You check your email. Or maybe a letter arrives at your old Indian address, forwarded by a relative. Your heart skips a beat. The subject line reads “Notice under Section 143(1)” or something more ominous like “Notice under Section 148.”

A wave of panic hits you. You live thousands of miles away. Tax rules are complicated. And the Indian tax department has your name on a notice.

Take a deep breath. Receiving an income tax notice is not the end of the world. It is not an accusation. It is often just a request for information, a mismatch in records, or a simple clarification. But ignoring it? That can lead to real problems.

This guide is your calm, step-by-step manual. We will walk you through exactly how to understand, verify, and respond to an income tax notice as an NRI. We will cover the specific triggers that affect NRIs and show you how to build a strong response.

What Is an Income Tax Notice for NRIs?

An income tax notice is an official communication from the Income Tax Department of India. It is sent to a taxpayer, which includes NRIs who have income sources in India. The key thing to remember is that a notice is not a penalty. It is a start of a conversation.

The department might need more information, want to point out an error they found, or ask you to explain a transaction. Think of it as a flag on the play. It means the system has noticed something that does not quite match their records, and they are asking you to clarify.

There are several types of notices, but as an NRI, you are most likely to encounter these:

- Intimation under Section 143(1): This is the most common one. It is not a full scrutiny notice. It is an automated message showing the result of the initial processing of your tax return. It might show a tax demand if they found a calculation error or a mismatch between your filed return and their data (like Form 26AS).

- Notice under Section 142(1): This is a notice asking for more information. The department might need additional documents, books of account, or other details to process your return.

- Notice under Section 148: This is a serious one. It gives the department the right to reassess your income if they believe you have not fully disclosed it for a particular year. This often comes after they find evidence of high-value transactions you did not report.

- e-Campaign Notices: These are not formal notices but proactive emails or SMS alerts from the department. They highlight specific discrepancies (like missing income in your return) and ask you to respond voluntarily. Ignoring these can lead to a formal notice.

You can view official information on these notices on the Income Tax Department website.

