If you’re an NRI exploring ways to invest in India, mutual funds are likely one of the first options that pop up. They’re widely accessible, professionally managed, and come with the potential for strong long-term returns.

But here’s the problem: the sheer number of mutual funds available can be overwhelming. Even more confusing are the rules, tax implications, and account requirements that come with investing as a non-resident.

You’re not alone in this confusion. Many NRIs are eager to participate in India’s growth story but don’t know where to begin. This guide is designed to give you clarity. It introduces eight mutual funds that we believe stand out for NRI investors in 2025. Each fund was selected after considering key factors such as historical performance, risk level, fund strategy, taxation, and how suitable it is for NRE and NRO account holders.

But we’re not just handing you a list. This guide explains why each fund was chosen, what kind of investor it suits, and what you should know before making any investment. Whether you’re a cautious investor looking for stable debt options or someone seeking long-term growth through equities, this article will help you make more confident, informed decisions.

Why NRIs Should Consider Investing in Indian Mutual Funds

NRIs often wonder whether it’s worth investing in mutual funds back home, especially when they already have investment opportunities in their country of residence. The answer, for many, is a firm yes. There are several reasons why mutual funds in India can be a smart addition to your financial portfolio, even when you live overseas.

First, investing in India gives you exposure to a different currency and economy. This can be a smart move for managing currency risk. For example, if you’re earning in dollars, pounds, or dirhams, putting some of your investments in Indian rupees helps diversify your financial exposure. It’s like not putting all your eggs in one currency basket.

Second, India’s economy is growing. The country’s large population, expanding middle class, and digital transformation create an environment for businesses to grow. Mutual funds allow you to benefit from this trend through professional fund managers who make investment decisions for you.

And third, mutual funds are relatively easy to access for NRIs. Most fund houses allow you to invest using your NRE or NRO account, and many now offer online onboarding through video-based KYC. You can also set up SIPs (Systematic Investment Plans) to invest regularly, just like residents in India.

Mutual funds offer a simple, diversified, and potentially high-growth way to invest in India, without the need to directly buy and track individual stocks.

Key Things NRIs Must Understand Before Investing

Before jumping into mutual fund investments in India, it’s important to understand the groundwork that needs to be in place. There are a few extra steps involved for NRIs compared to resident Indians.

The first and most important step is to complete your KYC, or Know Your Customer, process. This includes verifying your identity, address, and NRI status. Fund houses now offer online and video KYC options, but the process may still take a few days and often requires documentation like your passport, visa, and overseas address proof.

Next, your mutual fund investments must be linked to either an NRE (Non-Resident External) or NRO (Non-Resident Ordinary) account. An NRE account allows you to invest in India with full repatriation of both principal and interest, meaning you can take the money back to your country of residence without restrictions. An NRO account, on the other hand, is generally used for income earned in India, and repatriation is capped at USD 1 million per financial year (with proper documentation).

It’s also crucial to understand tax and repatriation rules. NRIs are subject to tax on capital gains in India, and tax is typically deducted at the time of redemption (TDS). Additionally, not all mutual fund companies accept investments from NRIs living in certain countries like the USA and Canada due to compliance constraints.

In short, you should have your documents in place, your bank accounts correctly linked, and a good understanding of how taxes and withdrawals will work. Once these basics are covered, you can move forward with much greater confidence.

The 8 Best Mutual Funds for NRIs in 2025

Choosing mutual funds isn’t just about chasing the highest return. It’s about selecting funds that match your risk profile, investment goals, and timeline. Below are eight funds we’ve identified as top picks for NRIs this year, based on performance, management quality, and suitability for non-resident investors.

Parag Parikh Flexi Cap Fund

This is a unique fund in the Indian market because it combines Indian equities with global stocks like Alphabet (Google), Amazon, and Meta. This hybrid model provides geographical diversification along with the flexibility to invest across different market capitalizations. It’s suitable for NRIs who want exposure to Indian growth but also want to cushion their portfolio with international holdings. With a strong track record and a conservative, long-term approach, this fund is ideal for globally-minded investors.

