Navigating tax season can feel like walking a tightrope. You are balancing rules from two different countries. One misstep, one forgotten date, and you could face penalties. The pressure is on.

For Non-Resident Indians, this is your annual reality. Your financial life is spread across borders. So are your tax responsibilities. The deadlines in India and the United States do not line up. It is easy to get confused. It is easy to miss a date.

This guide cuts through the noise. We have highlighted the five most critical deadlines you need to track in 2025. We will cover what you owe to India and what you owe to the U.S. Let us build your compliance calendar together, so you can file with confidence and avoid costly mistakes.

Overview: Why These Deadlines Matter

Think of tax deadlines as gates at a train station. If you arrive on time, you board smoothly and your journey continues without a hitch. If you arrive late, the gate is closed. You are left on the platform, watching your train leave. Now you must pay a fee to get on a later, less convenient train.

That fee is a penalty. Governments charge them for late payments and late filings. These penalties are not just small fines. They can grow over time, accruing interest. They can lead to notices and stressful legal letters. In severe cases, they can even affect your visa status or your ability to get loans.

But it is not just about penalties. Missing deadlines can mean losing out on benefits. For example, if you do not file the right form on time, you might pay a higher tax on your Indian income than necessary. You are leaving money on the table.

Staying on top of these five dates is the simplest way to protect your hard-earned money and your peace of mind. Let us break them down one by one.

1. Pay Self-Assessment Tax in India — by July 31

This is arguably the most important date in the Indian tax calendar. Many people confuse filing their return with paying their tax. They are two separate actions. The deadline to pay any remaining tax you owe for the financial year is July 31.

What is Self-Assessment Tax?

Throughout the year, tax is often deducted at source from your income. Your bank deducts it from your interest. Your tenant deducts it from your rental income. But this might not cover your entire tax liability. Self-assessment tax is the final amount you calculate and pay directly to the government to settle your dues for the year.

Why This Date is Non-Negotiable

I recently spoke with an NRI who thought the extended ITR filing deadline also applied to the payment. He was wrong. The government may give you more time to file the paperwork, but it wants its money on time.

If you do not pay your self-assessment tax by July 31, you will be charged interest from August 1 onwards. This interest is calculated under Section 234A of the Income Tax Act. It adds up quickly. There is no way to avoid this interest once the deadline passes. It is an automatic penalty for late payment.

Actionable Tip: By mid-July, gather all your documents. Calculate your total income and tax liability. If you see a shortfall, log into the income tax e-filing portal and pay the balance immediately. Do not wait until the last week. Treat July 31 as your absolute final date to settle your tax bill for the previous year.

2. File ITR in India — extended deadline: September 15

Now for the paperwork. The deadline to file your Income Tax Return in India for most NRIs is typically July 31. However, for the financial year 2024 , the government has extended this deadline to September 15. This gives you an extra six weeks to prepare and submit your return.

Who Needs to File?

You must file an Indian tax return if your total taxable income in India exceeds the basic exemption limit. This includes income from rent, capital gains from selling property, or interest from savings and fixed deposits.

What Happens if You File Late?

The extended deadline is a gift. Use it. But what if you miss even September 15? You can still file a belated return. The last date for this is December 31. However, it comes with a cost.

Filing a belated return attracts a late fee. The penalty can be up to Rs. 5,000. Furthermore, you lose the ability to carry forward certain losses from your investments. It is like showing up to a party after the main event is over. You can still get in, but you have missed the best parts.

Actionable Tip: Use the window between July 31 and September 15 wisely. Once you have paid your self-assessment tax by July 31, you can methodically gather your Form 16s, bank statements, and capital gains reports to file an accurate return without the last-minute rush. An accurate return is better than a hasty, mistake-filled one filed under pressure.

3. U.S. Income Tax Deadline for NRIs

This is where things get a little more layered for U.S. based NRIs. The U.S. tax system gives you a few different deadlines, depending on your situation. Your key form is the Form 1040-NR, the U.S. Nonresident Alien Income Tax Return.

