Imagine this. You are sipping your morning coffee, scrolling through your emails. One subject line makes you pause. It is from the Income Tax Department of India. Your heart skips a beat. A wave of confusion hits you. You live abroad. You pay taxes there. Why is India sending you a notice?

The reason often lies in a simple form you might have missed. A schedule called FA. Or a rule you did not know about. The world of taxes has changed. Borders are no longer barriers for tax authorities. If you are an NRI with assets or income abroad, the Indian government likely knows about them. And they expect you to tell them too.

This guide breaks down everything you need to know. We will talk about foreign asset disclosure rules. We will explain the scary Black Money Act in simple terms. And we will show you how to stay safe from those unsettling tax notices.

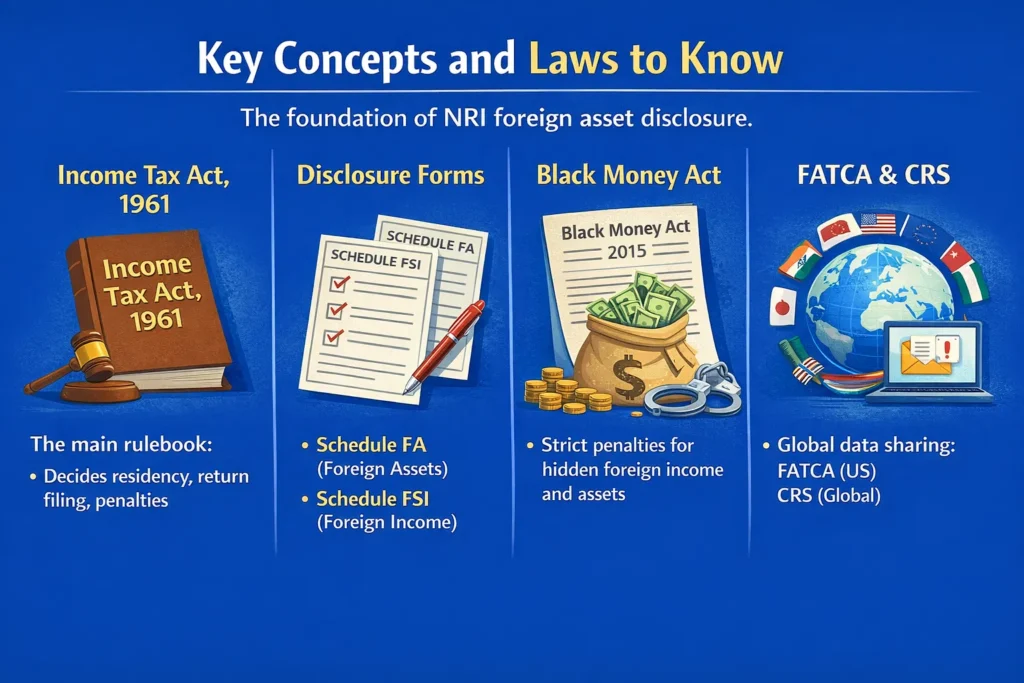

Key Concepts and Laws to Know

Before we dive into the details, let us get familiar with the key players. Think of this as learning the rules of the road before you start driving. These laws and forms are the foundation of NRI foreign asset disclosure.

The Income Tax Act, 1961 is the main rulebook. It decides your residential status. It dictates if you need to file a return. And it outlines the penalties for getting it wrong.

Then come the specific disclosure forms. Schedule FA is your calendar year report card for foreign assets. It asks what you own outside India. Schedule FSI is about the income those assets generate. You must include these with your income tax return if you are required to.

The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 is the strict enforcer. It was created to tackle money hidden overseas. The penalties under this act are severe. They include high taxes, huge fines, and even jail time. Recently, some relief was offered for small assets. But for larger amounts, it is a law you do not want to trigger.

Finally, there are the global systems. FATCA (US) and CRS (Global) are automatic data exchange agreements. Banks in over 100 countries now share financial data with each other. Your bank in Dubai or Singapore sends details to India. The Indian tax department then checks if this matches what you declared. If it does not, that is when the notice arrives.

