You land that promotion or a new job. The salary hits six figures. $150,000 a year. It feels great. Finally, you have room to breathe, save, and enjoy life.

Then tax season arrives.

You see the number withheld from your paychecks. You calculate what you might owe. It stings. A huge chunk of your hard work is gone.

But here’s the truth most people miss: Paying too much tax is a choice. Not a legal one, but a choice based on poor planning. The government isn’t going to hand you a manual on how to keep your money. That’s on you.

This guide is that manual. We are talking about legal tax optimization. No loopholes. No evasion. Just smart, logical strategies to ensure you keep more of what you earn. Let’s dive into exactly how to pay less taxes on your $150K income.

How Much Tax Do You Actually Pay on $150K?

Before we fix the problem, let’s look at the numbers. The tax rate on 150k isn’t as scary as it seems at first glance. Many people confuse their marginal tax bracket with their overall tax bill.

Your income tax on 150k depends on a few things:

- Filing Status: Are you single or married filing jointly?

- Deductions: Are you taking the standard deduction or listing out your expenses?

- Location: Does your state have an income tax?

Here is a simplified breakdown. For a single filer in 2024, the federal income tax brackets are progressive. This means you don’t pay 24% on your entire income. You pay 10% on the first chunk, 12% on the next, and so on.

After the standard deduction (which is over $14,000 for individuals), your taxable income drops. So, what is 150k after taxes? A rough estimate for a single filer in a state with no income tax might look like this:

- Federal Income Tax: ~$24,000 – $28,000

- Social Security / Medicare (FICA): ~$11,000

- Net Take-Home Pay: ~$111,000 – $115,000

Your effective tax rate (the actual percentage of your total income paid in taxes) lands around 18% to 24% . But here’s the kicker. With smart planning, you can shrink that number significantly and push your take-home pay even higher.

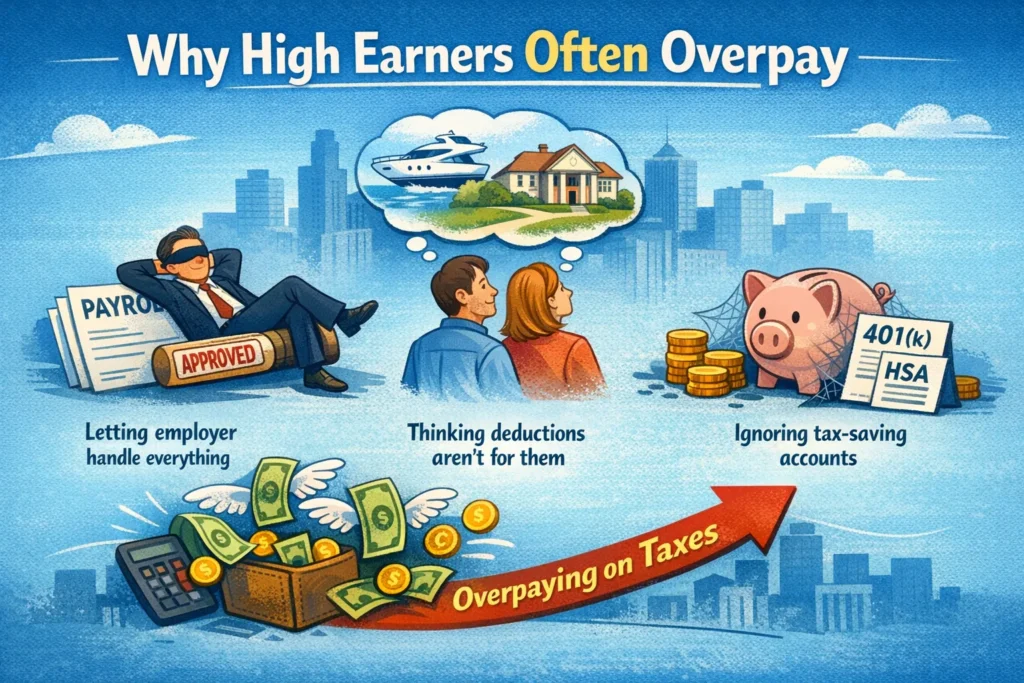

Why High Earners Often Overpay

Making more money should mean keeping more money, right? Not always. High earners often fall into predictable traps. They overpay because they assume their tax situation is too complex to handle or, conversely, too simple to worry about.

Common reasons people overpay:

- They let their employer handle everything and never check the details.

- They think deductions are only for the ultra-wealthy or business owners.

- They ignore accounts designed specifically to save them money (like a 401(k) or HSA).

- They don’t think about the tax impact of their investments.

The goal of how to pay less in taxes isn’t about finding a secret trick. It’s about avoiding these common pitfalls and being intentional with your money.

