Someone tells you: "The moment you land in India permanently, you lose all your NRI tax benefits."

Your stomach drops. You start doing the math on your foreign salary, your UK rental income, your FCNR deposits. And the numbers look terrifying.

Here is the good news. That statement is not entirely true.

The tax impact of returning to India depends entirely on which of the three tax statuses applies to you NRI, RNOR, or Resident. And the difference between them is not just academic. It can mean legally saving lakhs of rupees over two to three years. Understanding the RNOR vs NRI vs resident tax status comparison is one of the most important things a returning NRI can do before booking that one-way ticket home.

This blog breaks down all three statuses, compares them on the income types that actually matter, and helps you figure out which one works in your favour.

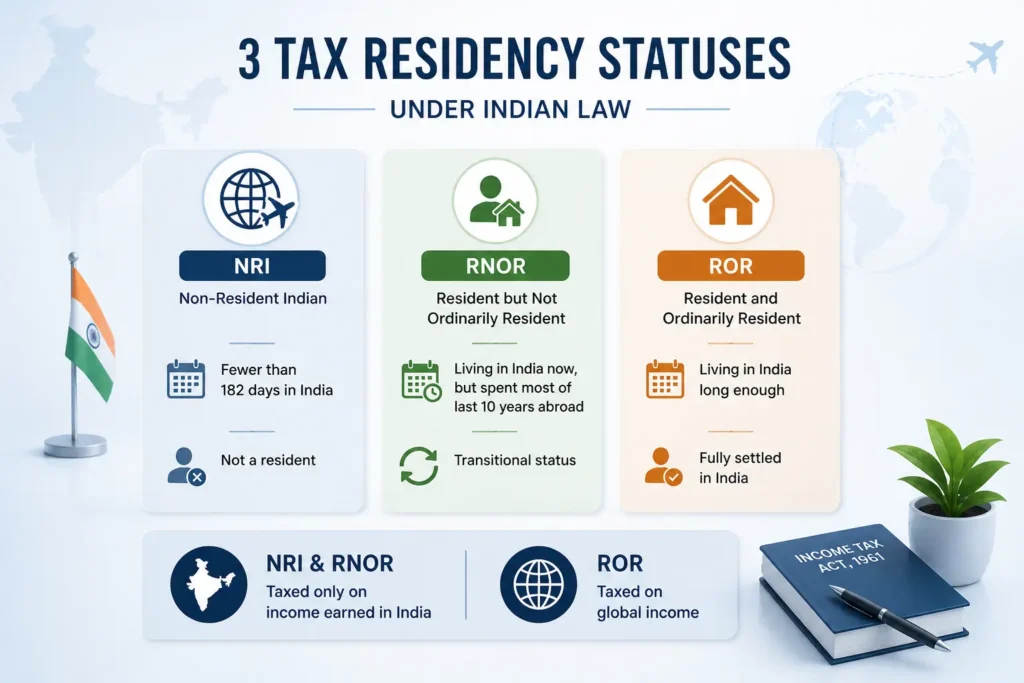

The Three Tax Residency Statuses Under Indian Law: A Plain English Summary

Here is something most people get wrong. Your tax status in India is not determined by your citizenship or your passport. It is determined by your residential status under the Income Tax Act. Every financial year, the law looks at where you spent your time and labels you accordingly.

There are three possible labels:

NRI (Non-Resident Indian): You spent fewer than 182 days in India during the financial year. You are not a resident. Simple.

RNOR (Resident but Not Ordinarily Resident): You are now physically living in India. You are technically a resident. But your history shows you spent most of the last decade abroad. So the law gives you a transitional status.

ROR (Resident and Ordinarily Resident): You are a full resident. You have been living in India long enough that the law considers you fully settled here.

Now here is the one sentence that matters most: NRI and RNOR are taxed only on income earned in India. ROR is taxed on global income.

That single difference is what makes RNOR so valuable for returning NRIs.