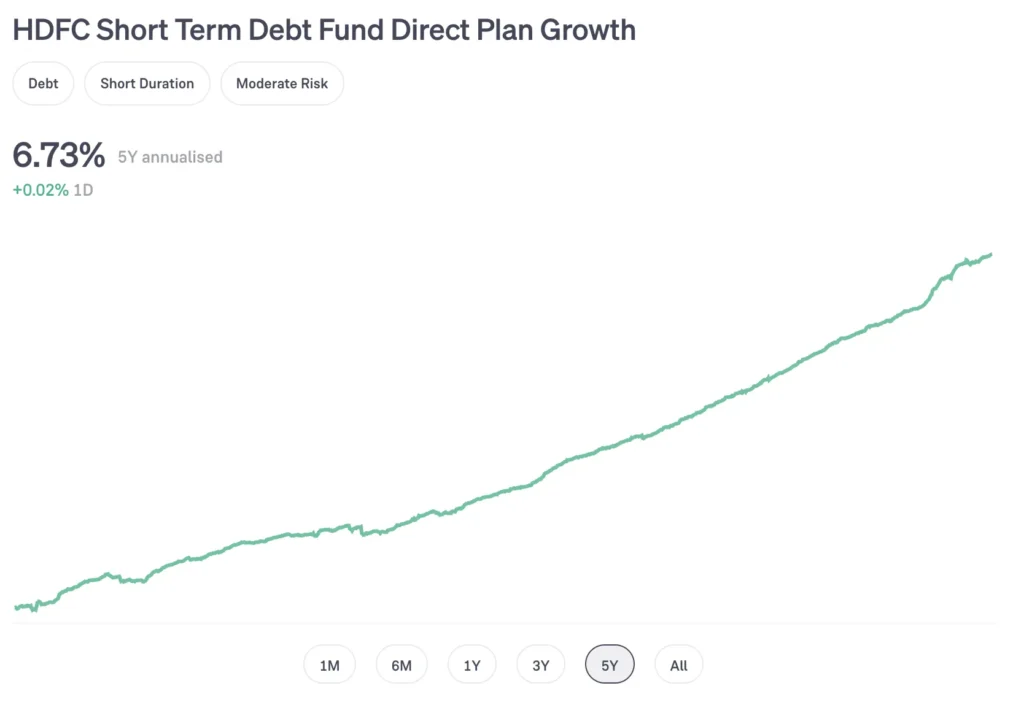

HDFC Short Term Debt Fund

If you’re a conservative investor who prefers stable returns with minimal risk, this short-term debt fund is worth considering. It primarily invests in high-quality corporate bonds and government securities. The interest rate sensitivity is lower because of its short duration, which makes it a great parking place for your funds for 1 to 3 years. This fund is particularly useful for NRIs who want predictable income or are planning to repatriate funds in the near term.

Axis Small Cap Fund

This is not a fund for the faint-hearted. The Axis Small Cap Fund focuses on smaller companies with high growth potential, but also comes with high volatility. If you’re young, have a long investment horizon, and are willing to ride out market ups and downs, this fund could deliver strong returns. It’s a good fit for NRIs looking to be aggressive with a portion of their portfolio, aiming to create wealth over 7–10 years or more.

