You moved abroad for a new job, a better life, or to study. But your financial roots are still in India. Maybe you need to send money back home. Maybe you want to save your foreign income in India. Or perhaps you have rental income from a property you still own.

You know you need a special bank account for this. An NRI account.

The process seems confusing. The bank websites are full of jargon. You are not sure where to even begin. The thought of dealing with paperwork from thousands of miles away is overwhelming.

What if I told you it does not have to be hard?

I have helped many friends through this exact process. It is much simpler than you think. This guide will walk you through the entire process, one clear step at a time. Let’s get your NRI account opened.

What is an NRI Bank Account?

Think of it like this. A regular Indian savings account is for people who live in India. The moment you are officially considered a Non-Resident Indian (NRI), that same account becomes a problem. You cannot use it freely for international transactions.

An NRI bank account is a special account designed just for you. It follows rules set by the Reserve Bank of India (RBI) for Indians living abroad. There are three main types.

- The first is the NRE (Non-Resident External) Account. This is where you park your foreign earnings. You deposit money like US Dollars or British Pounds into this account. The bank converts it to Indian Rupees. The best part? The money in this account is 100% tax-free in India. Both the interest you earn and the initial amount you put in. You can also send this money back abroad anytime you want. This is called repatriation.

- The second type is the NRO (Non-Resident Ordinary) Account. This account is for managing the money you earn in India. Think of rental income from a property, dividends from stocks, or pension. You can put foreign money into it too, but its main job is to handle Indian income. The interest you earn on this account is taxable in India. Sending large amounts of money abroad from an NRO account has some restrictions.

- The third type, the FCNR (Foreign Currency Non-Resident) Account, is less common. It is a fixed deposit you open in a foreign currency itself. So, you deposit US Dollars and after the fixed term, you get back US Dollars. Your money is protected from the ups and downs of the rupee exchange rate.

For most NRIs, the conversation starts with choosing between an NRE and an NRO account. Often, people open both.

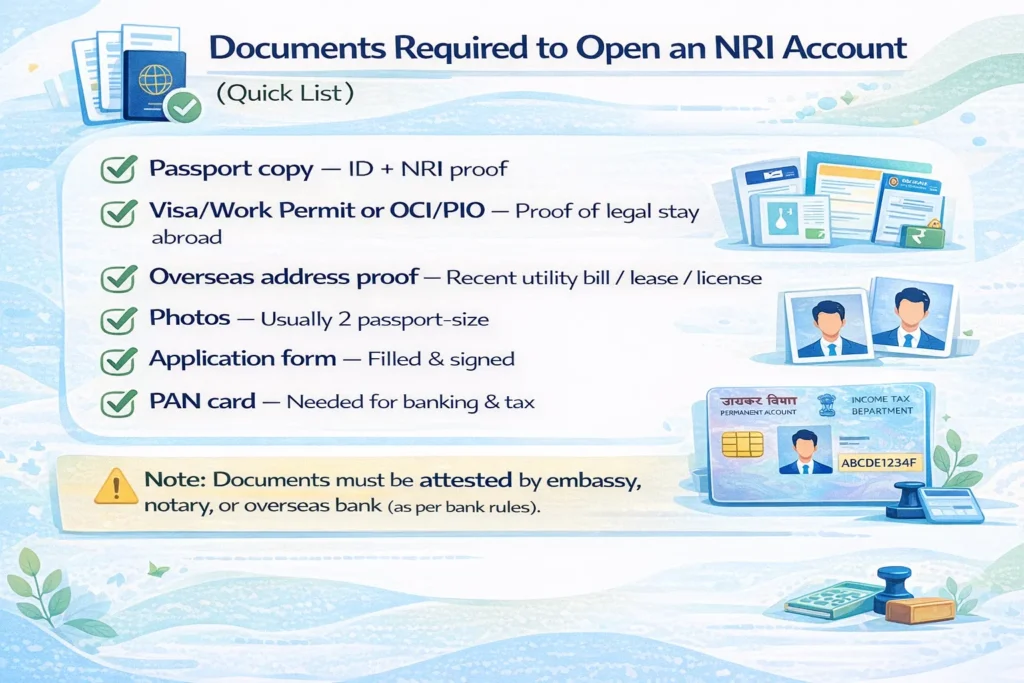

Documents Required to Open an NRI Account

This is the part that worries people the most. But the list is straightforward. You just need to get your copies attested. This means a recognized authority needs to stamp them to confirm they are real.