How Each Status Is Determined: The Day Count Rules

The three statuses are determined by Section 6 of the Income Tax Act. Here is how the counting works for each.

| Status | Key Condition | Who This Typically Is |

|---|---|---|

| NRI | Fewer than 182 days in India in the financial year (or fewer than 120 days if Indian income exceeds Rs. 15 lakh) | Someone still based abroad, visiting India occasionally |

| RNOR | Now resident in India, but was non-resident in 9 of the last 10 financial years OR was in India for 729 days or fewer across the last 7 financial years | Someone who has just returned after a long stint abroad |

| ROR | Does not meet NRI or RNOR conditions; has been resident long enough to become "ordinarily resident" | Someone who has been back in India for several years and no longer meets RNOR conditions |

The transition sequence works like this. You spend years abroad as an NRI. You return to India. For the first two to three years, you are typically RNOR. And then, once your overseas history fades from the look-back window, you become ROR.

It is a gradual shift. Not an overnight cliff. And the RNOR stage in the middle is where the tax planning opportunity lives.

Under Indian tax law, NRIs and RNORs are taxed only on income earned in India, while Residents (ROR) are taxed on their global income. RNOR is the most tax-efficient status for someone who has returned to India, as it combines physical presence with foreign income exemption typically for 2 to 3 financial years.

For a deeper explanation of RNOR eligibility conditions and how the window works, read our full RNOR guide for returning NRIs.

The Core Comparison: What Gets Taxed Under Each Status

This is the table that answers the question everyone is actually asking. Which income gets taxed, and which doesn't, depending on your status.

| Income Type | NRI | RNOR | ROR |

|---|---|---|---|

| Foreign salary / employment income | Not taxable in India | Not taxable in India | Taxable in India |

| Rental income from overseas property | Not taxable in India | Not taxable in India | Taxable in India |

| Capital gains from foreign assets (stocks, property) | Not taxable in India | Not taxable in India | Taxable in India |

| Interest on NRE account | Not taxable | Not taxable (until re-designation) | Taxable |

| Interest on FCNR deposit | Not taxable | Not taxable during RNOR period | Taxable |

| Interest on NRO account | Taxable in India | Taxable in India | Taxable in India |

| Indian rental income | Taxable in India | Taxable in India | Taxable in India |

| Capital gains from Indian assets | Taxable in India | Taxable in India | Taxable in India |

| Dividends from Indian mutual funds / stocks | Taxable in India | Taxable in India | Taxable in India |

The insight jumps out immediately. NRI and RNOR are almost identical in how foreign income is treated. The massive gap is between RNOR and ROR.

Here is what makes RNOR so powerful: it gives you NRI-level foreign income protection while you are already living in India. You are home. Your kids are in school. You are sleeping in your own bed. And your foreign income is still not being taxed. That combination is the whole point of the RNOR status.

Real Examples: How Much Tax Each Status Actually Saves

Numbers make this real. Here are three illustrative examples using FY 2025-26 as the base year. These are approximate figures to show the concept actual tax depends on individual circumstances, applicable slabs, and DTAA provisions.

Example 1: The Returning Professional

Rohan spent 12 years working in the US. He returns to India in April 2025. His foreign salary for FY 2025-26 is Rs. 40 lakh. He also has FCNR interest of Rs. 3 lakh.

- As NRI (if he had managed India days below 182): Foreign salary and FCNR interest both not taxable in India. India tax = Rs. 0 on these.

- As RNOR (which he actually qualifies for after returning): Foreign salary and FCNR interest still not taxable. India tax = Rs. 0 on these.

- As ROR (what he would be if RNOR didn't exist): Rs. 43 lakh added to his taxable income. At the 30% slab plus surcharge, the tax liability on just this foreign income could exceed Rs. 13 to 15 lakh.

The RNOR window, for Rohan, could save Rs. 13 to 15 lakh per year for 2 years. That is not a small number.

Example 2: The Property Owner Abroad

Meera owns a flat in London generating rental income of Rs. 12 lakh per year. She has returned to India.

- As NRI: UK rental income not taxable in India.

- As RNOR: UK rental income still not taxable in India.

- As ROR: Rs. 12 lakh added to Indian taxable income. Even after standard deduction, the tax could be Rs. 3 to 3.5 lakh per year. However, if UK tax was already paid on this income, Meera can claim foreign tax credit using Form 67 under the India-UK DTAA, which reduces the net India liability. But it still creates compliance work and some residual tax.

The lesson: RNOR removes the problem entirely. ROR requires you to manage it through DTAA which works, but adds complexity.

