The flights are booked. The kids' school admissions are sorted. The shipping container is packed.

And then someone asks: "Have you spoken to a tax advisor yet?"

Blank stare.

Most NRIs spend months planning the logistics of moving back to India. The financial and tax side? That gets pushed to "I'll figure it out once I land." And that's exactly where the problem starts. Because RNOR benefits — the legal window that keeps your foreign income tax-free for 2 to 3 years after return — are not automatic. They depend on eligibility, timing, how you handle your accounts, and what you do with your income during that window.

This is a phase-wise RNOR checklist for returning NRIs. It covers what to do 12 to 18 months before you return, what to action at the time of arrival, and what to manage during the RNOR window itself. Follow it in sequence and you protect every rupee of your foreign income legally.

Quick Recap: What Is RNOR and Why Does the Checklist Matter?

RNOR stands for Resident but Not Ordinarily Resident. It is a transitional tax status under Section 6 of the Income Tax Act that sits between NRI and full resident status.

Here is why it matters. The moment you become a full resident (called ROR — Resident and Ordinarily Resident), India taxes your global income. Everything. But during the RNOR period, only your Indian income is taxable. Foreign income stays protected.

The window typically lasts 2 to 3 financial years after return. But it is not handed to you automatically. You have to qualify, document it, and manage it correctly. One wrong move — like routing foreign salary into your Indian savings account — and the benefit disappears.

For a detailed explanation of RNOR eligibility and how the window works, read our full guide on RNOR status for returning NRIs.

Here is exactly what you need to do, phase by phase.

Phase 1: Before You Return (12 to 18 Months Out)

This is the phase most NRIs skip entirely. And it is the most valuable one.

Think of it like packing for a long trip. The people who pack two weeks early always travel better than those who throw things into a bag at midnight. The financial preparation for return works the same way. The decisions you make 12 to 18 months before landing have more impact than anything you do after.

To maximise RNOR benefits, returning NRIs must plan in three phases: before returning (calculate eligibility and time the move), at the time of return (update accounts and open RFC), and during the RNOR window (file ITR correctly, report foreign assets, and manage income sources strategically).

1. Calculate your RNOR eligibility now, not later

Pull out your passports. Count your non-resident years over the past 10 financial years. Check your total India days over the past 7 financial years. You qualify as RNOR if you were a non-resident in 9 out of the last 10 financial years, OR if your total India stay was 729 days or less in the last 7 financial years.

Why it matters: If you're borderline on either condition, you need to know now — while you still have time to adjust travel plans.

2. Choose your return date strategically

India's financial year runs from April 1 to March 31. Returning in April gives you the maximum number of RNOR years. Returning in February or March effectively wastes that financial year's RNOR benefit.

Why it matters: The difference between an April return and a March return can mean one full extra financial year of tax-free foreign income. That could be lakhs.

3. Watch your India visits in the pre-return years

Every day you spend in India counts toward the 729-day threshold. If you are visiting India frequently in the 2 to 3 years before your final return, you may be eating into your RNOR eligibility without realising it.

Why it matters: Crossing 729 days in the preceding 7 years can cost you RNOR status — or shorten its duration significantly.

4. Review your foreign income streams and consider realising gains before return

Do you have foreign stocks, overseas property, or other assets you plan to sell? Consider selling them while you are still based abroad. Capital gains from foreign assets are not taxable in India during RNOR, but it is cleaner to book them before the transition begins.

Why it matters: Once you become ROR, capital gains from foreign assets are fully taxable in India. Realising them during the RNOR window — or before returning — is better planning.

5. Stop routing foreign income into Indian accounts right now

If your overseas salary, rental income, or dividends are currently going directly into an Indian bank account — stop that arrangement. Re-route to your overseas account or an NRE account.

Why it matters: Income received in Indian accounts can be treated as income received in India, making it taxable even during RNOR. This is one of the most avoidable mistakes.

6. Organise your travel history records

Collect passport copies showing all entry and exit stamps. Get your visa records in order. If you have multiple passports from the same period, keep all of them. Also gather foreign employment contracts, overseas tax return filings, and proof of overseas residence.

Why it matters: If the Income Tax Department questions your RNOR status, your travel history is your primary evidence. You want this ready, not buried in a drawer.

Phase 2: At the Time of Return (Month of Arrival and First 90 Days)

You've landed. The boxes are being unpacked. And your financial to-do list is already waiting.

This phase is about getting your accounts and registrations aligned correctly. The sequence matters here. Do things in the wrong order and you could trigger unnecessary tax on income that should have been protected.

