Let’s talk about your money. You’ve built a life in Mexico. The culture, the people, the food. It’s home now. But a part of you still looks towards India. Maybe it’s family. Maybe it’s the memories. And now, you hear about the growth, the opportunities. You think, "Can I be a part of that?"

The answer is a clear yes. Investing in India as an NRI from Mexico is not only possible, it’s a smart way to diversify your future. But the rules are different. The terms are new. Words like FEMA, PIS, and repatriation can feel like a wall.

I remember speaking to an engineer from Guadalajara. He wanted to invest his savings but was terrified of making a legal mistake. He thought the process was only for people living in Delhi or Mumbai. He was wrong.

This guide is your map. We will walk through every step together. From opening the right bank account to picking investments and understanding taxes. We will break down the jargon into simple English. You will learn about mutual funds, stocks, and even new options like GIFT City. By the end, you will have a clear action plan.

Think of it as building a bridge. Your life and earnings are in Mexico. Your investment opportunities are in India. This guide is the architectural plan for that bridge. Let’s start building.

Who Is Considered an NRI Under Indian Rules?

First, let’s get the label right. Are you even an NRI? Under Indian law, it’s not about your passport. It’s about where you live.

You are considered a Non-Resident Indian (NRI) if you live outside India for more than 182 days in a single financial year. That’s it. Your citizenship can be Indian. You could hold an OCI card. But for banking and investment rules, your residency status is the key.

Why does this matter? Because the Indian government has special rules for NRIs. These rules control how you can bring money in, where you can invest it, and how you can take it back out. Using the wrong set of rules is like trying to pay with pesos in a Delhi market. It just won’t work.

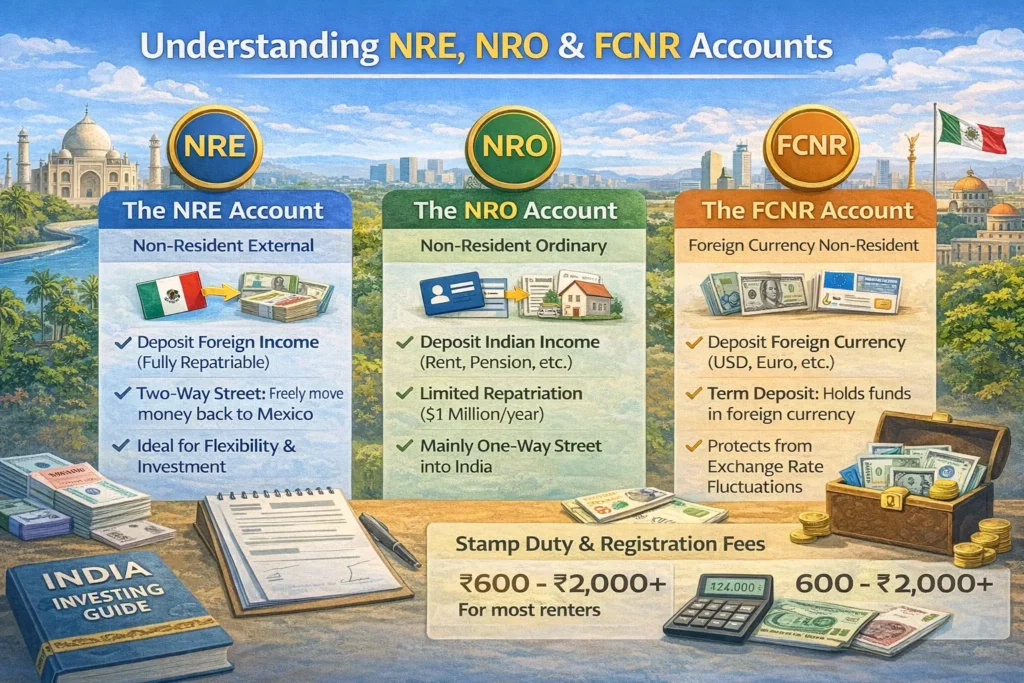

Understanding NRE, NRO & FCNR Accounts

This is the most important part of your foundation. Your Indian bank accounts are the gateway for all your investments. You cannot use your old Indian savings account anymore. You need new ones. There are three main types.

The NRE (Non-Resident External) Account: This is your primary investment account. You open it with money you earned abroad, in Mexico. You transfer your pesos, convert them to rupees, and deposit them. The big benefit? Everything in this account is fully repatriable. This means you can take every single rupee, convert it back to dollars or pesos, and send it back to Mexico anytime. No questions asked. It’s like a two-way street for your money.

The NRO (Non-Resident Ordinary) Account: This account is for money you earn inside India. Did you sell an old family property? Do you get rental income from an apartment? That money goes here. The rules are stricter. You can only repatriate, or send out, up to one million USD per financial year from this account. And you need to show tax documents. Think of it as a mostly one-way street into India, with a small, monitored lane for exiting.

The FCNR (Foreign Currency Non-Resident) Account: This one is different. You don’t convert your foreign currency. You deposit your US dollars or euros directly. The bank holds it in that currency. It’s a term deposit, like a fixed deposit, but in foreign currency. Your capital is protected from rupee exchange rate fluctuations. This is a safe, simple place to park foreign currency savings you might need later.

