Taxes in India are changing faster than ever. You’re watching your salary slip more carefully. You’re checking your stock portfolio. And you’re wondering: What’s different this year?

The truth is, FY 2024-25 brings major shifts in how India collects taxes, who pays them, and what gets reported. More young professionals are filing returns. Digital transactions are being tracked closely. And the government is collecting more money than before.

In this guide, we break down the numbers that matter. No jargon. Just the facts you need to understand where Indian taxation is headed and what it means for your wallet.

Shift in Taxpayer Demographics in India (FY 2024-25)

India’s taxpayer base is getting younger. And it’s growing fast.

Walk into any co-working space in Pune or Bangalore. You’ll see 25-year-olds filing their first tax returns. They’re freelancers, software engineers, content creators. Many of them earn more than their parents ever did at that age.

Personal income tax collections jumped 21% year-on-year, crossing ₹9.48 lakh crore. That’s not just inflation. That’s millions of new taxpayers entering the system.

The demographic shift is real. Urban millennials between 20 and 35 are now the fastest-growing segment. Think about it. Your younger colleagues? They’re probably filing ITRs for the first time this year. Women taxpayers are also increasing. Tier-2 and Tier-3 cities are contributing more because of digital banking and UPI adoption. Remote work made it possible for someone in Indore to earn a Mumbai salary. And the tax department knows it.

Here’s what’s driving this change: Better jobs. Higher salaries. More awareness about tax compliance. And one more thing. The new tax regime is now the default. Most first-time filers don’t even know there’s an old regime. They just go with what’s simpler.

Major Tax Collection Volume Trends FY 2024-25

Let’s talk numbers. Big numbers.

Gross direct tax collections during FY 2024-25 reached ₹25,86,947 crore, including ₹12,40,308 crore from corporate taxes and ₹12,90,144 crore from personal income tax.

That’s massive growth. And here’s why it matters to you.

- Direct tax collections: Growing steadily across all categories.

- Advance tax payments: Companies and individuals are paying more upfront. Securities transaction tax jumped 65%, reaching ₹49,201 crore. That’s because more people are trading stocks than ever before.

- TDS and TCS: These are still the largest contributors. Your employer deducts tax every month. Your bank deducts it when you make certain transactions. It adds up.

- Digital compliance: Everything’s automated now. The Income Tax Department can see your transactions in real-time. They match your AIS with your ITR. Mismatches? You get a notice.

Refunds increased by 42.63%, totaling over ₹4.10 lakh crore. The department is processing refunds faster. That’s good news if you’re waiting for money back.

What’s the takeaway here? The government is meeting its targets. Tax collections hit 100.78% of the budget target, which was ₹22.07 lakh crore. The economy is growing. People are earning more. And tax compliance is improving.