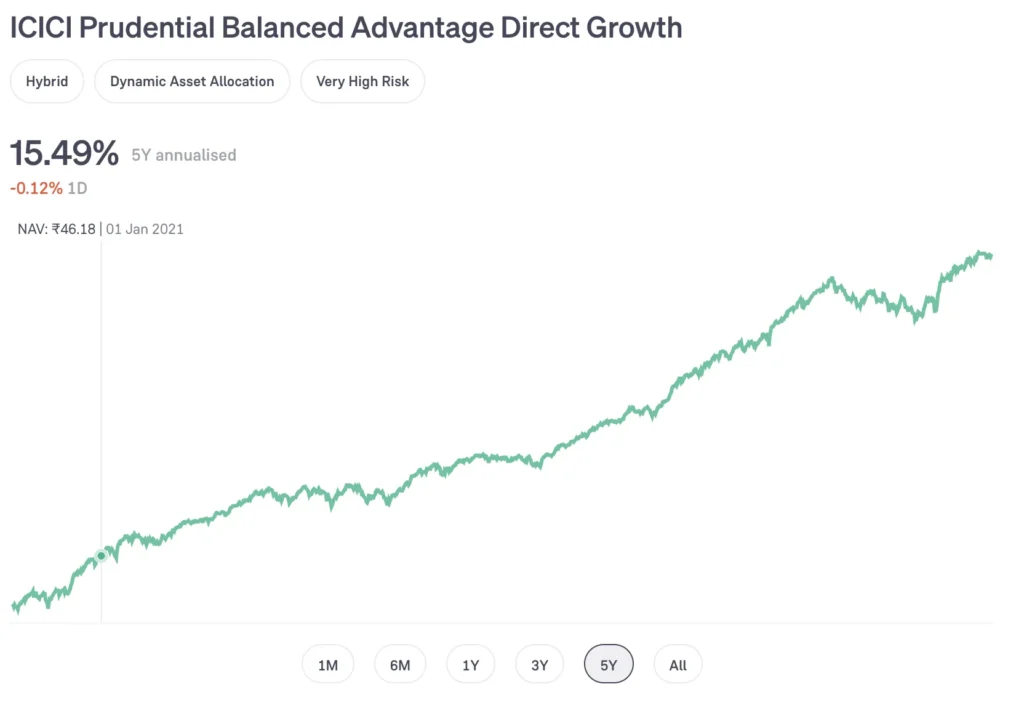

ICICI Prudential Balanced Advantage Fund

One of the most popular balanced funds in India, this fund dynamically shifts between equity and debt depending on market valuations. That means it takes more equity exposure when the market is undervalued and moves to debt when markets seem overheated. This makes it a good “middle-path” fund, offering decent returns with relatively lower risk. It’s suitable for NRIs who want moderate growth with less market anxiety.

Nippon India ETF Nifty 50 BeES

If you believe in the long-term story of India’s top companies and prefer a passive, low-cost investment style, this ETF could be perfect for you. It tracks the Nifty 50 Index and doesn’t try to beat the market. Instead, it mimics the performance of the top 50 listed companies in India. With a low expense ratio and high transparency, this is a smart option for NRIs who want to keep things simple and cost-effective.

