The idea of buying a property back home is powerful. It is more than just an investment. It is a tangible connection to your roots, a plan for your future return, and a source of pride.

But from thousands of miles away, the process can feel murky. You hear stories. Stories about legal trouble, delayed projects, or tax headaches. The excitement quickly mixes with a nagging worry. Am I doing this right?

It does not have to be that way.

With the right information, you can make a decision that is both smart for your wallet and peaceful for your mind. This guide walks you through the six most important things you need to know. Let us break it down, step by step.

Understand Legal Eligibility & Regulatory Framework

Before you even look at a single property listing, you need to understand the rules of the game. The laws governing property ownership for Non-Resident Indians are specific, but they are clear.

The good news is, as an NRI, you are generally allowed to buy any residential or commercial property in India. There is just one big exception. You cannot buy agricultural land, plantation property, or a farmhouse. That is reserved for Indian residents. This rule is set by the Foreign Exchange Management Act, or FEMA. It is the primary law that dictates how NRIs can deal with property and money in India.

Think of it like a guest list for a private event. You are welcome to join the main party (buying apartments, plots, offices), but the VIP backroom (agricultural land) is off-limits.

FEMA Rules & Allowed Property Types

FEMA is your friend. It clearly defines what you, as an NRI, can and cannot do.

- You CAN buy: Any residential apartment, a plot of land to build a house on, or a commercial space like a shop or office. You do not need any special permission. You can pay for it using money from your NRE (Non-Resident External) or NRO (Non-Resident Ordinary) accounts, or by sending funds from abroad.

- You CAN inherit: If a relative passes away and leaves you agricultural land, you are allowed to inherit it. You can even hold onto it. You just cannot buy it directly yourself.

- You CAN sell: You can sell any property you own to either a resident Indian or another NRI.

Getting this foundation right is the first and most critical step. A mistake here can lead to serious legal complications down the line.

RERA Compliance & Title Verification

Now, let us talk about your safety net. A few years ago, buying a property under construction was a huge gamble. You never knew if the builder would actually finish it. Then, the Indian government introduced a powerful law called RERA, the Real Estate (Regulation and Development) Act.

RERA is like a strict referee for the real estate game.

Its job is to protect you, the homebuyer. Here is how it works. Every new real estate project above a certain size must be registered with a state’s RERA authority. The builder has to provide all project details—the layout, completion timeline, exact apartment sizes, and even how they will spend your money.

Before you sign anything, you must check if the project is RERA-registered. You can easily find this on the official RERA website for the state where the property is located. Look for a unique registration number. The builder is legally required to mention this number in all their ads and documents.

Why is this so important?

- No False Promises: The builder cannot promise a swimming pool and then not build it. What is on the RERA website is what you get.

- Your Money is Safer: Builders must keep 70% of the money they collect from buyers in a separate bank account. This money can only be used for that specific project’s construction costs. It prevents them from using your money to start another project elsewhere.

- Strict Penalties for Delays: If the builder delays possession, they have to pay you interest for every month of delay.

Along with RERA, always do a title verification. This is a legal check to confirm the person selling the property is the real owner and that there are no existing loans or legal disputes attached to it. I always recommend hiring a local lawyer you trust to do this for you. It is a small cost that can save you from massive problems.

Decide Purpose, Location & Property Type

Why are you buying this property? Your answer to this simple question will guide every other decision you make. The strategy is completely different for each goal.

- Is this for your own future use? Maybe you plan to move back to India in 5 years. In this case, you should focus on location, connectivity, and quality of life. Think about being close to family, good hospitals, and maybe a quieter neighborhood. A ready-to-move-in property might be better to avoid construction delays.

- Is this purely for rental income? Here, your focus shifts to yield. You want a property in a high-demand area, probably near business districts, colleges, or IT parks. An apartment in a well-connected area might be easier to rent out than a large, independent house. You are thinking like a business owner.

- Is this for short-term price appreciation? You are betting on the growth of a specific area. This is riskier. You might look at upcoming neighborhoods where new infrastructure like a metro line or highway is being built. This can be profitable, but it requires deep market research and a higher risk appetite.

