Getting an income tax notice can feel like a sudden storm on a clear day. Your heart skips a beat. A wave of anxiety hits. For an NRI, this feeling is often mixed with confusion. You are dealing with the tax laws of two countries. A notice from India can seem complicated and frightening.

But here is the secret. Most of these notices are not random audits. They are automated alerts. They are triggered by simple mismatches in your data. The good news? They are almost always avoidable.

This guide breaks down the process into clear, actionable steps. We will show you how to build a solid defense against notices. You will learn how to file correctly, stay compliant, and handle any communication from the tax department with confidence.

Before You File: Build Your Single Source of Truth

Imagine building a house on a shaky foundation. It will not stand for long. Filing your Income Tax Return (ITR) without checking your official data is exactly that. You are building on uncertainty. Your first and most important step is to gather your documents and make them agree with each other.

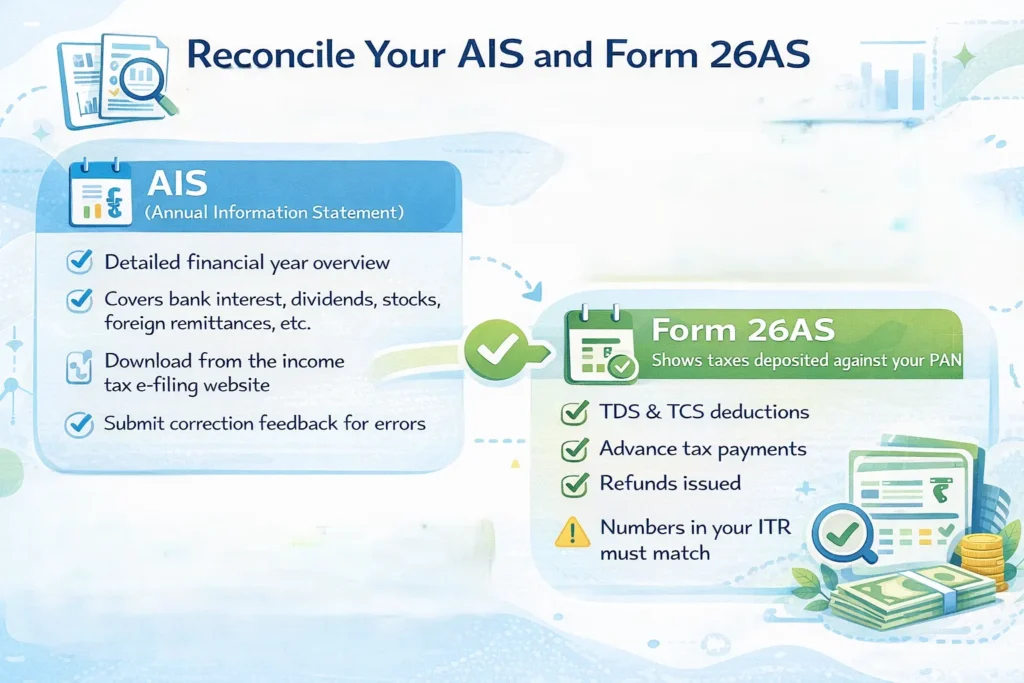

Reconcile Your AIS and Form 26AS

Think of these two documents as your official report card from the Income Tax Department.

- AIS (Annual Information Statement): This is a comprehensive view of your financial year. It includes information reported by banks, brokers, companies, and other institutions. It shows your savings account interest, dividends, stock sales, foreign remittances, and more. You must download your AIS from the compliance portal on the income tax e-filing website. Check every line item. Is that dividend amount correct? Did you really sell those shares on that date? If you see a mistake, use the feedback mechanism to submit a correction. An uncorrected error here is a direct invitation for a notice.

- Form 26AS: This is your tax passbook. It is a consolidated statement that shows all the taxes deposited against your PAN. This includes Tax Deducted at Source (TDS), Tax Collected at Source (TCS), advance tax you paid, and your refund history. The tax department uses Form 26AS as its master ledger. The numbers in your ITR must match the numbers here. No exceptions.

Pro Tip: Do not ignore this. A huge number of mismatch notices, over thirty percent by some estimates, come from people filing returns without first correcting errors in their AIS. Fix the data at the source before it becomes a problem.

Gather Your Personal Financial Statements

Now, lay your own records next to the official ones. Collect your:

- Bank statements for your NRO and NRE accounts.