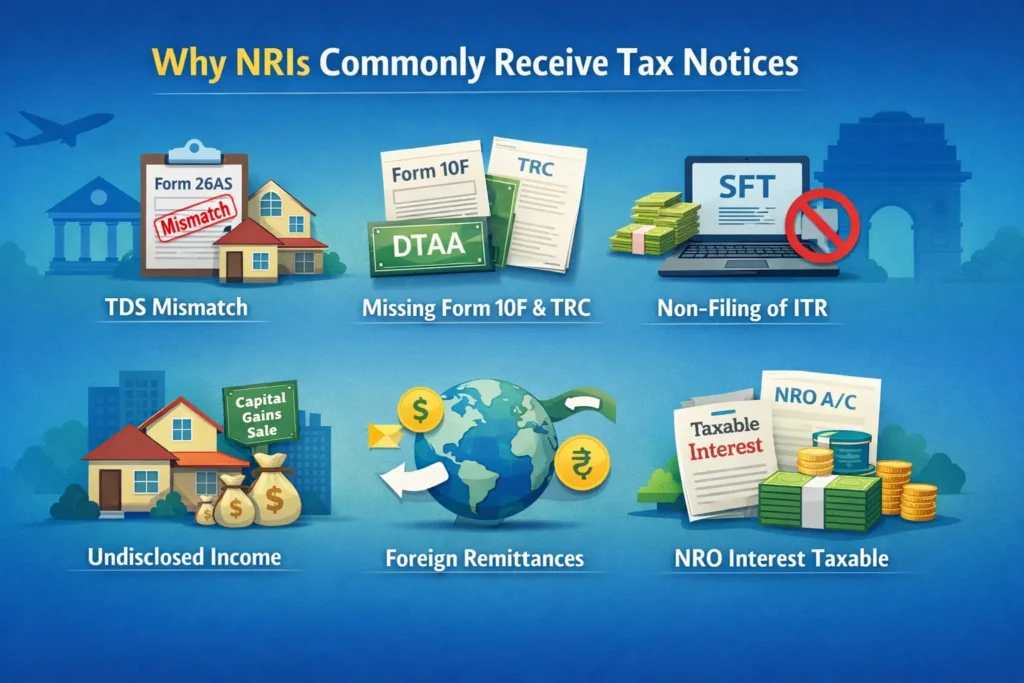

Why NRIs Commonly Receive Tax Notices

Why you? You try to be compliant. The reasons are often technical and specific to the NRI situation. According to recent data, over 150,000 income tax notices were issued to NRIs in 2024 alone. The most common triggers are:

- TDS Mismatch: This is a huge one. A tenant or a bank deducts TDS from your rental or interest income but quotes the wrong PAN or forgets to deposit it. Your Form 26AS does not show this credit, so the department thinks you did not pay tax on that income.

- Missing Form 10F or Tax Residency Certificate (TRC): If you are claiming tax benefits under a DTAA (Double Taxation Avoidance Agreement), you must submit Form 10F and your TRC to the Indian payer. If you do not, the payer will deduct TDS at a higher rate (often 20% or more). The department then sees this high TDS and may ask why you are claiming a refund for it without the proper documents.

- Non-Filing of ITR Despite SFT: The department gets information from banks and other institutions (called Statement of Financial Transactions or SFT). If your NRE/NRO account shows high-value transactions (large deposits, big investments) but you did not file a return, they will send a notice asking why.

- Undisclosed Rental Income or Capital Gains: You sold a property in India or own one that is rented out. The buyer deducts TDS on the sale, or the tenant deducts TDS on rent. This data is with the tax department. If you did not file a return reporting this income, they will notice.

- Foreign Remittances: While money you send abroad from NRO accounts is not taxable, the remittance itself is a high-value transaction that gets reported. This can sometimes trigger a query.

- Assuming All NRI Income is Exempt: A classic mistake. Not all income you earn as an NRI is exempt. Interest from NRE and FCNR deposits is tax-free, but interest from NRO deposits is fully taxable. Many NRIs forget to report their NRO interest income.

Step-by-Step Response Process for NRIs

When you get that notice, do not panic. Follow this process methodically.

1. Read the Notice Carefully

Your first job is to understand what the notice is about. Do not skim it. Read every word. Look for three critical pieces of information:

- Assessment Year (AY): Which financial year is this notice for?

- Section Number: What is the section under which the notice is issued? This tells you the nature of the notice (e.g., 143(1), 148, 142(1)).

- Response Deadline: What is the last date to respond? This is usually 15, 21, or 30 days from the date of issue. Mark this date in your calendar immediately.

Also, look for the Document Identification Number (DIN). Every legitimate notice will have a unique DIN. If it does not, it might be a scam.

2. Verify Authenticity

Unfortunately, tax scams are common. You must confirm the notice is real before you act on it.

Go to the Income Tax e-Filing portal. Look for the “Authenticate Notice / Order” tool under the “Quick Links” section. Enter the DIN from your notice. The portal will confirm if the notice is genuine and show you its details. This simple step can save you from phishing attacks and fraud.

3. Gather Documents

Now, build your defense. Your response is only as strong as your supporting documents. Gather everything you need based on the notice’s query. Here is a checklist:

- Form 26AS: This is your consolidated tax statement. It shows all TDS deducted on your income and taxes paid. This is your primary document to reconcile any mismatches.

- AIS/TIS (Annual Information Statement): This is even more detailed than Form 26AS. It shows information about your savings account interest, dividends, foreign remittances, and other transactions reported by financial institutions.

- Bank Statements: For your NRO, NRE, and any other Indian accounts. These can prove the nature of transactions and the source of funds.

- TDS Certificates: Forms 16, 16A from your employer, tenant, or bank.