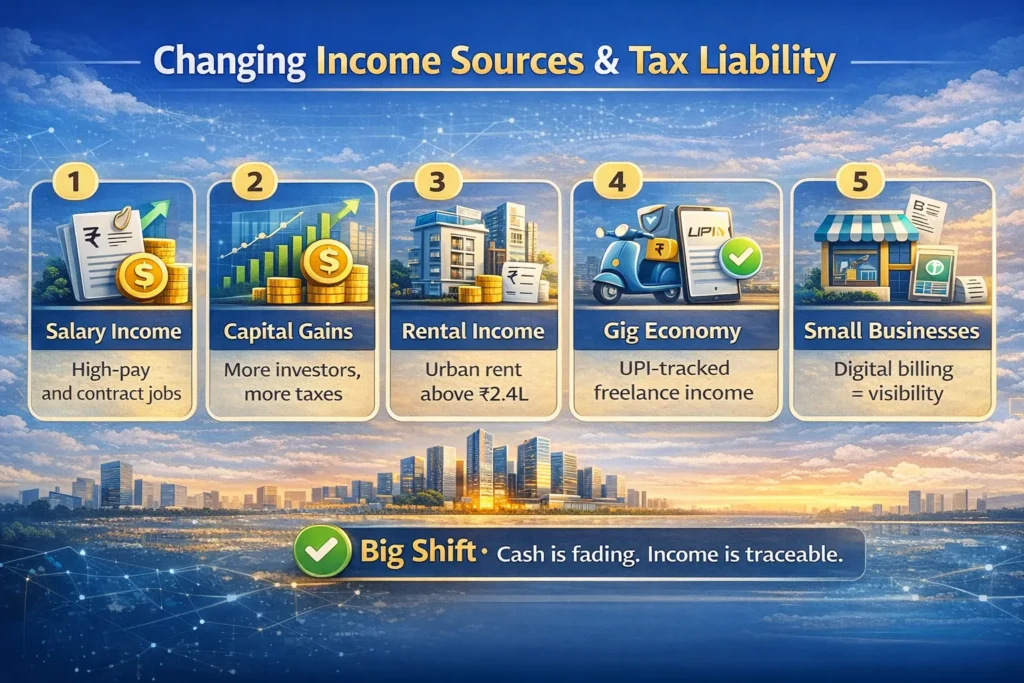

Changing Income Sources & Tax Liability Patterns

Where is all this tax money coming from? Different places than before.

- Salary income: Still the biggest source. But it’s not just traditional 9-to-5 jobs anymore. Contract roles and high-paying tech jobs are adding to the pile.

- Stock market and capital gains: This is the big story of FY 2024-25. Remember that 65% jump in securities transaction tax? Young investors are making money in the markets. And they’re paying taxes on it.

- Rental income: Urban real estate is booming. People who own property in cities like Bangalore and Hyderabad are earning rental income. And they need to report it if it crosses ₹2.4 lakh annually.

- Gig economy: Zomato delivery partners. Uber drivers. Freelance designers. They’re all part of the formal economy now. UPI payments leave a digital trail. The tax department sees it.

- wSmall businesses: Digital billing is everywhere. That small grocery store accepting payments through Paytm? They’re on the radar too.

Here’s what changed. Higher disclosures mean less under-reporting. The days of hiding cash income are over. Everything’s tracked. Everything’s visible.

I recently met a small business owner in Delhi. He told me, “I used to accept cash for half my sales. Now everyone pays through UPI. I have to report everything.”

That’s the new reality.

Updated Income Tax Reporting Thresholds FY 2024-25

Let’s get specific about what you need to report.

These thresholds aren’t just guidelines. Cross them, and the tax department will know.

| Transaction Type | Threshold Amount | How It’s Reported |

|---|---|---|

| Cash deposits in savings account | ₹10 lakh | SFT reporting by banks |

| Cash payment for credit card bills | ₹2 lakh | PAN required |

| Mutual fund purchases | ₹50,000+ | KYC + PAN mandatory |

| Real estate transactions | Full value | TDS compliance needed |

| Rental income | ₹2.4 lakh+ annually | Must be shown in ITR |

SFT reporting is the big thing now. Statement of Financial Transactions. Banks, mutual funds, credit card companies. They all report high-value transactions to the tax department.

Think about it. You deposit ₹15 lakh in cash across the year. Your bank reports it. The tax department sees it. If your ITR doesn’t match? You’ll get a notice.

Same with real estate. Bought a flat? The builder reports it. Paid stamp duty? The government knows. Took a home loan? Your bank reports the interest.

Everything is connected. Everything is visible.

One more example. You buy ₹1 lakh worth of mutual funds. Your fund house reports it. They have your PAN. They know your income. If you haven’t filed returns? They’ll find out.

The system is getting tighter. Not necessarily stricter. Just more transparent.

New Compliance Rules & Audit Enhancements

Compliance is no longer optional. It’s automated.

High-value digital transactions trigger scrutiny. Not human scrutiny. Algorithm scrutiny. The system flags mismatches. Then a real person looks at your case.

PAN-linked reporting is everywhere now. Your PAN is connected to your bank accounts. Your Demat account. Your mutual funds. Your property records.