Top Ways to Pay Less Taxes on $150K Income

Ready to build a plan? Here are the most effective strategies for someone in your income bracket.

1. Max Out Your Retirement Contributions (The #1 Strategy)

This is the simplest and most powerful tool for any salaried employee. A traditional 401(k) lets you put money in before the government takes its cut.

Think of it this way. Every dollar you contribute to a traditional 401(k) disappears from your W-2. You don’t pay income tax on it today. The tax man waits until you withdraw it in retirement.

In 2024, you can contribute up to $23,000. If you are 50 or older, you can add another $7,500 as a “catch-up” contribution.

Let’s do the math. If you earn $150,000 and contribute $20,000 to your 401(k), your taxable income instantly drops to $130,000. That could save you thousands in federal income tax for the year. This is a primary way how to reduce the tax on salary effectively.

2. Use a Health Savings Account (HSA)

If you have a high-deductible health plan (HDHP), you likely have access to an HSA. This account is the best retirement and tax-saving vehicle you aren’t using.

Why? It offers a “triple tax benefit.”

- Tax-Free In: The money you put in is tax-deductible, just like a 401(k).

- Tax-Free Growth: Any interest or investment gains in the account are not taxed.

- Tax-Free Out: Withdrawals are tax-free as long as you use them for qualified medical expenses. In retirement, you can even use it for non-medical expenses (it just acts like a traditional IRA then).

For 2024, you can contribute up to $4,150 for an individual or $8,300 for a family. For a high earner, this is a no-brainer. It reduces your taxable income now and builds a medical nest egg for the future.

3. Claim All Available Deductions

The tax code rewards certain behaviors. If you do these things, make sure you are claiming them. You must itemize to get these benefits, meaning you skip the standard deduction and list your expenses instead.

Common deductions for someone earning $150K:

- Mortgage Interest: Interest paid on the first $750,000 of your mortgage debt.

- State and Local Taxes (SALT): You can deduct up to $10,000 of combined state income and property taxes.

- Charitable Donations: If you give money or goods to qualified charities, keep the receipts.

- Student Loan Interest: You can deduct up to $2,500 in interest paid, even if you don’t itemize.

4. Pick the Right Deduction Strategy

This is a simple but crucial choice. You have two options:

- Standard Deduction: A flat amount you can subtract from your income. For 2024, it’s $14,600 for singles and $29,200 for married couples filing jointly.

- Itemized Deduction: The total of all your eligible expenses (mortgage interest, charity, etc.).

The rule is simple: choose the higher number. Many people assume the standard deduction is best because it’s easy. But if you own a home or give a lot to charity, itemizing might save you more. Always run the numbers both ways.

5. Focus on Tax Credits (They Are More Powerful)

A deduction lowers the amount of income that gets taxed. A credit lowers your actual tax bill, dollar for dollar.

Think of it this way. A $1,000 deduction might save you $240 if you are in the 24% tax bracket. A $1,000 credit saves you the full $1,000.

Important credits for your income level:

- Child Tax Credit: Worth up to $2,000 per qualifying child. It begins to phase out at higher income levels, but at $150K, you may still qualify for a partial credit.

- Child and Dependent Care Credit: If you pay for childcare so you can work, you may be eligible for a credit.

- Lifetime Learning Credit / American Opportunity Tax Credit: If you or a dependent are in college or taking courses to improve job skills, look into these.

6. Optimize Your Investment Taxes

If you have a brokerage account (investing outside of a retirement plan), how you buy and sell matters.

- Hold for the Long Term: Assets held for over a year are taxed at the long-term capital gains rate (0%, 15%, or 20%). This is almost always lower than your ordinary income tax rate.

- Tax-Loss Harvesting: This is a fancy term for a simple idea. Sell an investment that has lost value. Use that loss to offset any gains you made from selling other investments. If your losses exceed your gains, you can even use up to $3,000 of loss to lower your regular taxable income.

7. Use Flexible Spending Accounts (FSA)

Your employer might offer an FSA. This is another “use it or lose it” account, so be careful. But if you have predictable expenses, it’s a great tool.

You contribute pre-tax money to the account. You then use that money for eligible expenses.

- Healthcare FSA: For co-pays, prescriptions, glasses, and other medical costs not covered by insurance.

- Dependent Care FSA: For daycare or after-school care costs for children under 13.

The money you put in lowers your taxable income, saving you on federal, state, and even Social Security and Medicare taxes.

8. Time Your Income and Expenses

You have some control over when you get paid and when you pay certain bills. This is called tax timing.

- Defer Bonuses: If you expect a big year-end bonus, see if your employer can pay it in January instead of December. This pushes the tax liability into the next year.

