Navigating the Indian tax system can feel confusing from afar. You hear different rules. You are not sure what truly applies to you.

If you are a Non-Resident Indian earning an income in India, knowing your tax liability is the first step to smart financial planning. This guide breaks down the exact income tax slabs, surcharges, and cess for the Financial Year 2024-25. We will use clear numbers and real world examples so you can estimate your tax with confidence.

Let us get started.

Why Understanding NRI Tax Rules Matters

You might think tax rules are the same for everyone. For the most part, they are. But the devil is in the details.

NRIs are taxed on the same slab rates as resident Indians. However, a critical difference exists. NRIs are only taxed on income that is earned in India or received in India. Your global income is not taxable here.

Your official residential status under the Income Tax Act is what decides this. Getting this status wrong is a common mistake. It can lead to reporting income you do not need to.

Furthermore, NRIs cannot claim certain tax rebates available to residents, like Section 87A. And perhaps most importantly, the final tax amount is not just the slab rate. Surcharges and a cess stack on top, significantly increasing your total tax outgo. Missing these can lead to a nasty surprise when you file your return.

Income Tax Slabs for NRIs (FY 2024-25 / AY 2025-26)

For FY 2024-25, NRIs have the same two tax regime options as residents: the Old Regime and the New Regime. You must choose one. The New Regime is now the default, but you can opt for the Old Regime if it benefits you more.

Here are the exact slab rates.

Old Tax Regime

| Income Range (₹) | Tax Rate |

|---|---|

| Up to 2,50,000 | Nil |

| 2,50,001 – 5,00,000 | 5% |

| 5,00,001 – 10,00,000 | 20% |

| Above 10,00,000 | 30% |

Note: The rebate under Section 87A is not available for NRIs, even if your total income is below ₹5 lakh.

New Tax Regime

| Income Range (₹) | Tax Rate |

|---|---|

| Up to 3,00,000 | Nil |

| 3,00,001 – 6,00,000 | 5% |

| 6,00,001 – 9,00,000 | 10% |

| 9,00,001 – 12,00,000 | 15% |

| 12,00,001 – 15,00,000 | 20% |

| Above 15,00,000 | 30% |

Remember, these are just the basic slab rates. Your final tax bill will include a surcharge and a cess on top of this amount.

NRI Surcharge Rates for FY 2024-25

A surcharge is an additional tax on your income tax. It kicks in when your total income crosses specific high-value thresholds. For NRIs, these rates are the same as for residents.

| Total Income (₹) | Surcharge Rate |

|---|---|

| Up to 50 lakh | Nil |

| 50 lakh – 1 crore | 10% |

| 1 crore – 2 crore | 15% |

| 2 crore – 5 crore | 25% |

| Above 5 crore | 37% |

There is a concept called marginal relief that prevents your total tax from jumping suddenly when you cross an income threshold. But for general planning, use these rates.

Let us make this simple. Imagine your total income is ₹1.2 crore. First, you calculate your tax using the slab rates. Let us say that comes to ₹30 lakh. Now, because your income is between ₹1 crore and ₹2 crore, you add a 15% surcharge on this tax.

So, surcharge = 15% of ₹30 lakh = ₹4.5 lakh.

Your tax plus surcharge is now ₹34.5 lakh. But we are not done yet.