The tax department runs checks on:

- Unexplained credits in your bank account

- Foreign income that wasn’t reported

- Capital market transactions that don’t match your returns

Audit probability increases if:

- Your lifestyle doesn’t match your reported income

- You have significant stock trading turnover

- There’s a large gap between what you spend and what you earn

Businesses with turnover exceeding ₹1 crore must undergo mandatory tax audit, though this limit rises to ₹10 crore if cash transactions are less than 5% of total transactions.

Let me give you a real-world scenario. You earn ₹8 lakh annually according to your ITR. But you bought a car worth ₹15 lakh. You took a foreign vacation. You purchased gold.

The system will flag this. It’s called AI-based risk assessment. And it’s getting smarter every year.

What should you do? Keep proper records. Save your bank statements. Document everything. If you can explain your income sources, you’re fine.

The government isn’t trying to harass honest taxpayers. They’re trying to catch people who hide income. Big difference.

Capital Gains Tax Update FY 2024-25

Capital gains tax changed significantly this year. If you invest in stocks, mutual funds, or property, pay attention.

The big changes from July 23, 2024

Long-term capital gains tax increased to 12.5% from 10%, while the exemption limit rose to ₹1.25 lakh from ₹1 lakh.

Short-term capital gains tax on equity shares and equity-oriented mutual funds jumped from 15% to 20%.

Let’s break this down with examples.

For stocks and equity mutual funds

You bought shares worth ₹2 lakh. Sold them after 13 months for ₹3.5 lakh. That’s ₹1.5 lakh in long-term capital gains.

First ₹1.25 lakh? Tax-free.

Remaining ₹25,000? Taxed at 12.5%.

Your tax: ₹3,125.

For property

The long-term capital gains tax on property dropped from 20% to 12.5%, but indexation benefits were removed for properties bought after July 23, 2024.

If you bought property before July 23, 2024, you have a choice. Calculate tax at 20% with indexation. Or at 12.5% without indexation. Pick whichever is lower.

TDS and reporting obligations

Selling property? TDS will be deducted. Selling shares? Your broker reports it. Everything goes into your Annual Information Statement.

You must reconcile:

- Your AIS

- Your broker statements

- Your bank statements

- Your capital gains in ITR

Mismatches lead to notices. I’ve seen people get notices for differences as small as ₹5,000. The system is that precise.

One more thing. From October 1, 2024, share buybacks are taxed as dividend income. Not capital gains. Different rules. Different tax rates.

Stay sharp. This stuff matters.