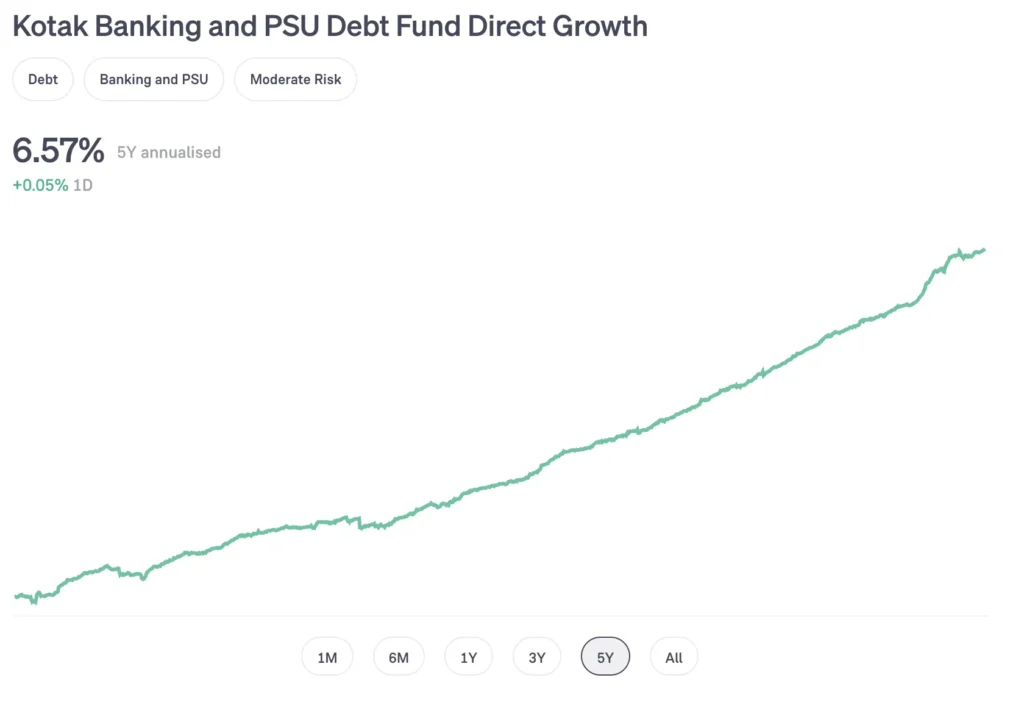

Kotak Banking & PSU Debt Fund

This fund is designed for safety-first investors. It primarily invests in bonds issued by Indian banks and public sector undertakings (PSUs), which are considered less risky. The returns are modest but stable, making it ideal for NRIs who want to preserve capital and receive predictable returns without worrying about credit risk.

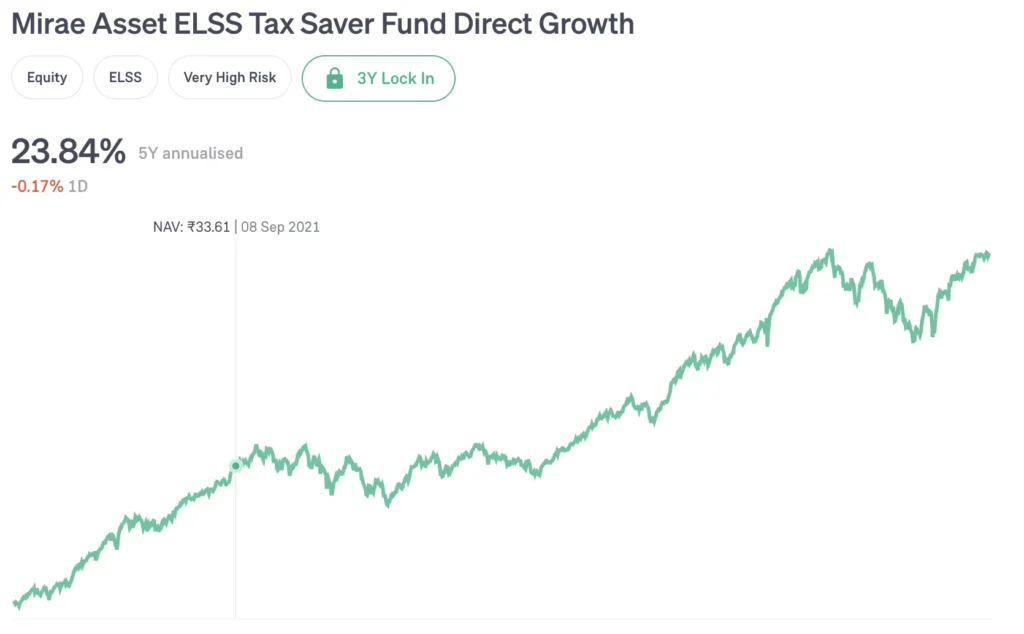

Mirae Asset Tax Saver Fund (ELSS)

This fund offers two advantages: strong equity-based growth and tax savings under Section 80C of the Indian Income Tax Act. It comes with a mandatory three-year lock-in period, which encourages disciplined, long-term investing. With consistent outperformance and a reasonable risk profile, it’s a good option for NRIs who also need to take care of tax planning.

SBI Bluechip Fund

This large-cap equity fund focuses on stable, well-established companies. It offers relatively lower volatility compared to mid- or small-cap funds, making it a great choice for NRIs looking for steady long-term growth. The fund is known for its disciplined investment approach and has delivered consistent returns over the last five years. It’s a solid fit for long-term goals like retirement or children’s education.