- Dividend summaries from your DEMAT account.

- Brokerage statements for the financial year.

- Any contract notes for property or other asset sales.

Your goal is simple. Make sure your personal records, your AIS, and your Form 26AS all tell the same story. Any difference is a red flag you must address before filing.

Choosing the Right ITR Form and Schedules

Picking the wrong form is a classic mistake. It is like trying to fit a square peg into a round hole. It will not work and will cause issues.

Step one is always to determine your residential status for the year. Are you a Non-Resident Indian (NRI), a Resident but Not Ordinarily Resident (RNOR), or a Resident? This status is the foundation. It decides which of your incomes are taxable in India. Do not assume last year’s status applies again. The rules are strict and based on your physical presence in India.

For most NRIs, the common ITR forms are:

- ITR-2: This is for you if you have income from salary, house property, capital gains, or other sources like dividends and interest. You use this if you do not have income from a business or profession.

- ITR-3: This is the form you need if you have income from a business or profession.

Filling the form is only half the battle. You must also fill out the correct schedules. This is where many NRIs get tripped up.

- Schedule OS: For reporting ‘Other Sources’ income like interest from NRO accounts.

- Schedule CG: For detailing your capital gains from the sale of shares, mutual funds, or property.

- Schedule FSI: This is crucial. You use this to declare income that you earned outside India but which is taxable in India. You can also claim tax relief under the DTAA (Double Taxation Avoidance Agreement) here.

- Schedule TR: To summarize the details of the tax relief you are claiming under DTAA.

- Schedule FA: This is the most misunderstood schedule. You only need to fill Schedule FA (Foreign Assets) if you are a Resident or an Ordinarily Resident. Most NRIs do not need to file this. However, if you returned to India during the year and became a resident, you might have to. This confusion leads to many errors.

NRI Income Buckets That Often Trigger Notices

Certain types of income are common minefields for NRIs. The tax department watches these closely.

NRO Account Interest and Dividends

The interest earned on your NRO savings account is fully taxable in India. The bank will deduct TDS, usually at over thirty percent. This TDS will show up in your Form 26AS. You must report the full interest income and then claim credit for the TDS already deducted. A common mistake is to only report the net interest received after TDS. This creates a mismatch. The department sees the full income in AIS and the TDS in 26AS, but your return shows a lower number. Notice.

Capital Gains from Shares, Mutual Funds, or Property

This is a major trigger zone. The AIS automatically captures your stock and fund transactions. The problem? It often gets the purchase price, or cost of acquisition, wrong. It might show as zero or an incorrect amount. If you simply accept this data and file, you might end up showing a massive capital gain that you never actually earned.

You must correct this through the AIS feedback system. You need to provide the correct contract notes and details. Once corrected, you can file your return with the accurate capital gains calculation.

Rental Income from Indian Property

If you own a property in India that you are renting out, you must report that rental income. The law requires your tenant to deduct TDS on the rent they pay you. They must also file Form 26QC and deposit the TDS. This TDS should then be visible in your Form 26AS.

You must ensure the rent you declare matches the rent the tenant reported. And the TDS credit you claim must match what is in 26AS. If your tenant did not deduct TDS, you are still liable to pay the tax on your rental income. The responsibility is yours.

Outward Remittances (Sending Money Abroad)

Sending money from India to your overseas account? The bank will ask for compliance with Section 195 of the Income Tax Act. This means the bank or you must determine if the remittance is taxable. If it is, TDS must be deducted before the money is sent.

This process involves filing Form 15CA and, in many cases, a certificate from a chartered accountant in Form 15CB. This entire trail is closely monitored. Skipping this process or getting it wrong is a surefire way to get the department’s attention.

TDS Rules Every NRI Must Understand

Tax Deducted at Source is at the heart of most notices. The rule for payments to NRIs is straightforward but strict.

Section 195 states that any person in India making a payment to an NRI must deduct TDS before making the payment, if the income is taxable in India. This applies to:

- A buyer purchasing your property.

- A tenant paying you rent.

- A company paying you dividends.

- A person paying you for freelance services.

The most common errors here are:

- The buyer of your property did not deduct TDS at the correct rate, which is often twenty percent for long-term capital gains.

- Your tenant did not deduct TDS on rent or did not file Form 26QC.

- The TDS was deducted but under a wrong PAN, so it does not show up in your Form 26AS.