I recently spoke to an NRI friend who bought a plot in his hometown because he felt emotionally connected to the place. But his goal was rental income. A plot of land generates no rent. It was a mismatch between his goal and his investment. He realized it too late. Be very clear about your why.

Financial Planning: Payment, Loans & Repatriation

Money matters can get tricky when you are dealing with cross-border transactions. Planning ahead is non-negotiable.

Payment: The easiest and most transparent way to pay for a property in India is by using funds from your NRE account. This account holds your foreign earnings in Indian rupees, and the money in it is fully repatriable, meaning you can take it back out of India. You can also use your NRO account, but the rules for taking money out are stricter.

Loans: Yes, NRIs can get home loans from Indian banks. Most major banks have special NRI home loan schemes. They will look at your income, credit history in your country of residence, and employment stability. The loan amount will typically be disbursed directly to the builder or seller, not to you. Remember, you can only service this EMI through your NRE or NRO accounts.

Repatriation: This is a big one. Repatriation means taking the sale proceeds of your property out of India and back to your country of residence.

The rules are straightforward but important:

- You can repatriate the money you used to buy the property. There is a limit, usually up to the amount you originally brought in from abroad to buy it.

- You can only repatriate the sale proceeds from a maximum of two properties in your lifetime.

- You must have held the property for at least a certain period, which is a minimum of three years.

- You need to provide documents like the sale deed, tax clearance certificates, and a certificate from a Chartered Accountant confirming all taxes have been paid.

Think of repatriation like a round trip for your money. You need to keep all your tickets (proof of original investment) and get your exit stamp (tax clearances) before you can board the flight back.

Taxation & TDS: From Rental Income to Capital Gains

Taxes in India can seem complicated. But for an NRI property owner, it mainly boils down to two situations: earning rent and selling the property.

1. If you earn Rental Income: The rent you receive is taxable in India. It is added to your total income and taxed as per the Indian income tax slabs. You are also allowed to deduct certain expenses like property taxes, society maintenance charges, and a standard 30% deduction for repairs. You must file an income tax return in India for this rental income.

2. If you Sell the Property: This is where Capital Gains Tax comes in. The profit you make from the sale is called a capital gain. The tax you pay depends on how long you held the property.

- Short-Term Capital Gain (STCG): If you sell the property within two years of buying it, the profit is considered “short-term.” It is added directly to your income and taxed at your applicable income tax slab rate. This is usually higher.

- Long-Term Capital Gain (LTCG): If you sell the property after holding it for more than two years, the profit is “long-term.” This is taxed at a lower rate, which is currently 20% with indexation. Indexation is a helpful concept. It adjusts your purchase price for inflation over the years you held the property. This higher “indexed” cost means your taxable profit is lower, so you pay less tax.

The TDS Trap: This is very important. When an NRI sells a property, the buyer is legally required to deduct TDS (Tax Deducted at Source) before paying you.

- For STCG, the TDS rate is as per your income tax slab.

- For LTCG, the TDS rate is a flat 20% (plus surcharge and cess), which can be over 23%.

Many NRIs are unaware of this. The buyer deducts this large amount and pays it to the government. You only get the remaining money. To get a refund for any excess tax deducted, you have to file your tax return later. This can create a cash flow problem. To avoid this, you can apply to the Indian tax department in advance for a lower TDS certificate, which allows the buyer to deduct a much smaller amount.