- Accelerate Deductions: If you plan to itemize, you can “bunch” expenses. For example, make your January mortgage payment in December to get an extra year of interest. Or make your charitable donations for next year in December of this year.

9. Structure Business or Side Income

If you have a side hustle, freelance work, or a small business, how you structure it matters.

When you are a sole proprietor, your business income is simply added to your W-2 income. You pay self-employment tax on top of income tax.

But registering as an LLC or S-Corp opens up options. You can deduct legitimate business expenses directly from your business income. This includes a home office, a portion of your internet bill, software subscriptions, and even some travel. This directly lowers your taxable income. This is a powerful way for how can i pay less in taxes when you have multiple income streams.

Sample Tax Savings Breakdown on $150K

Let’s see how this adds up. Imagine a single filer earning $150,000.

| Strategy | Action | Tax Savings (Estimate) |

|---|---|---|

| 401(k) | Contribute $20,000 | ~$4,800 |

| HSA | Contribute $4,000 (Family) | ~$960 |

| Itemized Deductions | Mortgage interest + charity > Standard Deduction | ~$2,000 |

| Tax Credits | Child Tax Credit (if applicable) | ~$2,000 |

| TOTAL POTENTIAL SAVINGS | ~$9,760+ |

These are rough estimates. Your actual savings depend on your tax bracket and specific situation. But the point is clear. By using these strategies, you can potentially save $8,000 to $15,000 or more each year.

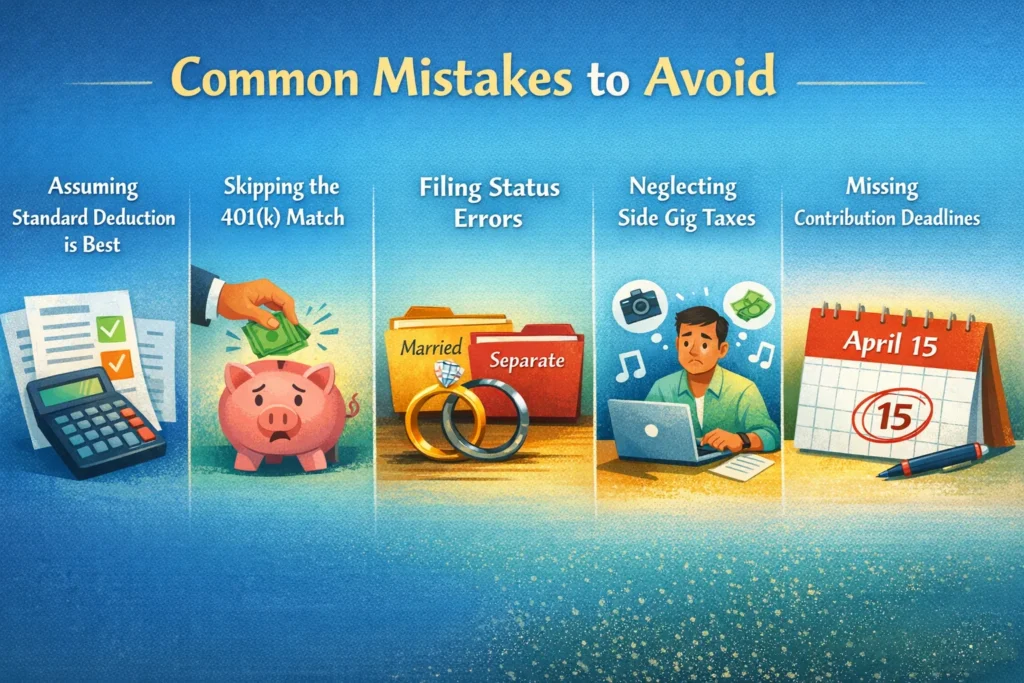

Common Mistakes to Avoid

Saving money is also about not losing it to common errors. Avoid these tax traps.

- Assuming the standard deduction is always best. Do the math or ask a pro.

- Leaving “free money” on the table. Not contributing enough to your 401(k) to get the full employer match is a huge mistake. It’s literally turning down a raise.

- Filing status errors. Married couples often file separately when filing jointly would save them thousands.

- Forgetting about side hustle taxes. If you make money from a side gig, you likely need to pay estimated taxes quarterly. Ignoring this can lead to penalties.

- Missing the deadline for contributions. You have until the tax filing deadline (usually April 15th) to make prior-year IRA and HSA contributions. Mark your calendar.

Advanced Tax Strategies for High Earners

If you’ve mastered the basics, here are some advanced moves for those earning $150K or more.

Backdoor Roth IRA

High earners often can’t contribute directly to a Roth IRA because of income limits. But there’s a legal workaround.