Your only proof that TDS was deposited in your name is Form 26AS. If the credit is not there, you cannot claim it. You might have to pay the tax again and then fight to get a refund from the deductor.

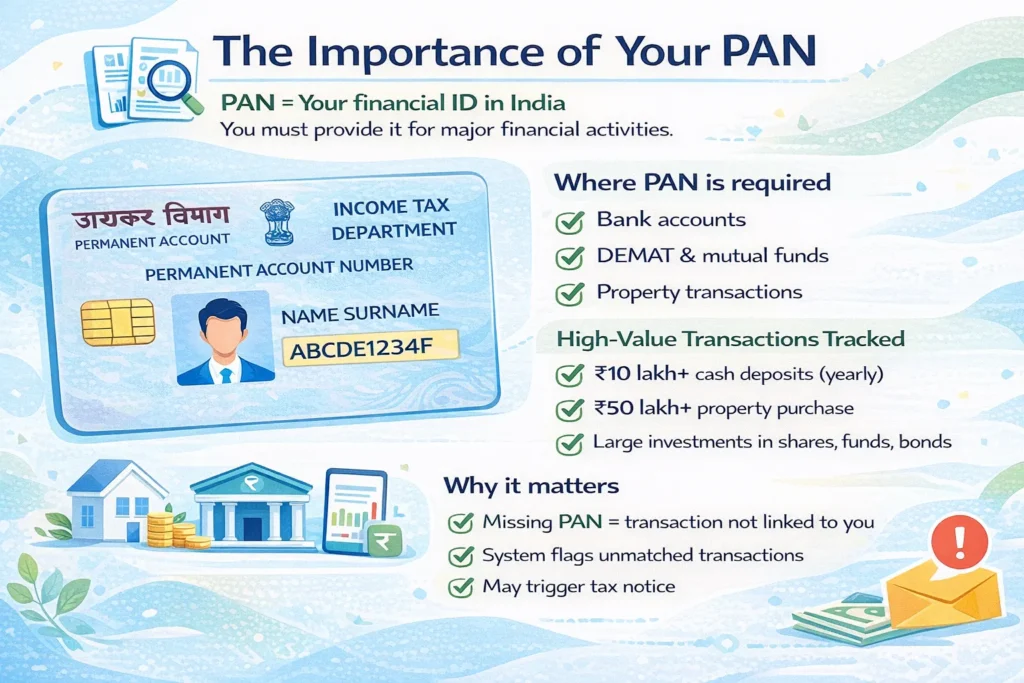

The Importance of Your PAN

Your Permanent Account Number is your financial identity in India. You must quote it everywhere.

- In all your bank accounts.

- For your DEMAT and mutual fund investments.

- In all property transactions.

The system is wired to flag high-value transactions that are not linked to a PAN. The Annual Information Statement (AIS) and Statement of Financial Transaction (SFT) systems automatically pick up transactions like:

- Cash deposits aggregating to ten lakh rupees or more in a savings account in a year.

- Purchase of property valued at fifty lakh rupees or more.

- High-value investments in shares, mutual funds, or bonds.

If your PAN is missing, the system cannot link the transaction to you. This creates an information gap. The department’s automated system might see a high-value transaction but no corresponding ITR or income disclosure. This gap often results in a notice.

The e-Campaign and Compliance Portal: Your Early Warning System

The tax department has moved away from sending surprise notices. They now often start with a softer nudge. This is the e-Campaign on the compliance portal.

What is it? It is a pre-notice alert. The department’s system identifies transactions in your AIS that do not seem to match your filed ITR. They send you a message in your e-filing account. It might say something like, “We have information about a high-value savings account deposit. Please confirm and explain.”

This is not a formal notice. It is your chance to fix things before it becomes one.

How do you handle it?

- Log in to your e-filing account and go to the compliance portal.

- You will see the items under campaign.

- You can select a feedback category – “Already disclosed in ITR,” “Not taxable,” “Not correct,” etc.

- You can upload proof like bank statements or explanations.

- Based on your response, you can align your already filed ITR or file a revised return if needed.

The most critical thing here is the deadline. You usually have only ten to fifteen days to respond. Ignoring this message is the worst thing you can do. It tells the system that you are not responding, and it will almost certainly escalate to a formal notice under section 133(6), 142(1), or worse.

Your Step-by-Step NRI Compliance Workflow

Let us put it all together into a simple, yearly workflow you can follow.

