

What is the 90% rule for non-residents?

The 90% rule is sometimes referenced in the context of DTAA provisions in specific countries, where non-residents may qualify for tax treaty benefits if 90% or more of their income is taxable in their country of residence. In the Indian context, this is not a commonly applied standalone rule. If you've heard this in a specific context, verify it with a qualified NRI tax advisor.

Does an NRI need to declare foreign income in ITR?

During NRI status, foreign income is not taxable in India and does not need to be reported in ITR. During RNOR, foreign income is still not taxable, but foreign assets must be disclosed in Schedule FA. Once you become ROR, foreign income must be reported in full.

How do you reduce tax on foreign income?

The most effective way during the return phase is RNOR status. Beyond that, India's DTAA with most countries helps avoid double taxation. If you're taxed in a foreign country on income also assessable in India, you can claim a foreign tax credit using Form 67 in your ITR, reducing your net India tax liability.

What is the 60% trap?

This refers to a situation where an Indian citizen living abroad has income exceeding Rs. 15 lakhs from Indian sources and spends between 120 and 182 days in India in a financial year. In such cases, the 60-day rule (normally used to determine residency) gets replaced by a 120-day threshold, potentially making the person a resident earlier than expected. This can catch NRIs off guard during their final years abroad. If you visit India frequently and earn significant Indian income, track your day count carefully.

0 Comments