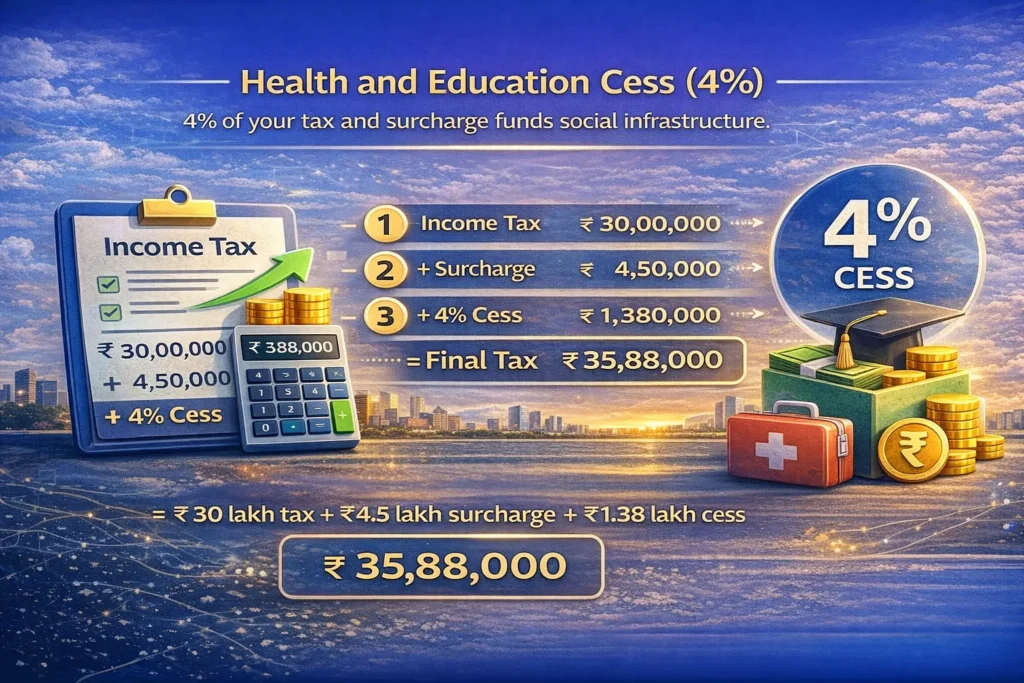

Health and Education Cess (4%)

After you have calculated your income tax and added the surcharge, the government applies a flat 4% Health and Education Cess on the total. This cess is used to fund social infrastructure projects.

It is a small percentage, but it adds up.

Using our previous example, your tax plus surcharge was ₹34.5 lakh. Cess = 4% of ₹34.5 lakh = ₹1.38 lakh.

So, your final tax liability becomes ₹34.5 lakh + ₹1.38 lakh = ₹35.88 lakh.

You can see how the initial tax of ₹30 lakh ballooned by over ₹5.8 lakh due to the surcharge and cess.

Capital Gains Tax for NRIs (FY 2024-25)

Selling assets in India? This is where NRI taxation gets particularly detailed. The tax you pay on profits from selling assets like stocks, mutual funds, or property depends entirely on the type of asset and how long you held it.

Here is a breakdown.

| Asset Type | Holding Period | Tax Type | Tax Rate |

|---|---|---|---|

| Equity Shares / Equity Mutual Funds | More than 12 months | Long-Term Capital Gains (LTCG) | 12.5%* |

| Equity Shares / Equity Mutual Funds | 12 months or less | Short-Term Capital Gains (STCG) u/s 111A | 15% |

| Debt Mutual Funds / Bonds / Property | More than 24 or 36 months | Long-Term Capital Gains (LTCG) u/s 112 | 20% with indexation benefits |

| Other Capital Assets | Short-term | Short-Term Capital Gains | As per your income tax slab |

Please verify the final LTCG rate from the official Finance Act 2024 documents once released.

A Note on Exemptions: NRIs can claim exemptions under Sections 54, 54F, and 54EC when they sell a house or other long-term assets. For instance, if you sell a residential property and reinvest the capital gains into another house or specified bonds, you can save on tax. There are limits, like a ₹10 crore cap on the new residential property and ₹50 lakh for bonds.

Example: Property Sale by an NRI

An NRI sells an apartment in Mumbai for ₹2 crore. The property was purchased years ago, so it qualifies as a long-term asset. After calculating the indexed cost of acquisition, the capital gain is determined to be ₹80 lakh.

- LTCG Tax @ 20% = ₹16 lakh.

- Assuming total income places them in the 25% surcharge bracket: Surcharge = 25% of ₹16 lakh = ₹4 lakh.

- Tax + Surcharge = ₹20 lakh.

- Cess @ 4% on ₹20 lakh = ₹80,000.

- Total Tax Payable = ₹20,80,000.

Also, remember that the buyer will deduct TDS (Tax Deducted at Source) at 12.5% of the sale value, which in this case would be ₹25 lakh. You will then claim a refund for the excess TDS when you file your ITR.

Deductions and Exemptions for NRIs

Can NRIs reduce their tax bill? Absolutely. But you need to know which deductions you are still eligible for.