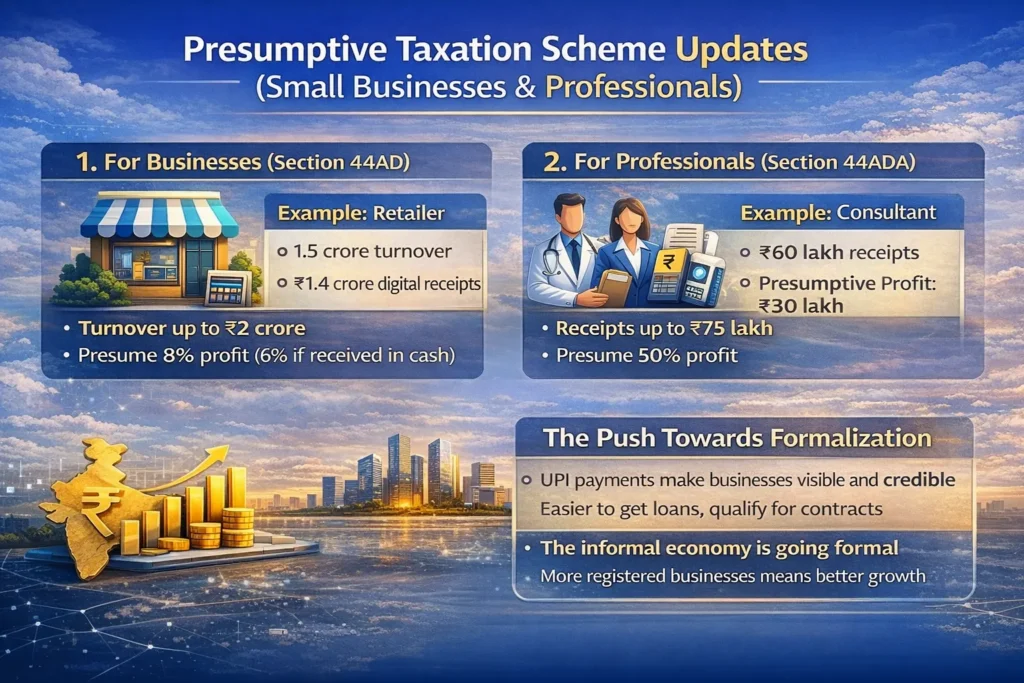

Presumptive Taxation Scheme Updates (Small Businesses & Professionals)

Small business owners and professionals have it easier. But only if they understand the rules.

Sections 44AD and 44ADA let you estimate your income without maintaining detailed books. It’s called presumptive taxation.

For businesses (Section 44AD)

If your turnover is below ₹2 crore and at least 95% of receipts are through digital modes, you can use the presumptive scheme.

You assume 8% of your turnover is profit if received digitally. 6% if received in cash.

Example: You run a small retail store. Annual turnover: ₹1.5 crore. You receive ₹1.4 crore through UPI and cards.

Your presumptive profit: ₹11.2 lakh (8% of ₹1.4 crore).

You pay tax on this. No need to maintain complex accounts.

For professionals (Section 44ADA)

If you’re a doctor, lawyer, architect, or consultant, and your receipts are below ₹75 lakh, you can assume 50% of your receipts as profit.

Example: You’re a freelance graphic designer. You earned ₹60 lakh this year. All through bank transfers.

Your presumptive profit: ₹30 lakh.

Pay tax on this. Simple.

The push towards formalization:

UPI payments are everywhere. Even small kirana stores accept them. This means more businesses are coming under the tax net.

Is this bad? Not really. It brings credibility. Banks give loans more easily if you file returns. Government contracts require GST registration.

The informal economy is becoming formal. Slowly but surely.

Standard Deduction & Tax Regime Choice 2025

This is where most people get confused. Old regime or new regime?

The new tax regime is now the default. Unless you file Form 10-IEA before the due date, you’ll automatically be taxed under the new regime.

Standard deduction for salaried individuals

The standard deduction remains at ₹50,000 for FY 2024-25. This reduces your taxable income automatically.

But here’s the catch. The new regime doesn’t allow most of the old deductions. No Section 80C. No HRA. No home loan interest deduction.

Which regime suits you?

If your total deductions are ₹1.5 lakh or less: Choose the new regime.

If your deductions exceed ₹3.75 lakh: The old regime might save you more.

Let me show you with an example.

Scenario: ₹10 lakh salary

New regime:

- Gross income: ₹10 lakh

- Standard deduction: ₹50,000

- Taxable income: ₹9.5 lakh

Tax calculation:

- Up to ₹3 lakh: Nil

- ₹3-7 lakh: 5% of ₹4 lakh = ₹20,000

- ₹7-10 lakh: 10% of ₹2.5 lakh = ₹25,000

Total tax: ₹45,000 (before cess)

Old regime:

- Gross income: ₹10 lakh

- Standard deduction: ₹50,000

- Section 80C: ₹1.5 lakh

- HRA: ₹1.5 lakh (assuming you pay rent)

- Taxable income: ₹6.5 lakh

Tax calculation:

- Up to ₹2.5 lakh: Nil

- ₹2.5-5 lakh: 5% of ₹2.5 lakh = ₹12,500

- ₹5-6.5 lakh: 20% of ₹1.5 lakh = ₹30,000

Total tax: ₹42,500 (before cess)

The old regime saves you ₹2,500. Not much. But if your deductions are higher, the savings increase.

Who’s migrating to the new regime?