1. Inform your bank about your return

This is legally required under FEMA. You must inform your bank that you have returned to India permanently. Your NRE account cannot continue as-is once you're a resident. The bank will guide you on re-designation.

Why it matters: Failing to inform the bank does not make the problem go away. It creates a FEMA compliance issue on top of everything else.

2. Open an RFC (Resident Foreign Currency) account

This is the most underused tool for returning NRIs. An RFC account lets you hold foreign currency in India legally. During the RNOR period, the interest on RFC deposits is tax-free. If you are still receiving foreign income — rent from overseas property, dividends, freelance payments — route it here.

Why it matters: RFC accounts are specifically designed for this transition period. They protect your foreign currency income while you figure out the long-term plan.

3. Do NOT convert NRE to NRO prematurely

NRO account interest is taxable. NRE account interest, until re-designation, is still tax-free. Converting your NRE to NRO the day you land is a common and costly mistake.

Why it matters: You lose tax-free interest income unnecessarily by moving too fast. The right move is to convert NRE to RFC or a resident savings account — not NRO.

4. Do not break FCNR deposits

Your FCNR (Foreign Currency Non-Resident) deposits can be held until maturity even after you return. The interest on FCNR deposits remains tax-free during the RNOR period.

Why it matters: Breaking FCNR early costs you both the deposit benefit and the tax-free interest. Leave them untouched until they mature.

5. Update your KYC and residential status everywhere

This includes every bank, mutual fund registrar (CAMS and KFintech), demat account provider, insurance company, and any other financial institution. Update your status from NRI to Resident across all of them.

Why it matters: Mismatched KYC status creates compliance problems and can flag your accounts for scrutiny.

6. Update PAN records and Aadhaar address

If your Aadhaar still shows an overseas address, update it. Ensure your PAN is linked correctly and that your residential address reflects your return.

Why it matters: Your PAN and Aadhaar are the backbone of your India tax identity. Keep them clean and current.

Which Accounts to Convert, Keep, or Open: A Quick Reference

| Account Type | What to Do at Return | Why |

|---|---|---|

| NRE Account | Re-designate to RFC or resident savings account | Cannot legally remain as NRE once you are resident; but do NOT convert to NRO |

| NRO Account | Can be retained as a resident savings account | NRO interest is taxable; do not route foreign income here |

| FCNR Deposit | Hold until maturity — do not break early | Interest remains tax-free during RNOR; breaking early loses this benefit |

| RFC Account | Open one immediately after return | Designed for returning NRIs; holds foreign currency; interest tax-free during RNOR |

| Indian Savings Account | Use for India expenses and income only | Foreign income deposited here may be treated as Indian income and taxed |

The golden rule: keep foreign income in foreign accounts or your RFC account for as long as possible during the RNOR period. The moment it touches your regular Indian savings account, you risk its tax-free status.

Phase 3: During the RNOR Period (First 2 to 3 Financial Years After Return)

The window is open. Now you have to manage it actively.

This is not a "set it and forget it" situation. Every financial year during RNOR requires deliberate action on taxes, investments, and income management. Most people who lose RNOR benefits do not lose them before returning. They lose them during this phase, through careless mistakes that were entirely avoidable.

1. File your ITR every year — as RNOR, not NRI or ROR

Your residency status in your ITR must be accurate. You are no longer an NRI. But you are also not yet a full resident (ROR). Select RNOR as your status in the ITR form each year during this period.

Why it matters: Filing as NRI when you are a resident is incorrect and can attract notices. Filing as ROR when you are RNOR means you may overpay tax on foreign income unnecessarily.

2. Report all foreign assets in Schedule FA

Schedule FA (Foreign Assets) in the ITR must be filled every year once you are RNOR. This includes overseas bank accounts, foreign property, foreign equity holdings, and any other assets held outside India.

Why it matters: Non-disclosure of foreign assets under the Black Money (Undisclosed Foreign Income and Assets) Act attracts penalties up to Rs. 10 lakhs per asset per year. This is not a formality to skip.

3. Re-check RNOR eligibility every April

Each new financial year, run the eligibility test again. Count your non-resident years in the preceding 10. Count your India days in the preceding 7. Do not assume the RNOR status continues automatically.

Why it matters: The year you stop qualifying but still file as RNOR is a compliance problem waiting to happen. Catch it early, not after a tax notice.

4. Use this window to remit and restructure foreign savings

The RNOR period is the best time to bring money from abroad to India in a tax-efficient way. You can remit foreign savings — from overseas accounts or maturing FCNR deposits — to your RFC or resident accounts without triggering Indian income tax, since these are capital remittances, not income.