The standard checklist includes:

- Passport Copy: Every page, including the front and back cover. This is your primary proof of identity and NRI status.

- Valid Visa or Work Permit: This proves you are legally residing abroad. For OCIs/PIOs, you will need your card.

- Proof of Overseas Address: A utility bill (electricity, water, gas), your rental agreement, or a driving license from your country of residence. The bill should not be more than 3-6 months old.

- Passport-sized Photographs: Usually two are enough.

- A Fully Filled Application Form: You can get this from the bank’s website.

- PAN Card: While not always mandatory for opening the account, it is absolutely crucial for any financial transactions and tax purposes.

A crucial point about attestation. Most banks require your documents to be attested by an Indian Embassy official, a public notary, or your overseas bank. Some banks also accept attestation from certain community organizations. Always check your chosen bank’s specific list to see who they accept.

You might also need to provide a PIO/OCI card if you have one.

5 Easy Steps to Open an NRI Bank Account in India

This is the core of the guide. Follow these five steps in order, and you will have a clear path forward.

Step 1: Choose the Right Bank and Account Type

This is your most important decision. Do not just pick the bank your family uses. Do a little research.

You need to choose two things. First, the bank. Second, the type of account you need.

Picking the Bank: Look for banks with strong NRI services. The big names are always a safe bet. State Bank of India (SBI) has the largest network and is present in many countries. ICICI Bank and HDFC Bank are known for their excellent digital platforms and customer service for NRIs. Axis Bank and Kotak Mahindra Bank also have very competitive NRI offerings.

Look for a bank that has a dedicated NRI desk or a relationship manager. This makes solving problems from abroad much easier.

Picking the Account Type: Ask yourself a simple question. Where is the money coming from?

- Is the money you want to deposit earned outside India? (e.g., your salary in the USA). You want an NRE Savings Account.

- Is the money earned inside India? (e.g., rent from your Mumbai apartment). You want an NRO Savings Account.

Most NRIs end up with both. They use the NRE account for their foreign savings and investments. They use the NRO account to collect Indian income and pay for local expenses like maintenance fees for their property.

Step 2: Collect and Verify Required Documents

Now that you know your bank and account type, get your documents ready. Refer to the list we discussed above.

Download the application form from your bank’s website. Fill it out carefully. Double check all details like your name spelling and address. A small mistake here can cause a big delay.

Then, get your documents attested. This can be a hassle, but it is a one-time task. Find a local notary public or check your bank’s website for a list of authorized attestors in your city.

Step 3: Fill the Application Form (Online or Offline)

This step is merging with the next one thanks to technology. Many banks now let you start the process entirely online.

You can visit the NRI section of your chosen bank’s website. You will often find a button that says “Apply Now” or “Open Account Online.” You will be guided to fill a digital form and upload scanned copies of your attested documents.

Some people prefer to walk into a branch in India if they are visiting. You can submit the physical form and documents there. You can also visit an international branch of an Indian bank if there is one in your city.

Step 4: Complete the KYC Process

KYC means “Know Your Customer.” It is a mandatory process where the bank verifies your identity and address.

There are three common ways this happens:

- In-Person in India: If you submitted your form at a branch in India, your KYC is done right there.

- In-Person Overseas: Some Indian banks have branches or partner banks abroad. You might be asked to visit one to complete your verification.

- Video KYC: This is the biggest blessing for NRIs. Many banks now offer a completely paperless Video KYC process. A bank official will video call you at a scheduled time. They will ask you to show your original documents to the camera. They will take a screenshot for their records. The entire process takes about 10-15 minutes. It is incredibly convenient.