Example 3: The NRI Who Overstayed Without Planning

Vikram visits India for what he thinks is a "long holiday." He ends up spending 200 days in India in FY 2025-26. His Indian income is Rs. 5 lakh, but his foreign dividend income is Rs. 18 lakh.

He does not qualify as RNOR because he did not meet the look-back conditions (he had been returning to India frequently in previous years). He is now ROR.

His Rs. 18 lakh foreign dividend income becomes fully taxable in India. At applicable slab rates, that is Rs. 5 to 6 lakh in additional tax. Entirely avoidable with better planning.

Disclaimer: The above examples use illustrative round figures and are not tax advice. Actual tax liability depends on individual circumstances, current income tax slabs, surcharge, applicable DTAA provisions, and deductions. Please consult a qualified NRI tax advisor for your specific situation.

When Is It Better to Stay NRI Rather Than Return as RNOR?

This is the question nobody asks out loud. But it is a genuinely valid one.

Staying NRI by carefully managing your India visit days below the 182-day threshold is sometimes the smarter move. Here is when.

When your RNOR window would be very short. If your residency history is borderline (say, you have been visiting India heavily for the last few years), you might only get one year of RNOR after returning. In that case, the tax benefit is limited and the complexity of managing the transition may not be worth it. Staying NRI for another year or two while letting the look-back window strengthen your future RNOR eligibility could be better.

When your foreign income is very high and ongoing. If you earn Rs. 80 lakh or more from overseas sources, and you are not yet ready to permanently return, staying NRI is tax-efficient. You pay zero Indian tax on that income indefinitely, as long as you stay below the day count threshold.

When your India income is minimal. NRI status restricts certain Indian investment options, but if your India income is small and you have no strong reason to shift investments, the restrictions may be worth tolerating for the tax benefit.

On the other hand, RNOR is clearly the better choice when you have already decided to return, when your RNOR window will cover 2 full financial years, and when you have significant foreign income to protect during the transition.

The choice is not one-size-fits-all. It depends on your timeline, your income profile, and how long you plan to continue earning overseas. For a step-by-step action plan once you have decided to return, our RNOR checklist for returning NRIs walks through exactly what to do and when.

Foreign Asset Reporting: How the Obligation Differs Across All Three Statuses

This is the part most comparison articles skip. And it catches returning NRIs off guard more than almost anything else.

As an NRI: You have no requirement to report foreign assets in your Indian ITR. Your overseas bank accounts, property, and investments are your own business as far as Indian tax filing goes.

As RNOR: You are now required to disclose all foreign assets in Schedule FA of your ITR. This includes foreign bank accounts, overseas property, foreign equity and mutual fund holdings, and any other assets held outside India. The Black Money (Undisclosed Foreign Income and Assets) Act applies from this stage.

As ROR: Everything in Schedule FA still applies, plus your foreign income is now part of your taxable income in India. Non-disclosure at this stage carries penalties that can run to Rs. 10 lakh per undisclosed asset per year.

Here is what surprises most people. The Schedule FA reporting obligation starts with RNOR not ROR. Many returning NRIs assume they only need to start reporting foreign assets when they become full residents. That is incorrect. And the penalties for missing it are severe enough that ignorance is not a safe defence.

The good news: if your foreign assets are clean and properly documented, Schedule FA is just a reporting exercise. It does not create tax liability during RNOR. But it must be done.

The Status Transition Strategy: How to Move from NRI to RNOR to ROR With Minimum Tax

Think of this as a three-stage relay race. Each stage has its own job. Drop the baton in any stage and you lose the advantage you built in the previous one.

Stage 1: While You Are Still NRI

This is the preparation stage. Use it well.

Realise capital gains from foreign assets now, while they are outside India's tax net entirely. Maximise your FCNR deposits so you have tax-free interest flowing into the RNOR years. Keep your India day count clean do not creep toward 182 or 120 days. And stop routing foreign income into Indian accounts.

Stage 2: The RNOR Years

This is the active protection stage. Your foreign income is still shielded. Use this time to keep foreign income in overseas accounts or your RFC (Resident Foreign Currency) account not your regular savings account. File your ITR every year as RNOR. Fill Schedule FA accurately. Re-check eligibility every April. And use this window to gradually remit foreign savings to India in a planned, tax-efficient way.