- Past Income Tax Returns (ITRs): For the relevant year and previous years for context.

- Tax Residency Certificate (TRC) and Form 10F: Absolutely crucial if the notice is about a DTAA claim or higher TDS deduction.

- Property Documents: Sale deed, purchase agreement, if the notice is about property sale or purchase.

- Proof of NRI Status: Passport copies with immigration stamps, employment visa, to prove your residential status.

4. Login to e-Filing Portal (e-Proceedings)

For most notices, the response must be filed online. The days of physical replies are mostly over.

Log in to your account on the Income Tax India e-Filing portal. Go to the “Pending Actions” tab and click on “e-Proceedings”. You should see the notice listed there with an option to respond. This is your official channel for communication. Ensure your registered email and mobile number are up to date so you never miss an alert.

5. Draft and Upload Your Reply

This is the core of your response. Be factual, concise, and attach all relevant proofs.

For a common 143(1) intimation showing a demand, your reply might look like this:

- Acknowledge: “This is in response to your intimation u/s 143(1) for AY 2024-25 bearing DIN XYZ.”

- Explain the Discrepancy: “The demand of ₹X,XXX arises due to a mismatch in TDS claimed. As per my Form 26AS (attached), the TDS of ₹Y,YYY on my fixed deposit income was not reflected in the department’s system at the time of processing.”

- Provide Evidence: “I have attached the following documents for your kind perusal: 1) Form 26AS, 2) TDS certificate from the bank (Form 16A), 3) Bank statement highlighting the credit.”

- Request Action: “Kindly consider the attached documents and take necessary action to rectify the demand.”

If the notice is more complex, like under Section 148, you may need to file a revised return or submit a detailed letter explaining your income. The tone should always be respectful and professional.

6. Submit Before Deadline and Track

Do not wait until the last day. Submit your response well before the deadline. Once you submit, you will receive an acknowledgment number. Save this number. It is your proof that you responded on time.

You can track the status of your response in the same “e-Proceedings” section. The case may be closed, or the department might ask for more information. Check the portal regularly.

Missing the deadline is a bad idea. It can lead to a best-judgment assessment under Section 144, where the tax officer calculates your income without your input, which always results in a higher tax demand.

Penalties and Consequences of Non-Response

Ignoring a tax notice is the worst thing you can do. The consequences can be severe and expensive.

- Penalty for Non-Compliance: A penalty of ₹10,000 can be levied for failing to comply with a notice.

- Interest: You will be charged interest under Section 234A, B, and C for any tax paid late, adding a significant amount to your bill.

- Reassessment: Under Section 144, the Assessing Officer can pass an order based on their best judgment, which will likely assume the highest possible income.

- Loss of DTAA Benefits: If you do not submit your TRC and Form 10F in response to a notice, you could lose your right to claim tax treaty benefits.

- Legal Action: In extreme cases of tax evasion, the department can initiate prosecution proceedings.

Here is a simple comparison of what different failures can cost you:

| Action | Potential Consequence |

|---|---|

| Late filing of return | Late fee under Section 234F (₹5,000 if filed after Dec 31) |

| Not filing a return | Penalty of up to 50% of the tax evaded + prosecution risk |