Eligible Deductions for NRIs:

- Section 80C: You can claim deductions up to ₹1.5 lakh for investments in ELSS mutual funds, LIC premiums, or repayment of the principal amount of a home loan. Important: You can continue contributing to a PPF account you opened before becoming an NRI, but you cannot open a new one.

- Section 80D: Premiums paid for health insurance for yourself, your family, or your parents are eligible. The limit is generally ₹25,000 for self and family, and an additional ₹25,000 for parents.

- Section 80E: The interest paid on an education loan for higher studies is fully deductible.

- Section 80G: Donations made to certain charitable institutions and funds are eligible for deduction.

- Section 80TTA: Interest income from a savings bank account up to ₹10,000 is deductible.

Deductions NRIs are NOT Eligible For:

- New PPF accounts.

- National Savings Certificate (NSC).

- Senior Citizen Savings Scheme (SCSS).

- Deductions for disability (Section 80U, 80DD).

- Deduction for medical treatment of a dependent with a specified disease (Section 80DDB).

Choosing the right regime depends heavily on whether you have substantial deductions to claim.

Old vs New Tax Regime: Which Should NRIs Choose?

This is the million dollar question. The New Regime offers lower slab rates but comes with very few opportunities for deductions. The Old Regime has higher slab rates but allows you to reduce your taxable income significantly.

Let us look at some scenarios. Assume a 4% cess is applied in all cases.

Scenario 1: NRI with a salary of ₹15 lakh and no deductions.

- Old Regime Tax: Approximately ₹2,62,500

- New Regime Tax: Approximately ₹1,87,200

- Better Option: New Regime

Scenario 2: NRI with a salary of ₹15 lakh and ₹1.5 lakh under Section 80C.

- Old Regime Tax (on ₹13.5 lakh taxable income): Approximately ₹2,32,500

- New Regime Tax: Approximately ₹1,87,200

- Better Option: New Regime is still better, but the gap narrows.

Scenario 3: NRI with a salary of ₹15 lakh, ₹1.5 lakh under 80C, and ₹2 lakh home loan interest (80EEA).

- Old Regime Tax (on ₹11.5 lakh taxable income): Approximately ₹1,77,500

- New Regime Tax: Approximately ₹1,87,200

- Better Option: Old Regime

The bottom line? If you have significant deductions, primarily from a home loan, the Old Regime might be better. For most other NRIs, especially those with just a salary and no major investments in 80C instruments, the New Regime is simpler and more tax efficient.

Worked Examples: Step-by-Step NRI Tax Calculations

Let us tie everything together with detailed examples.

Example 1: NRI with Salary Income

- Total Income: ₹12,00,000 (from salary in India)

- Regime Chosen: New Tax Regime

- Deductions: None

- Calculate Slab Tax:

- Up to ₹3,00,000: Nil

- ₹3,00,001 to ₹6,00,000: 5% of ₹3,00,000 = ₹15,000

- ₹6,00,001 to ₹9,00,000: 10% of ₹3,00,000 = ₹30,000

- ₹9,00,001 to ₹12,00,000: 15% of ₹3,00,000 = ₹45,000

- Total Slab Tax = ₹90,000

- Surcharge: Income is below ₹50 lakh, so surcharge = Nil.

- Cess: 4% of ₹90,000 = ₹3,600.

- Total Tax Payable = ₹93,600.

- Effective Tax Rate = (93,600 / 12,00,000) * 100 = 7.8%.

Example 2: NRI with Long-Term Capital Gains

- Total Income: ₹55,00,000 (comprising ₹5 lakh other income + ₹50 lakh LTCG from equity shares)

- LTCG Tax Calculation:

- LTCG on equities = ₹50,00,000.

- LTCG Tax @ 12.5% = ₹6,25,000.

- Tax on Other Income: Using slabs, tax on ₹5 lakh is ₹12,500 (under old regime for illustration).

- Total Tax before Surcharge: ₹6,25,000 (LTCG) + ₹12,500 = ₹6,37,500.

- Surcharge: Total income exceeds ₹50 lakh. Surcharge = 10% of ₹6,37,500 = ₹63,750.

- Tax + Surcharge = ₹7,01,250.

- Cess: 4% of ₹7,01,250 = ₹28,050.

- Total Tax Payable = ₹7,29,300.