You contribute to a traditional IRA (which has no income limits). Then, you immediately convert that traditional IRA into a Roth IRA. You pay taxes on any growth in between (which should be minimal if you do it right away). After that, the money grows tax-free forever. It’s a bit of paperwork, but it opens the door to tax-free wealth for high-income earners.

Real Estate Depreciation

If you own rental property, the IRS lets you deduct a portion of the building’s cost every year as “depreciation.” This is a non-cash deduction. It lowers your taxable rental income on paper, even if the property is actually generating cash flow. It can dramatically reduce or even eliminate the tax you owe on your rental income.

Income Splitting

If you own a business, you might be able to split income with family members in lower tax brackets. For example, you could legitimately employ your child in the business. Their earned income is taxed at their rate, which is likely much lower than yours. This must be done carefully and legally, with real work performed.

How Filing Status Impacts Taxes on $150K

Your marital status on December 31st determines your filing status for the entire year. This choice has a massive impact.

For example, the taxes on $150k married filing jointly are much friendlier than filing as a single person. The tax brackets for married couples are almost double the size of the single brackets.

- A single person hits the 24% bracket at $100,525 of taxable income.

- A married couple filing jointly doesn’t hit the 24% bracket until they earn $201,050.

So, if you are married and one spouse earns $150,000 while the other stays home, your joint income is still $150,000. You get to use the wider, lower tax brackets designed for two people. This can result in a significantly lower tax bill compared to two single people each earning $75,000.

Tools and Resources for Tax Planning

You don’t have to figure this all out alone. Use these resources:

- Tax Calculators: Use online calculators (like those from SmartAsset or NerdWallet) to estimate your tax liability and see the impact of changes.

- Tax Preparation Software: Tools like TurboTax or H&R Block walk you through deductions and credits step-by-step.

- Certified Public Accountant (CPA) or Enrolled Agent (EA): If your situation is complex (side business, rental properties, RSUs), paying a few hundred dollars for professional advice can save you thousands.

Conclusion

Earning $150,000 puts you in a strong financial position. But how much of it you actually get to keep comes down to one thing: planning.

Paying less tax isn’t about finding shady loopholes. It’s about understanding the rules of the game and playing by them. It’s about choosing to put money in a 401(k) instead of a regular bank account. It’s about using an HSA for medical expenses. It’s about timing your donations.

These small, smart choices are not complicated. They just require intention. Start with the retirement account. Look into an HSA. Track your potential deductions. Even implementing just two of these strategies can put thousands of dollars back in your pocket every single year.

Don’t let taxes take a bigger bite than they have to. Take control, make a plan, and keep more of what you earn.

FAQs

How much federal tax do I pay on $150K as a single filer?

You will likely pay between $24,000 and $28,000 in federal income tax. Your exact bill depends on your deductions and credits, but the effective rate usually falls between 18% and 24%.

What is the best way to lower my taxable income quickly?

Max out your traditional 401(k). For 2024, you can contribute up to $23,000. This money comes out of your paycheck before taxes, instantly lowering your reported income and your current tax bill.

Can I contribute to a Roth IRA if I make $150K?

Single filers phase out of Roth eligibility starting at $146,000. However, you can use the “backdoor Roth IRA” strategy. This involves contributing to a traditional IRA and then converting it to a Roth.

Is an HSA better than a 401(k) for tax savings?

For medical expenses, yes. An HSA offers a triple tax benefit: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical costs. It is an incredibly powerful savings tool.

Should I itemize deductions on $150K?

Maybe. Compare your total eligible expenses (mortgage interest, charity, state taxes) to the standard deduction ($14,600 for singles in 2024). If your itemized total is higher, you should itemize to save more.

How does marriage affect my taxes on $150K?

Marriage can lower your taxes significantly. The married filing jointly tax brackets are almost double the size of single brackets, meaning more of your income is taxed at lower rates compared to being single.

What tax credits can I get with a $150K income?

You may qualify for the Child Tax Credit (up to $2,000 per child) and the Child and Dependent Care Credit. These are more valuable than deductions because they reduce your tax bill dollar-for-dollar.

How can my side hustle reduce my taxes?

A side hustle lets you deduct legitimate business expenses like a home office, software, and equipment. These deductions lower your total taxable income, saving you money on both your side income and your main salary.

What is tax-loss harvesting?

It means selling an investment at a loss to offset the taxes on an investment you sold at a gain. You can also use up to $3,000 in net losses to lower your regular taxable income each year.

Can I pay zero taxes on $150K?

For a salaried employee, it is not realistic to pay zero federal income tax. However, by strategically using pre-tax retirement accounts, an HSA, and all available credits, you can reduce your bill by thousands of dollars.

0 Comments