Who Needs to Disclose Foreign Assets and File Returns

This is the most common point of confusion. Not every NRI needs to declare every global asset. It all hinges on one thing. Your residential status for the financial year.

The rules are different for each category.

| Category | Obligations | Notes |

|---|---|---|

| Resident & Ordinarily Resident (ROR) | Must disclose all foreign assets & income in Schedule FA/FSI | Includes bank accounts, shares, property, trusts |

| RNOR (Resident but Not Ordinarily Resident) | Limited obligations | Depends on stay period, income source |

| Non-Resident Indian (NRI) | India income taxable; disclosure of foreign assets usually not required | But mistakes in residential status often trigger notices |

For a Resident and Ordinarily Resident (ROR), the net is wide. You are taxed on your worldwide income. You must report all your foreign assets and income. There are no ifs or buts.

A Resident but Not Ordinarily Resident (RNOR) has a narrower scope. You are only taxed on Indian income. And foreign income is only taxed if it comes from a business controlled in India. Disclosure requirements are lighter but still exist for certain assets.

A Non-Resident Indian (NRI) is generally in the clear for foreign assets. You are only taxed on income earned in India. You typically do not need to file Schedule FA. So why do so many NRIs get notices? The answer is often a simple mistake. They accidentally qualify as a Resident. They forget to declare their NRI status. Or they have significant Indian income they did not realize was taxable.

When ITR Filing Becomes Mandatory for NRIs

Filing an income tax return is not always mandatory. But for NRIs, the triggers are specific. You must file an ITR if your total income in India exceeds the basic exemption limit. This is currently ₹2.5 lakh for most individuals under 60.

But there is more to it. Even if your income is below this limit, you should consider filing in these situations.

You own significant foreign assets and you qualify as a Resident. This makes Schedule FA mandatory.

You have any income from India that had tax deducted at source, or TDS. Filing a return is how you can claim a refund for any excess tax deducted.

You have carried forward a loss from a previous year. You can only do this if you have filed a return on time.

You are a joint owner of any assets or bank accounts in India. Filing a return creates a clear paper trail of your financial activities.

And most importantly, if you have received a notice from the tax department. Once a notice is issued, filing a return becomes compulsory.

What Must Be Disclosed in Schedule FA

Think of Schedule FA as a detailed inventory list for everything you own abroad. If you are required to file it, you must be thorough. Leaving anything out can be considered non-disclosure.

The schedule requires you to list different types of assets.

Financial interests in any entity. This means shares you hold in foreign companies.

Immovable property. Any house, apartment, or land you own outside India.

Other assets. This is a broad category. It includes things like jewelry, paintings, or other valuable items held overseas.

Accounts in foreign banks. This is a big one. Every single foreign bank account must be declared. You need to provide the bank’s name, the country it is in, and the account number.

For each asset, you need to provide specific details. The maximum value of the asset during the year. The value at the end of the year. And the country where the asset is located.

A crucial point. All values must be converted to Indian Rupees. You must use the RBI’s notified exchange rate for the last day of the financial year. Using the wrong rate is a common error.

Penalties and Risks of Non-Compliance

This is the part everyone fears. And for good reason. The consequences of getting this wrong are serious. The tax department has a powerful toolkit for enforcement.

First, there are penalties under the standard Income Tax Act. If you fail to file your return on time, a late fee applies. It can be five thousand rupees. Or ten thousand if your income is over five lakh rupees. Worse, you lose the ability to carry forward certain losses.

Then there are the notices. A notice under section 142(1) is a simple inquiry. The department asks for information. A notice under section 148 is more serious. It allows the department to reassess your income for past years if they believe you underreported.

But the most severe penalties come from the Black Money Act. This law treats undisclosed foreign income and assets as a separate category of offense. The tax rate is a flat thirty percent. No deductions are allowed. On top of that, a penalty of ninety percent of the tax amount can be levied. That makes the total outflow a staggering one hundred and twenty percent of the value of the undisclosed asset. In extreme cases of willful evasion, there is even a provision for imprisonment.