Why it matters: Once you become ROR, investment income generated by those foreign funds will be taxable. Getting the funds into the right Indian structures before ROR saves ongoing tax.

5. Use DTAA and Form 67 for any income taxed in both countries

If you have income that is taxable both in a foreign country and in India (for example, some types of pension or investment income), use India's DTAA (Double Taxation Avoidance Agreement) with that country. Claim a foreign tax credit using Form 67 when filing your ITR.

Why it matters: Without Form 67, you pay full tax in both countries. With it, you offset the foreign tax against your India liability.

6. Start shifting investments to Indian products systematically

Use the RNOR years to gradually move your portfolio into Indian mutual funds, fixed deposits, equity, or real estate — in a tax-efficient sequence. Do not try to do everything in year one.

Why it matters: A planned investment shift avoids large taxable events in a single year and sets you up for a clean ROR transition.

If you want a personalised roadmap for your specific return — including account sequencing, income routing, and investment timing — the MostlyNRI team can help you build one before you land.

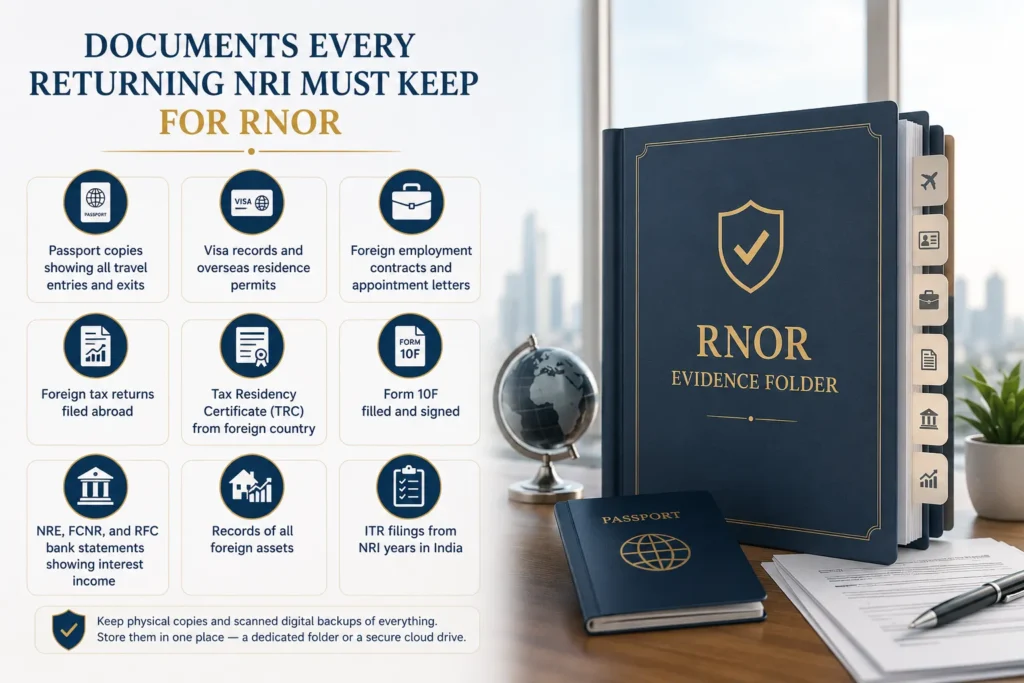

Documents Every Returning NRI Must Keep for RNOR

Think of this as your RNOR evidence folder. Keep physical copies and scanned digital backups of everything below. Store them in one place — a dedicated folder or a secure cloud drive.

- Passport copies showing all travel entries and exits across the RNOR eligibility years

- Visa records and overseas residence permits for all countries where you lived

- Foreign employment contracts and appointment letters confirming your overseas work

- Foreign tax returns filed abroad for each year of NRI status

- Tax Residency Certificate (TRC) from the foreign country — essential for DTAA claims

- Form 10F filled and signed — required alongside TRC for DTAA treaty benefits

- NRE, FCNR, and RFC bank statements showing interest income during the RNOR period

- Records of all foreign assets — property documents, overseas investment statements, shareholding certificates

- ITR filings from the NRI years in India, showing income and tax paid

If the Income Tax Department ever questions your RNOR status or your foreign asset disclosures, this folder is your defence. Keep it updated every year, not just once.

What Happens When RNOR Ends: Preparing for Full Residency

At some point, the window closes. You re-check eligibility in April, and this time, you don't qualify as RNOR anymore. You are now ROR — Resident and Ordinarily Resident. And from that year, your global income is fully taxable in India.