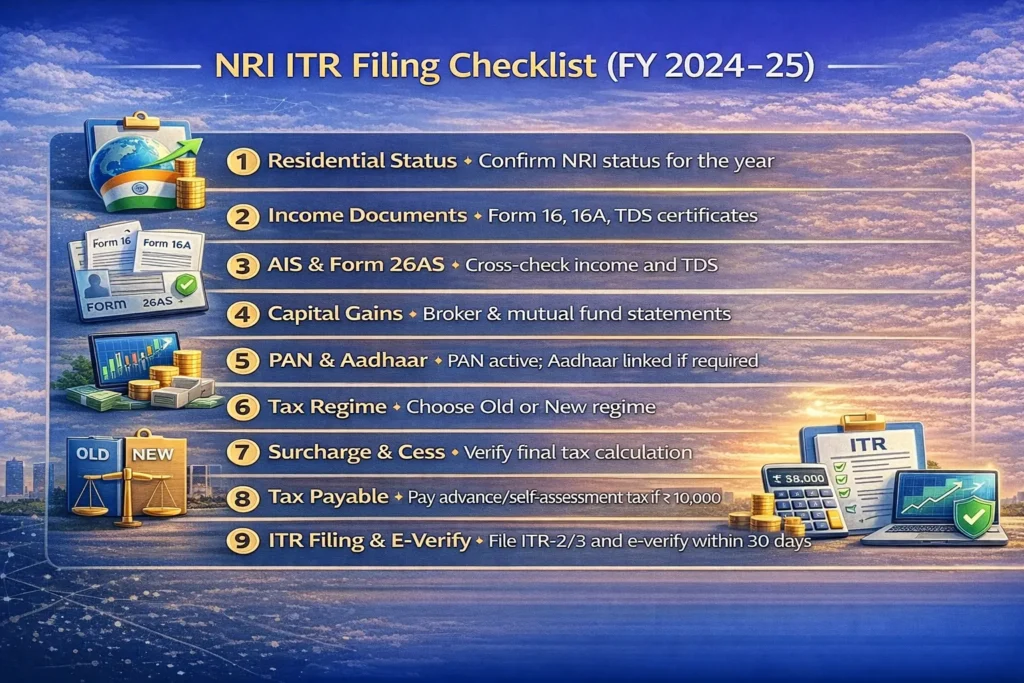

NRI ITR Filing Checklist (FY 2024-25)

Before you hit the submit button on your ITR, run through this list.

- Confirm your residential status for FY 2024-25.

- Collect all your Indian income documents: Form 16 from your employer, Form 16A for TDS on other income, and TDS certificates.

- Download your AIS (Annual Information Statement) and Form 26AS to cross-check all reported income and TDS.

- Gather capital gains statements from your stockbroker or mutual fund house.

- Ensure your PAN is active and your Aadhaar is linked if needed.

- Decide conclusively between the Old and New tax regime.

- Double-check your calculation for surcharge and cess.

- If your total tax liability after TDS exceeds ₹10,000, you may need to pay advance tax or self-assessment tax.

- File the correct ITR form (likely ITR-2 or ITR-3) and remember to e-verify it within 30 days to complete the process.

Frequently Asked Questions

Do NRIs get the Section 87A rebate of ₹12,500?

No. The tax rebate under Section 87A is available only to Resident Individuals.

Are NRIs taxed on their foreign income?

No. As an NRI, you are only taxed on the income that accrues or arises in India, or is received in India. Your foreign income is not taxable in India.

Do surcharge and cess apply to NRIs?

Yes, absolutely. The surcharge rates and the 4% health and education cess apply to NRIs in the exact same way they apply to resident taxpayers.

Can NRIs claim 80C deductions?

Yes, NRIs can claim deductions under Section 80C for specific investments made in India, such as ELSS, LIC, and principal repayment on a home loan, subject to the ₹1.5 lakh limit.

How can NRIs avoid double taxation?

India has Double Taxation Avoidance Agreements (DTAAs) with many countries. You can use these treaties to claim tax relief. You may get a tax credit in your country of residence for the taxes you paid in India, or vice-versa, depending on the treaty terms.

What is the LTCG tax rate for NRIs on shares after Budget 2024?

The government has proposed a uniform LTCG tax rate of 12.5% for all listed equities. However, you must always verify the final rate from the enacted Finance Act 2024.

0 Comments