The recent relief for small assets, those under twenty lakh rupees, is a welcome change. But it does not change the requirement to disclose them in Schedule FA. It only offers protection from the harshest penalties of the Black Money Act.

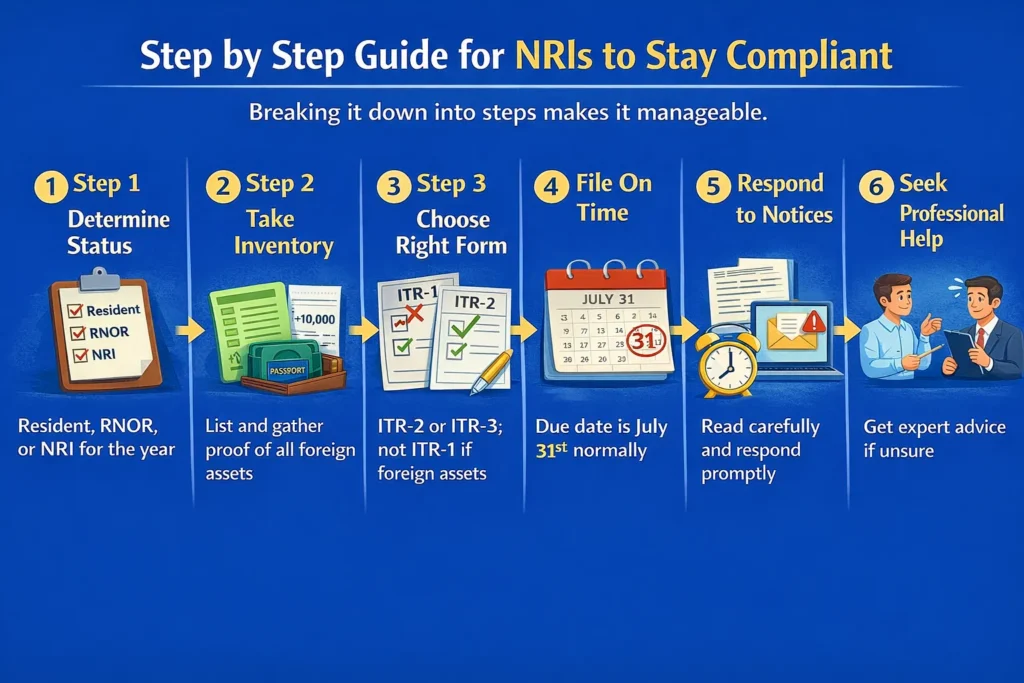

Step by Step Guide for NRIs to Stay Compliant

The rules can feel overwhelming. But compliance is a process. Breaking it down into steps makes it manageable.

Step one: Determine your status. This is the most critical step. Carefully work out if you were a Resident, RNOR, or NRI for the financial year. A small mistake here cascades into every other step.

Step two: Take inventory. Make a list of all your foreign assets. Include bank accounts, investment accounts, property deeds, and any other holdings. Gather your bank statements and other proof.

Step three: Choose the right form. Most people with foreign assets cannot use the simple ITR-1 form. You will likely need ITR-2 or ITR-3. Using the wrong form can lead to your return being labeled defective.

Step four: File on time. The due date for most individuals is July 31st. If you miss it, you can file a belated return. But you will face a late fee and lose certain benefits.

Step five: Respond immediately if you get a notice. Do not ignore it. Do not panic. Read it carefully to understand what information is being asked for. Gather the relevant documents. You can usually respond online through the e-Proceeding tab on the income tax portal.

Step six: Seek help if you need it. The rules are complex. The stakes are high. If you are unsure about your status, your disclosures, or a notice, getting professional advice is a smart investment.

Why NRIs Receive Notices

Understanding why notices are sent can help you avoid them. The tax department is not sending them at random. They are usually triggered by a specific red flag.