This transition is not a cliff edge. But it does require preparation — ideally starting 6 months before the expected end of RNOR.

Here is what to do before the window closes.

Finalise the liquidation of foreign assets you were planning to sell. Capital gains from foreign assets during RNOR are not taxable in India. After ROR, they are. If you have been sitting on the fence about selling overseas property or closing foreign investment accounts, act before RNOR ends.

Route remaining foreign income into India or stop it altogether. Any foreign income still flowing after you become ROR will be taxable. Either restructure the investment to stop generating income, or accept that it will now appear in your India ITR.

Step up your Schedule FA reporting discipline. As ROR, your foreign asset disclosure obligations continue — and the scrutiny generally increases. Make sure every foreign account, property, and investment is correctly disclosed each year.

Engage an NRI tax advisor well before the end of RNOR. Do not wait until you have already become ROR to start planning. The decisions you make in that 6-month window before transition can significantly reduce your ongoing tax burden.

The MostlyNRI advisory team works with returning NRIs specifically on this end-of-RNOR transition planning. If you are 12 to 18 months away from that shift, this is the right time to talk.

Frequently Asked Questions

How do I maintain RNOR status in India?

RNOR status is not something you actively "maintain" — it is a status you either qualify for or you don't, based on your residency history. Each financial year, you check whether you were a non-resident in 9 of the previous 10 years, or whether your India days in the preceding 7 years were 729 or less. If you meet either condition, you are RNOR for that year. You cannot artificially extend it, but you can avoid mistakes that cause you to misfile.

Can an RNOR maintain an NRE account?

No. Once you become a resident in India (including RNOR status), you cannot legally maintain an NRE account under FEMA regulations. You must re-designate the NRE account to a resident savings account or an RFC account. The interest already earned on the NRE account during the NRI period and until re-designation remains tax-free, but you cannot continue adding funds to it as a resident.

Does an RNOR need to declare foreign income?

Foreign income does not need to be reported as taxable income during RNOR — it is exempt. However, the foreign assets generating that income must be disclosed in Schedule FA of your ITR every year. Exemption from taxation does not mean exemption from disclosure. Failing to report foreign assets attracts serious penalties under the Black Money Act.

What are the advantages of RNOR status?

The primary advantage is that foreign income — salary, rental income, capital gains, and investment income from abroad — is not taxable in India during the RNOR period. Interest on NRE and FCNR deposits also continues to be tax-free. This gives returning NRIs a genuine window to transition their finances from an overseas structure to an India-based one without an immediate global income tax hit.

How long is the RNOR period in India?

Typically 2 to 3 financial years, depending on your residency history and when you return. The exact duration varies because RNOR eligibility is re-tested every financial year. Returning in April (start of financial year) generally gives you the longest possible RNOR window. Once you no longer meet either eligibility condition, you transition to ROR.

Can I lose my RNOR status?

Technically, RNOR is not something you "lose" — you simply stop qualifying for it once your residency history no longer meets the conditions. However, you can effectively waste or reduce your RNOR window by returning mid-financial year, by miscounting your India days in prior years, or by filing the wrong tax status in your ITR. You cannot voluntarily give up RNOR — if you qualify, that is your correct legal status.

How long can an NRI account be maintained after returning to India?

Under FEMA, an NRE account must be re-designated to a resident account or RFC account within a reasonable time after becoming a resident. There is no fixed statutory deadline in days, but the general expectation is within a few months of return. FCNR deposits are an exception — they can be held to maturity even after you become a resident. Continuing to hold an NRE account as a resident without re-designation is a FEMA violation.

What is the difference between NRI and RNOR?

An NRI is someone who is not a resident of India in a financial year (typically spending less than 182 days in India). An RNOR is someone who is a resident (physically present in India enough to qualify as resident) but whose residency history is primarily overseas. The key tax difference: NRIs are taxed only on Indian income. RNORs are also taxed only on Indian income — plus they must disclose foreign assets. It is only when you become a full ROR that global income becomes taxable in India.

What is the 90% rule for non-residents?

This rule appears in certain DTAA treaties, particularly in the context of treaty country residents who earn most of their income in that country. It is not a core Indian Income Tax Act concept, but it is sometimes relevant when claiming treaty benefits. In a few treaties, a non-resident can claim specific deductions or exemptions if 90% or more of their total income originates from the treaty country. If this is relevant to your situation, verify it with a qualified advisor who knows the specific treaty applicable to your country of residence.

Also read: RNOR vs NRI vs Resident: Which Tax Status Saves You the Most When Moving Back to India?

Also read: How NRIs Can Use Paytm for International Transactions

0 Comments