Stage 3: Approaching ROR

Start preparing at least 6 months before you expect to become ROR. Restructure or exit remaining foreign income sources where possible. If foreign income will continue, get your DTAA documentation in order TRC (Tax Residency Certificate), Form 10F, and Form 67 for claiming foreign tax credits. Engage a qualified NRI tax advisor before the transition, not after.

The MostlyNRI team works specifically with returning NRIs on this three-stage transition. If you want to know exactly where you stand in this journey and what to do next, it is worth a conversation before you make any major financial moves.

Frequently Asked Questions

What is the tax status of an NRI after coming back to India?

When an NRI returns to India permanently, they typically become RNOR (Resident but Not Ordinarily Resident) first, not a full resident. This is because their overseas residency history qualifies them for this transitional status under Section 6 of the Income Tax Act. RNOR usually lasts 2 to 3 financial years. After that, if they no longer meet the RNOR conditions, they become ROR and are taxed on global income.

Who is eligible for RNOR status?

You qualify as RNOR if you meet either of two conditions: you were a non-resident in 9 out of the 10 financial years immediately before the current year, OR you were in India for 729 days or fewer across the 7 financial years immediately before the current year. You only need to satisfy one condition. Most NRIs who have spent 8 or more continuous years abroad will qualify comfortably.

Which tax regime saves more tax for a returning NRI?

This depends on income type and amounts. For foreign income specifically, RNOR saves the most because you are physically in India but foreign income is still exempt. The new vs old income tax regime choice within India is a separate decision that depends on deductions you plan to claim. A CA familiar with NRI taxation can run the comparison for your specific income profile.

What is the 90% rule for non-residents?

This is a provision found in certain DTAA treaties, not a standalone Indian tax law rule. In specific treaties, a non-resident can claim treaty benefits if 90% or more of their global income originates from the treaty country. It is relevant in limited situations, typically when a non-resident is close to the residency threshold. If this applies to your situation, verify with an advisor who knows the specific treaty for your country of residence.

Why do many NRIs delay returning to India?

Practically speaking, the tax complexity is a real factor for high-income NRIs. Becoming ROR means global income taxation, which can significantly increase the Indian tax burden. Beyond tax, reasons include ongoing career opportunities abroad, children's education preferences, lifestyle adjustments, and the time needed to plan the financial transition properly. For many, the RNOR window reduces the tax deterrent significantly and makes the return financially viable.

Is NRI better or OCI for tax purposes?

These are completely different things. NRI is a tax status determined by days spent in India. OCI (Overseas Citizen of India) is a citizenship status that gives foreign nationals of Indian origin the right to live and work in India without a visa. OCI has no direct bearing on your Indian tax status. An OCI cardholder who spends more than 182 days in India is still a resident for tax purposes and taxed accordingly.

What income is taxable for RNOR?

During RNOR, only India-sourced income is taxable. This includes Indian salary, rental income from Indian property, capital gains from Indian assets, and interest on NRO accounts. Foreign salary, overseas rental income, capital gains from foreign assets, and interest on NRE and FCNR deposits are not taxable during the RNOR period.

What is the difference between NRI and RNOR?

An NRI is someone who is not resident in India (fewer than 182 days in India in a financial year). An RNOR is someone who is technically resident in India — physically present for more than 182 days — but whose residency history is primarily overseas. Both NRI and RNOR are taxed only on Indian income. The key difference: an NRI does not need to disclose foreign assets in their ITR, while an RNOR must report all foreign assets in Schedule FA.

What is the penalty for not declaring NRI status correctly?

Filing an incorrect residential status in your ITR can attract scrutiny, reassessment, and penalties under the Income Tax Act. If foreign assets are not disclosed when you are already RNOR or ROR, the Black Money Act applies — penalties can reach Rs. 10 lakh per undisclosed asset, with the possibility of prosecution in serious cases. Beyond income tax, misrepresenting residential status for FEMA purposes (for example, maintaining an NRE account after becoming a resident) can attract separate FEMA penalties.

Also read: Tax Residency Certificate (TRC) in India: Meaning, Benefits, Form 10FA & How to Apply Online

Also read: The 2-Year Tax Window

0 Comments