Young professionals without home loans. People who don’t invest much. Those who value simplicity over savings.

Around 60-65% of taxpayers are now using the new regime. That’s a rough estimate based on filing patterns.

Choose wisely. You can switch every year if you don’t have business income.

Urbanization & Digital Economy Driving Tax Revenue Growth

India is going digital. And taxes are following.

Tier-2 and Tier-3 cities are contributing more to tax collections. Why? Because people in Jaipur, Surat, and Coimbatore now have access to the same financial tools as people in Mumbai.

Digital infrastructure is the game-changer:

- FASTag tracks highway toll payments

- UPI records every small transaction

- GST e-invoicing makes business transactions visible

- Direct Benefit Transfer reduces cash leakages

The steady growth in direct tax collections indicates rising corporate profits and increasing incomes from high-value jobs in manufacturing and services sectors.

The gig economy is officially taxed

Food delivery partners. Ride-sharing drivers. Freelance writers. They’re all in the system now.

Think about it. A Zomato delivery partner makes ₹40,000 a month. All payments through the app. The company reports his income. He gets a Form 16 equivalent.

He files his ITR. He’s part of the formal economy.

Is this fair? Absolutely. Everyone should pay their share. And honestly, being part of the formal system has benefits. Access to credit. Government schemes. Pension plans.

Financial literacy is improving

YouTube videos explain tax filing. Mobile apps make it easy. CA services are more affordable. People understand taxes better than they did five years ago.

The result? More compliance. Less evasion. Higher collections.

And here’s the thing. This trend will accelerate. As more Indians move to cities, use smartphones, and earn through formal channels, tax collections will keep growing.

It’s not about the government becoming stricter. It’s about the economy becoming more transparent.

Summary: What These Changes Mean for You

Let’s wrap this up with what actually matters.

Higher transparency = fewer tax leakages

The system is tighter. Transactions are tracked. Under-reporting is harder.

Tax base expanding due to digitization and young earners

Millions of first-time taxpayers entered the system this year. That trend will continue.

Investors and digital businesses face more reporting rules

If you trade stocks, own property, or run an online business, you’ll report more than before. Keep records. Stay organized.

Choosing the right tax regime + compliance saves money

Don’t just go with the default. Calculate both regimes. See which saves you more. File on time. Avoid penalties.

The Indian tax system is evolving. It’s becoming smarter. More data-driven. More efficient.

For honest taxpayers, this is good news. For those trying to hide income, the walls are closing in.

My advice? Embrace the change. File your returns accurately. Claim what you’re entitled to. And sleep peacefully knowing you’re compliant.

Because in FY 2024-25, the tax department knows more than you think. And that’s not a bad thing.

Frequently Asked Questions

What are the major tax reporting changes in FY 2024-25?

The biggest changes include lower reporting thresholds for financial transactions, mandatory SFT reporting by banks for deposits above ₹10 lakh, and stricter capital gains reconciliation requirements. The new tax regime is now the default, and ITR forms have been updated to capture more detailed information.

Which income sources require more disclosure now?

Capital gains from stocks and property, rental income above ₹2.4 lakh annually, large cash deposits, high-value mutual fund purchases, and cryptocurrency transactions all require detailed disclosure. The Annual Information Statement now pre-fills most of this data.

Will the new tax regime become mandatory?

No, it’s the default but not mandatory. You can still opt for the old regime by filing Form 10-IEA before the ITR due date. For non-business cases, you can switch between regimes every year based on what’s more beneficial for you.

Why is the number of taxpayers increasing in India?

Several factors are driving this growth: more young professionals entering high-paying jobs, widespread adoption of digital payments making income visible, better tax literacy through online resources, and stricter compliance requirements. The gig economy and remote work opportunities have also brought millions into the formal sector.

Also Read: 10 Common NRI Investment Myths Debunked

Also Read: 10 Tips for NRIs to Protect Their Indian Investments from Scams and Fraud

Also Read: Understand the Difference Between W-2 and 1099 Income

0 Comments