| Ignoring a notice | Penalty of ₹10,000 + best-judgment assessment + interest |

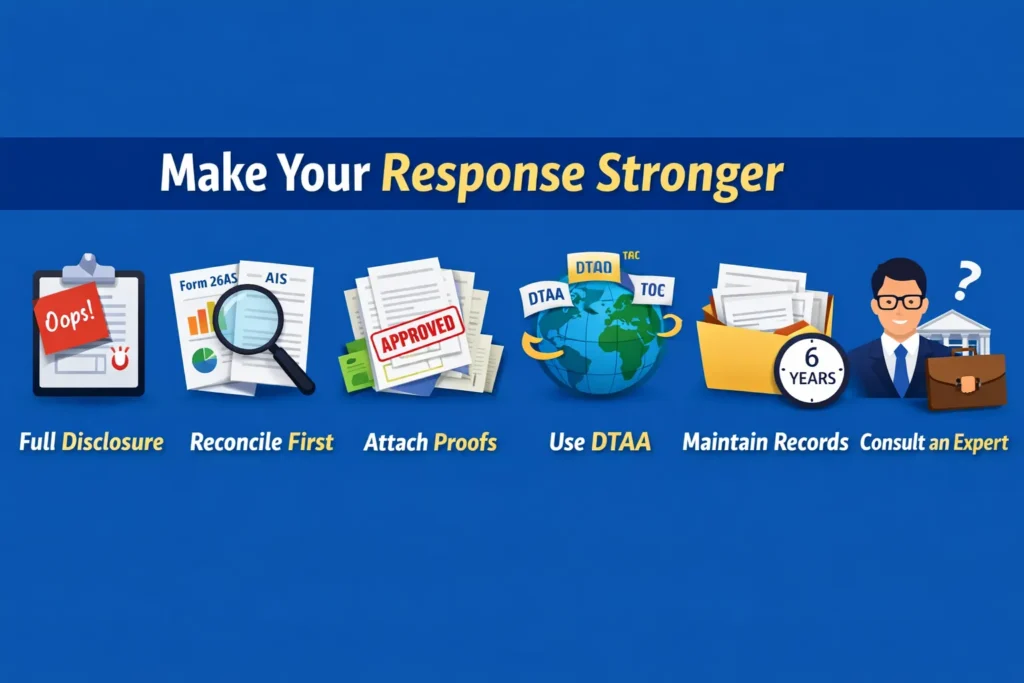

How to Make Your Response Stronger

A good response solves the immediate problem. A strong response prevents the next one.

- Full Disclosure: Be transparent. If you made a mistake, acknowledge it and correct it. Hiding information will only make it worse later.

- Reconcile First: Before you even file your return, reconcile it with your Form 26AS and AIS. This prevents most 143(1) notices.

- Attach Proofs: Do not just state facts. Prove them with bank statements, certificates, and forms.

- Use DTAA Correctly: If you are a tax resident of another country, understand the DTAA rules. Submit your Form 10F and TRC to the payer before receiving the income to avoid high TDS.

- Maintain Records: Keep all your financial documents, including proof of NRI status, for at least six years.

- Consult an Expert: For notices under serious sections like 148, or if your income situation is complex (foreign assets, multiple properties), it is wise to hire a CA who specializes in NRI taxation. They know the language of the department and can craft the most effective response.

FAQs for NRIs

Can I respond to an Indian tax notice from abroad?

Yes, absolutely. The entire process is online through the e-Filing portal. You can respond from anywhere in the world with an internet connection.

What if my total income is below the taxable limit?

Even if your income is below taxable limit, if you have received a notice, you must respond. You can explain your case and provide documents to show that your income was not taxable.

Is Form 10F and TRC mandatory for all NRIs?

It is mandatory only if you are claiming tax benefits under a DTAA to avoid paying higher tax in India. If no TDS was deducted at a higher rate and you are not claiming a refund based on DTAA, you may not need it for a notice. But if the notice is about a DTAA claim, you must submit it.

What happens if I miss the response deadline?

The department may pass an order against you, creating a tax demand with penalties and interest. However, you can still respond late with a condonation request, explaining the reason for the delay. It is better to respond late than never.

Can I ignore an e-Campaign notice?

Technically, it is not a formal notice, so there is no immediate penalty for ignoring it. But it is a strong warning. Ignoring it almost guarantees you will receive a formal, legally binding notice under sections like 142(1) or 148 soon after.

Also Read: Notices for Foreign Asset Disclosure & Non-filing of Returns—What NRIs Need to Know

0 Comments