April 15 – Standard deadline

This is the default tax deadline for everyone in the United States. It is deeply ingrained in the American system. If you are an NRI who was physically present in the U.S. on this date, this is your deadline.

June 15 – Automatic extension for NRIs abroad

Here is a crucial break specifically for you. If you are living outside the United States on April 15, you get an automatic two-month extension to file your return and pay any tax due. Your new deadline becomes June 15.

I want to emphasize the word automatic. You do not need to file any form to request this extension. It is a built-in benefit for taxpayers abroad. However, there is a small catch. If you owe any tax, the IRS will still charge you interest on that amount from the original April 15 deadline. The extension is for filing, not necessarily for paying in full.

October 15 – With Form 4868 filed

Need even more time? You can get it. If June 15 is still too soon, you can file Form 4868, the Application for Automatic Extension of Time to File. This pushes your filing deadline all the way to October 15.

This is a true filing extension. It gives you extra time to gather your documents and complete your 1040-NR. But remember, it is not an extension to pay. You must make a good faith estimate of your tax liability and pay most of it by the June 15 deadline to avoid significant interest and penalties.

Actionable Tip: Mark your calendar based on your location. If you will be in the U.S. in mid-April, aim for April 15. If you are in India or elsewhere, your main deadline is June 15. If you know you will need more time, file Form 4868 online before June 15 to secure your October 15 extension.

4. FBAR & FATCA Reporting Deadlines (U.S.)

This is the deadline that often causes the most anxiety. It is not an income tax return, but a report of your foreign financial accounts. It is about disclosure.

What Are FBAR and FATCA?

- FBAR (Foreign Bank Account Report): This is Form FinCEN 114. If the total value of all your foreign financial accounts (like bank accounts in India, brokerage accounts, etc.) exceeded $10,000 at any point during the year, you must file this report. It goes to the U.S. Treasury Department, not the IRS.

- FATCA (Foreign Account Tax Compliance Act): This is Form 8938. It is filed with your 1040-NR tax return. It has higher threshold amounts than the FBAR, but it serves a similar purpose: telling the IRS about your foreign assets.

The Deadlines

The FBAR deadline is aligned with the federal tax deadline. It is due on April 15. But because you are abroad, you automatically get an extension to October 15. You do not need to file a separate form for this FBAR extension.

Since Form 8938 is attached to your tax return, its deadline is the same as your 1040-NR deadline. So it is either June 15 or October 15, depending on your situation.

Why This is Critical

The penalties for failing to file the FBAR are severe. They can be staggering. We are not talking about a small fee. Civil penalties can run into the tens of thousands of dollars for non-willful violations, and can even exceed the balance in the account for willful violations. It is the U.S. government’s way of ensuring it knows about your global financial footprint.

Actionable Tip: Do a yearly review of all your non-U.S. financial accounts around March. Tally their combined maximum value. If you crossed the $10,000 threshold, note it down. When you file your U.S. taxes, file your FBAR electronically at the same time. Treat it as part of your annual U.S. tax compliance package, not as an optional extra.

5. Filing Form 10F and Tax Residency Certificate for DTAA Benefits

This deadline is different. It is not a fixed calendar date. It is an event-based deadline, and getting it right can save you a lot of money.

What is DTAA?

The Double Taxation Avoidance Agreement is a treaty between India and the U.S. It prevents you from being taxed twice on the same income. For example, the interest you earn from an Indian fixed deposit is typically taxed in India at a high rate. But under the DTAA, you can often claim a lower rate because you are a U.S. tax resident.

The Role of Form 10F and TRC

To claim these lower rates, you need to prove your tax residency. You do this by providing two documents to the Indian payer (like your bank):

- Tax Residency Certificate (TRC): Issued by the U.S. government, this certifies you are a tax resident of the United States.

- Form 10F: A form you submit to the Indian income tax department with details from your TRC.

The “Deadline”

There is no official due date like July 31. The deadline is practical. You should submit these documents to your bank before the income is credited or the tax is deducted.