- Determine Your Status: First, confirm your residential status for the financial year.

- Download Your Documents: Get your AIS and Form 26AS from the e-filing portal.

- Reconcile Everything: Sit down with your NRO/NRE bank statements, brokerage statements, and rental documents. Match them line by line with your AIS and 26AS.

- Fix Errors: Use the AIS feedback system to correct any wrong information. Do this immediately.

- Verify TDS: Scrutinize your Form 26AS. Does it show all the TDS credits from your tenant, your buyer, and your bank? If something is missing, follow up with the deductor to correct it.

- Handle Remittances: For any money you sent abroad, ensure you have the Form 15CA/CB documentation in order.

- Choose and File: Select the correct ITR form (ITR-2 or ITR-3) and fill out all necessary schedules accurately.

- Pay and File: Pay any advance tax or self-assessment tax liability. Then file your return well before the deadline.

- Monitor: After filing, periodically check your e-filing account for any e-Campaign messages. Respond to them promptly.

Best Practices Checklist

Keep this checklist handy every time you file your taxes.

- Always review your AIS and Form 26AS before you even start preparing your return.

- Never claim a TDS credit that is not visibly present in your Form 26AS.

- Quote your PAN in every single financial transaction you undertake in India.

- Understand and ensure compliance with Section 195 TDS for any payments you receive from India.

- Keep your proofs organized. This includes TDS certificates, foreign inward remittance certificates (FIRCs), rent agreements, and property sale deeds.

- Treat any e-Campaign message from the income tax portal with utmost urgency. Respond before the deadline.

Special Situations for NRIs

Selling a Property in India: The buyer is legally obligated to deduct TDS at twenty percent on any long-term capital gains. They often do not know this. You must inform them. If your total income is low and the capital gains tax rate is less than twenty percent, you can apply to the tax department for a lower TDS certificate under Section 197.

Earning Freelance or Digital Income Abroad: If you are a resident under Indian tax laws, your global income is taxable in India. This includes foreign freelance income. You must disclose this income in your ITR. You can then claim a tax credit in India for any taxes you paid on that income in your country of residence, provided there is a DTAA between the two countries.

Returning to India: Your first year of becoming a resident again is a critical transition year. You must now start reporting your global income in India. Pay special attention to the requirement for filing Schedule FA, which details your foreign assets and signing authority. The Indian tax year is April to March, so you will need to pro-rate your foreign income for the part of the year you were a resident.

Frequently Asked Questions

How should I respond to an income tax notice as an NRI?

Do not panic. Read the notice carefully to understand the section under which it is issued and what information is being asked for. Gather all relevant documents like your ITR, AIS, 26AS, and proof of transactions. Prepare a clear and concise point-by-point response. If the matter is complex, it is wise to consult a tax professional.

What is an NRI TDS mismatch?

This is the most common issue. It happens when the TDS amount you claimed in your ITR does not match the TDS amount shown in your Form 26AS. This usually occurs because the deductor made an error, such as quoting a wrong PAN or not depositing the TDS.

Do NRIs need to fill out Schedule FA?

Generally, no. Schedule FA is for reporting foreign assets only if you are a Resident and Ordinarily Resident (ROR) of India. Most NRIs are non-residents or RNORs and are exempt from this requirement. However, if you have returned to India and qualify as a ROR, you must fill it.

Why is PAN so important for NRIs?

Your PAN is the unique identifier that links all your financial transactions in India. Without it, the tax department cannot match your income and taxes correctly. Missing PAN in high-value transactions almost guarantees a query from the department.

Can you explain TDS on payments to NRIs simply?

Any person in India making a payment to an NRI must deduct TDS before sending the money if the income is taxable in India. The rate can vary. For example, it is twenty percent for long-term capital gains on property. The deductor is responsible for this. Your job is to ensure they do it correctly and that the TDS appears in your Form 26AS.

Conclusion

The Indian tax system is becoming more and more data-driven. The goal is not to harass taxpayers but to improve compliance through technology. For an NRI, the key to a peaceful life is alignment.

Make your financial statements, your AIS, your Form 26AS, and your ITR all tell the same story. Pay attention to TDS. Take the e-Campaigns seriously. Keep your documents ready.

Do this, and you will build a strong wall of compliance. This will keep you off the tax department’s radar and allow you to focus on what matters most to you.

0 Comments