The biggest reason is a failure to file Schedule FA when required. This is often because someone mistakenly filed as an NRI when they were actually a Resident.

Another common trigger is a mismatch in data. Under CRS, your foreign bank sends your account info to India. The tax department’s computer systems automatically cross-check this data against your ITR. If your return shows no mention of that account, a notice is automatically generated.

Using the wrong ITR form is a technical trigger. If you have foreign assets but filed using ITR-1, the system will flag it as an incomplete filing.

Sometimes, it is about Indian income. An NRI might have rental income from a property in India. They might think it is not taxable or that the tenant’s TDS is enough. The system may see the income and the lack of a return and send a notice asking for an explanation.

Frequently Asked Questions

What happens if an NRI does not file an ITR?

If they have no obligation to file, nothing happens. But if they were required to file, they face late fees, interest on unpaid taxes, and the risk of receiving a notice. It can also complicate future financial transactions in India.

What is the penalty for not disclosing a foreign bank account?

If you were required to disclose it in Schedule FA and did not, it could be considered a violation under the Black Money Act. The penalties, as discussed, are severe. For a Resident, not disclosing it is a major compliance failure.

Does a Double Taxation Avoidance Agreement (DTAA) remove my disclosure requirements?

No. A DTAA helps you avoid being taxed twice on the same income. It does not remove your obligation to report that income and your assets to the Indian tax authorities. Disclosure and taxation are two separate things.

Can I correct a mistake from a previous year?

Yes, you can. You can file a revised return for a past year if you realize you made an error or omitted something. It is always better to proactively correct a mistake than to wait for the department to find it.

Practical Tips and Best Practices

Staying compliant is easier when you make it a habit. Here are some practical tips.

Always double check your residential status each year. Do not just assume it is the same as last year. The rules are based on your physical presence in India.

Even if your income is below taxable limits, consider filing a return. This creates a clear record. It prevents any mismatch with CRS data and shows you are acting in good faith.

Keep your documentation organized. Maintain separate files for your foreign bank statements, property documents, and investment statements. It will make filing your return much faster.

If your financial life is spread across multiple countries, it is wise to get professional help. The cost of an expert is tiny compared to the cost of a penalty.

If you are planning to move back to India, plan your taxes too. Understand how your residential status will change. Prepare for the new disclosure requirements that will come with being a Resident.

Latest Legal Updates for 2024 and 2025

The law is not static. Recent changes have provided some relief and clarity.

The most significant update is the CBDT’s circular on the Black Money Act. It states that if the total value of all foreign assets, excluding property, is less than twenty lakh rupees at any time during the year, then penalty proceedings under the Act will not be initiated. This is a huge relief for many with modest holdings abroad. Remember, you still must disclose these assets in Schedule FA.

Tax tribunals have also ruled in favor of taxpayers. In some cases, returning NRIs have been protected from harsh penalties for past non-disclosure. The courts recognized that the shift in residency status creates a complex transition.

On the other hand, the tax department is getting more sophisticated. They are sending more targeted notices based on the CRS data they receive. The process is becoming more automated. Compliance is more important than ever.

Conclusion

Navigating the world of foreign asset disclosure and ITR notices can feel like walking through a maze. The rules are detailed. The penalties are stiff. But the path to compliance is straightforward.

It starts with knowing your status. It requires honesty in your disclosures. It demands timeliness in your filings. And it benefits greatly from a proactive approach.

If you are reading this and feeling unsure about your past filings, or if you have a notice sitting in your inbox, do not let the anxiety paralyze you. The worst thing you can do is nothing. Addressing the issue is the first step toward resolving it.

If your situation feels complex, seeking expert guidance can provide clarity and peace of mind. Understanding your obligations is the best way to protect your hard-earned wealth and stay on the right side of the law.

Also Read: 5 Steps to Open an NRI Bank Account in India

Also Read: Received an Income Tax Notice for Political Donation?

Also Read: Common Mistakes That Lead to Tax Notices for NRIs

0 Comments