Think of it like a coupon. If you give the coupon to the cashier before they ring up the total, you get the discount. If you try to give it to them afterwards, it is too late. The higher tax has already been deducted. You would then have to go through the lengthy process of filing a refund claim later.

Actionable Tip: Do not wait. As soon as you have your U.S. Tax Residency Certificate for the year, fill out Form 10F and submit both documents to your Indian banks and other financial institutions. Do this at the beginning of the financial year, in April if possible. This ensures that from the very first interest payment, tax is deducted at the correct, lower DTAA rate.

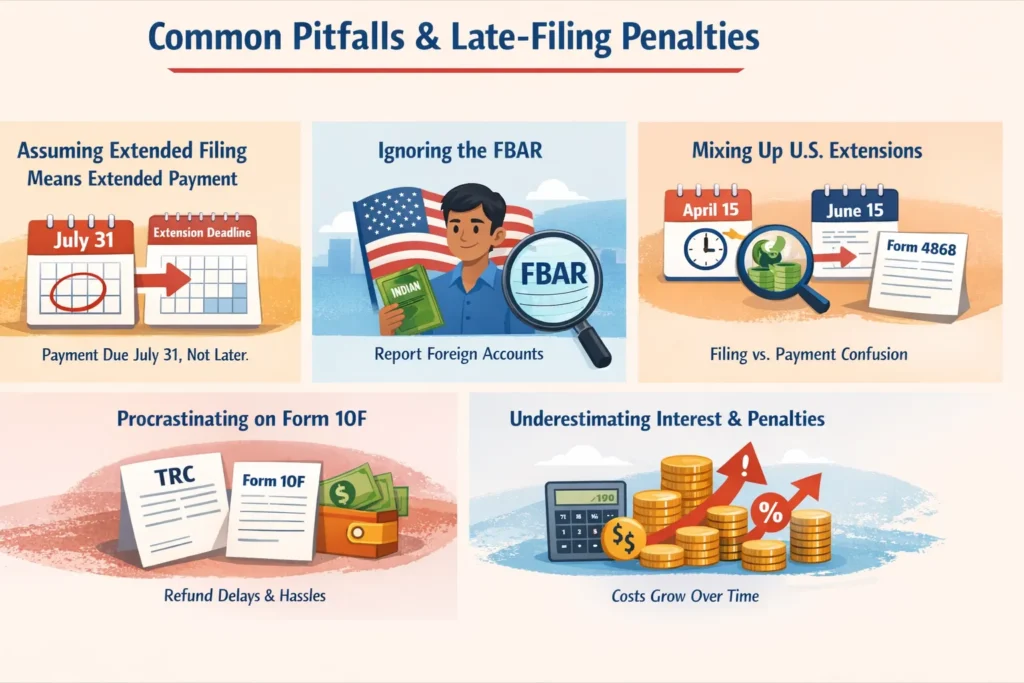

Common Pitfalls & Late-Filing Penalties

Let us look at where most NRIs stumble. Knowing these traps is the first step to avoiding them.

- Assuming Extended Filing Means Extended Payment: This is the most common and costly mistake. Remember, in India, the payment deadline of July 31 is set in stone. The extended filing deadline is a separate benefit.

- Ignoring the FBAR: Many NRIs think their Indian bank accounts are irrelevant to the U.S. This is false. The FBAR reporting requirement is separate from your tax liability. You must report the accounts even if they generated no income.

- Mixing Up U.S. Extensions: The automatic extension to June 15 is for filing, but interest on unpaid tax still runs from April 15. The October 15 extension requires a form. Confusing these can lead to unexpected interest charges.

- Procrastinating on Form 10F: Waiting until you receive a tax deduction to submit your TRC and Form 10F means you have already lost money. You are now in refund territory, which is always slower and more frustrating.

- Underestimating Interest and Penalties: These are not one-time fees. Interest compounds, and penalties can be a percentage of the tax owed, making a small problem a very big one over time.

0 Comments