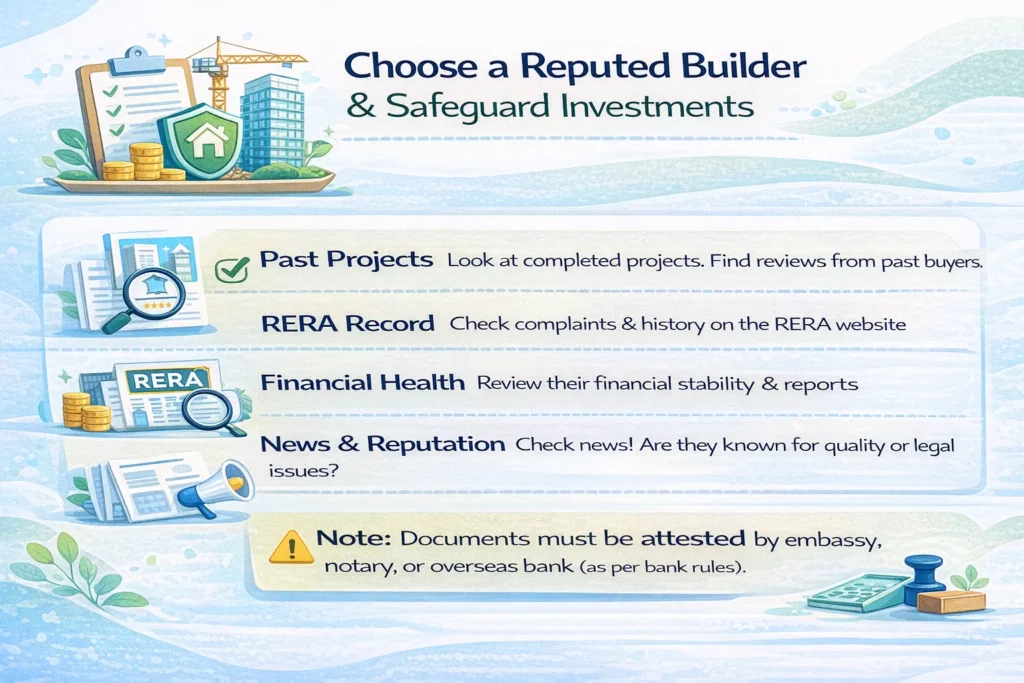

Choose a Reputed Builder & Safeguard Investments

Your builder’s reputation is your biggest insurance against stress. A fancy brochure means nothing. You need to look for a track record of delivering projects on time.

How do you check a builder’s credibility?

- Past Projects: Look at projects they have already completed. Can you find reviews from people who live there? Try to contact them.

- RERA Record: Check the RERA website not just for the current project, but for the builder’s other projects. Have there been many complaints against them?

- Financial Health: Is the builder a publicly listed company? If so, their financial reports are available. A stable financial background is a good sign they can complete the project.

- News and Reputation: A simple online search can reveal a lot. Have they been in the news for positive reasons or for legal disputes with customers?

I remember reading a news article about an NRI who invested in a Hyderabad apartment in 2010. The project got delayed for years. While the property’s value did increase over a long period, the stress and lost opportunity cost were immense. He regretted not checking the builder’s history more carefully. A good builder is worth their weight in gold.

Manage Property Remotely: POA & Property Management

You have bought the property. Congratulations. But now, you are back in the US, Canada, or the UAE. How do you manage it from there?

The key is a Power of Attorney (POA). A POA is a legal document that gives another person the authority to act on your behalf. You can give a trusted family member or friend in India a POA to handle tasks like:

- Registering the property.

- Dealing with tenants.

- Collecting rent.

- Paying maintenance fees and property taxes.

You can make the POA specific, limiting their powers only to certain tasks. It is crucial to draft this document carefully with a lawyer. For it to be valid for property registration, it often needs to be executed at the Indian Embassy in your country of residence or notarized locally and then apostilled.

If you do not have a trusted person, you can hire a property management company. These companies act as your local representative for a fee. They find tenants, handle repairs, and ensure your property is well-maintained. It is a hands-off solution that gives you peace of mind.

FAQs

Can an NRI get a home loan in India?

Yes, most Indian banks offer home loans to NRIs. The loan is disbursed in India and must be repaid through your NRE or NRO accounts.

What is the difference between NRE and NRO accounts for property investment?

An NRE account is best for investing because the funds are fully repatriable. An NRO account is for managing income earned in India, like rent, and repatriation from it has limits.

Are there any restrictions on how many properties an NRI can buy?

No, there is no limit. An NRI can buy any number of residential or commercial properties. The restriction is only on the type (no agricultural land).

What happens if I become a resident of India again?

The FEMA rules for NRI property ownership will no longer apply to you. You will be treated as a resident Indian for all future property transactions.

0 Comments