The bank will then verify all your details. This can take a few days to a couple of weeks.

Step 5: Fund Your Account and Start Using It

You will receive a welcome kit from the bank. It will have your account number, checkbook, and debit card. They will usually mail it to your overseas address.

Most banks require you to make an initial deposit to activate the account. This minimum amount varies. It can be as low as ₹5,000 for some banks or as high as ₹1,00,000 for others. Check your bank’s policy.

To fund your account, you can do a wire transfer from your overseas bank. You will need your Indian bank’s SWIFT code and your new account number. Your Indian bank will handle the currency conversion.

And that is it. Your account is now active. You can manage it through online banking, send money to family, or start investing in India.

Can NRIs Open an NRI Bank Account Online?

Yes, absolutely. This is now very common.

The process is not always 100% online from start to finish, but it is very close. As I mentioned, you can fill the form and upload documents online. Then, you can complete the verification via Video KYC from your living room abroad.

The entire process, from application to approval, can happen without you ever setting foot in a branch. However, this can depend on the bank you choose and the country you are in. Some countries have stricter rules. Always check the bank’s website for the most current information.

Best Banks for NRI Accounts in India (2025)

It is hard to say one bank is the “best” for everyone. It depends on what you value most.

- State Bank of India (SBI): The largest bank. Best if you want a huge network and presence. Their processes can be a bit slower, but they are reliable.

- ICICI Bank: Very popular among NRIs. They have a great online platform and strong customer support. Their NRI services are a core focus.

- HDFC Bank: Another excellent choice. They offer a wide range of investment products alongside banking. Their digital app is very user-friendly.

- Axis Bank: Known for competitive exchange rates and good service. They have a streamlined process for NRIs.

- Kotak Mahindra Bank: They often offer higher interest rates on NRE deposits and have good service reviews.

My advice? Shortlist two banks. Visit their websites. Compare their minimum balance requirements, fees for wire transfers, and online banking features. Then make your choice.

Tips to Make the NRI Account Opening Process Easy

I learned this from helping my friend Rohan open his account from Singapore. A little preparation saves a lot of time.

- Call the Bank’s NRI Desk: Before you start, just call them. Ask them every small question you have. They are there to help and will guide you on the exact documents they need.

- Use Video KYC: If your bank offers it, always choose this option. It is the fastest way to get things done.

- Check Exchange Rates: Before you transfer a large amount of money, keep an eye on currency exchange rates. Sometimes waiting a few days can get you more rupees for your dollar.

- Start Small: Do not feel pressured to transfer your life’s savings on day one. Open the account. Transfer a small amount to test the process. Make sure everything works. Then proceed with larger transfers.

FAQs

Can I open an NRI account from the USA/UK/UAE?

Yes, you can. The process is the same for NRIs in any country. You can apply online and use Video KYC from anywhere in the world.

What’s the minimum balance for NRE/NRO accounts?

It varies by bank. It can range from ₹5,000 to ₹1,00,000 or more. Many banks offer zero-balance accounts if you maintain a fixed deposit. Always check with your specific bank.

Can I convert my resident account to an NRI account?

Yes, and you must. The moment you become an NRI, you are required to convert your existing resident savings account to an NRO account. You inform your bank, fill a form, and they will convert it. You can then open a new NRE account for your foreign income.

Are there tax benefits for NRI accounts?

Yes, for the NRE account. The interest you earn on an NRE account is completely tax-free in India. The interest on an NRO account is taxable.

Which is better: NRE or NRO account?

One is not better than the other. They serve different purposes. Use an NRE account for your foreign income you want to save or invest in India. Use an NRO account to manage your income that is generated within India.

Also Read: 8 Ways NRIs Can Repatriate Funds from India Without Hassle

Also Read: 6 Things NRIs Should Know Before Investing in Indian Real Estate

Also Read: Tips to Avoid Income Tax Notices: Compliance Strategies for NRIs

0 Comments