How We Selected These Funds

The funds listed above were not chosen at random. We looked at several key parameters to ensure each recommendation adds real value for NRI investors. These included long-term performance consistency, the experience of fund managers, transparency, expense ratios, and how well each fund aligns with the practical realities of NRI investing, such as NRE/NRO account compatibility and ease of repatriation.

We also considered a mix of equity and debt strategies to cater to different risk appetites. Some investors prefer stability, while others seek growth. The list reflects that diversity.

Understanding Tax Implications for NRIs

Taxation is one of the most misunderstood aspects of NRI investing. It’s not just about what you earn but also about how much you keep after taxes. In India, mutual fund gains are taxed at the time of withdrawal, and for NRIs, tax is deducted at source (TDS).

For equity mutual funds, if you sell your units after holding them for more than one year, the gains are considered long-term and taxed at 10% (above ₹1 lakh in gains). If sold within a year, short-term capital gains apply at a 15% rate. For debt funds, short-term gains (held under 3 years) are taxed at your applicable slab rate, while long-term gains (held over 3 years) are taxed at 20% with indexation benefits.

NRIs also need to factor in repatriation limits. If your mutual fund is linked to an NRO account, there is a cap on how much money you can send back abroad – USD 1 million per financial year, subject to documentation and approval from your bank. With NRE-linked investments, this limitation doesn’t apply.

You may also be eligible to claim tax relief under the Double Taxation Avoidance Agreement (DTAA) between India and your country of residence. It’s best to consult a tax advisor to ensure you’re complying with both Indian and foreign laws.

Building a Balanced Mutual Fund Portfolio as an NRI

Investing isn’t about picking the “best” mutual fund. It’s about building a portfolio that suits your goals. A well-diversified mutual fund portfolio typically includes a mix of equity and debt funds. For instance, a moderate-risk investor might consider allocating 60% to equity (using a combination of large-cap, flexi-cap, and ELSS funds) and 40% to debt (through short-term or banking & PSU debt funds).

SIPs can be a powerful tool for NRIs to invest consistently without trying to time the market. Additionally, make it a habit to review your portfolio at least once a year. Rebalance if needed, especially if your goals or financial situation change.

The key is to start with clarity, diversify wisely, and stay invested with discipline.

Frequently Asked Questions (FAQs)

Can NRIs invest in mutual funds in India?

Yes, NRIs can invest in Indian mutual funds, provided they complete the necessary KYC formalities and invest through an NRE or NRO account. Many fund houses now allow NRIs to complete KYC via video verification. However, do note that some mutual fund companies restrict investments from NRIs living in the USA and Canada due to compliance constraints.

What is the best mutual fund for an NRI?

There is no single “best” mutual fund for all NRIs. The right fund for you depends on your risk tolerance, financial goals, investment horizon, and tax preferences. For instance, if you’re seeking equity exposure with tax benefits, the Mirae Asset Tax Saver Fund could be suitable. If safety is your priority, a debt fund like Kotak Banking & PSU might work better.

How can an NRI start a SIP in India?

Starting a SIP as an NRI is straightforward. First, complete your KYC process and link your NRE or NRO bank account to the AMC (Asset Management Company). You can then register for a SIP through online platforms or directly with the fund house. The SIP amount will be auto-debited each month, just like for resident investors.

Are mutual fund returns taxable for NRIs?

Yes, mutual fund gains are taxable for NRIs in India. Tax is deducted at source (TDS) on both equity and debt fund redemptions. You might also be taxed in your country of residence, although you may be able to claim credit under DTAA. The exact amount of tax you pay depends on the type of fund and the duration for which you hold it.

Can NRIs repatriate their mutual fund earnings?

Repatriation is allowed, but the rules depend on the type of bank account linked to your investment. Investments made through NRE accounts are fully repatriable, including both principal and capital gains. However, if you’ve invested through an NRO account, there are annual repatriation limits and documentation requirements.

Also Read: Facts About NRI Mutual Fund Taxation

Also Read: Can NRIs Invest in Mutual Funds in India?

0 Comments