For most investors starting out, the first step is opening an NRE account. It gives you the most flexibility to invest and bring your profits back to Mexico.

Important Regulatory Rules — FEMA & RBI Overview

Now, let’s talk about the rulebook. All NRI investment is governed by FEMA. That’s the Foreign Exchange Management Act. It’s the big book of rules for cross-border money movement.

The Reserve Bank of India (RBI) is the referee. They enforce FEMA. For you, this means there are specific channels you must use. You can’t just log into any Indian trading app and start buying stocks. You need to use the designated NRI routes.

The most important rule for stock market investors is the Portfolio Investment Scheme (PIS). The RBI says NRIs must use a PIS-approved demat and trading account to buy and sell shares on Indian exchanges. This is not as scary as it sounds. It’s just a special label on your account that lets the RBI monitor your investments. Any major bank or broker in India can set this up for you.

Remember, these rules are not there to stop you. They are there to create a clear, legal path for you to invest. Following them keeps you safe.

Mutual Funds — Easy Diversified Investing

Mutual funds are a fantastic starting point. Think of a mutual fund like a shared investment basket. Thousands of people pool their money. A professional fund manager uses that pool to buy a mix of stocks or bonds. You own a small piece of that entire basket.

As an NRI, you can invest in almost all Indian mutual funds. You use your NRE or NRO account to pay for them. The process is straightforward. You complete a one-time KYC (Know Your Customer) process. Then you can invest online through the fund’s website or a registered advisor.

The best part? Repatriation. If you buy units using your NRE account, you can sell them later and send the full proceeds back to Mexico. If you use an NRO account, the repatriation limits we discussed earlier will apply.

Choose equity funds for long-term growth, debt funds for stability, or hybrid funds for a mix. It’s an easier way to get into the Indian market than picking individual stocks.

Indian Stock Market — Demat + PIS Scheme

If you want to pick your own companies, you can invest directly in the stock market. This is where the PIS account comes in.

Here is the step-by-step.

- Open your NRE/NRO account with an Indian bank.

- Ask that bank, or a broker like ICICI Direct or HDFC Securities, to open a PIS Demat and Trading Account for you.

- Link this trading account to your NRE/NRO bank account.

- Transfer funds from your bank account to your trading account.

- Start buying and selling stocks.

The PIS account acts as a monitoring system. The bank will report all your trades to the RBI. There are limits on how much you can invest in a single company, but for most individual investors, these limits are very high.

You can invest in most listed companies. You can also invest in Exchange Traded Funds (ETFs). The profits you make, if you send them back, must go through the same PIS channel.

Fixed Deposits & Debt Investments

Maybe the stock market feels too unpredictable. That’s okay. You can choose stability.

Indian banks offer Fixed Deposits (FDs) for NRIs. You can open an NRE FD or an NRO FD. The interest rates are often higher than what you might find in Mexico or the US. Your money is locked for a period you choose, from 1 year to 5 years. At the end, you get your initial amount plus the earned interest.

The FCNR Fixed Deposit we mentioned earlier is another great option. You deposit US dollars. You earn interest in US dollars. When the deposit matures, you get your dollars back, plus interest. There is zero currency risk. It’s a safe way to earn a return on foreign currency you plan to use later.

Real Estate — Property & REITs

NRIs have always loved Indian real estate. The rules are friendly. You can buy residential and commercial property. You cannot buy agricultural land, plantation land, or a farmhouse without special permission. But apartments, offices, and plots are open for investment.

You can pay from your NRE, NRO, or FCNR account. You can even take a home loan from an Indian bank. When you sell, you can repatriate the sale proceeds. There is a rule. You can only send back an amount equal to what you originally paid from foreign currency sources. Any profit above that must stay in your NRO account, subject to the annual one-million-dollar repatriation limit.

A newer, simpler option is REITs (Real Estate Investment Trusts). Think of them as mutual funds for real estate. You buy units of a REIT listed on the stock exchange. That REIT owns a portfolio of income-generating offices or malls. You get a share of the rental income as dividends. It’s a way to invest in real estate without the hassle of managing a property from another continent.

GIFT City IFSC Funds & International Access

This is a game changer. GIFT City in Gujarat is India’s special financial zone. It has its own set of international rules. For NRIs, this opens a unique door.

Through GIFT City, you can open an account with a bank or fund manager there. You can then invest in global products. We are talking about US stocks, European bonds, or international mutual funds. All from within India’s regulatory umbrella.

Why is this useful? It consolidates your investments. You can have exposure to India through your NRE account and exposure to the world through your GIFT City account. It’s a powerful tool for a global investment strategy, managed from a single hub.

Other Investment Vehicles

The options go deeper. You can look at Government Securities (G-Secs) for ultra-safe debt. The National Pension System (NPS) is a long-term retirement-focused product with tax benefits. For high-net-worth individuals, Alternative Investment Funds (AIFs) offer access to private equity, hedge funds, and venture capital.

The key is to start simple. Mutual funds and fixed deposits are the most accessible doors. Walk through those first.

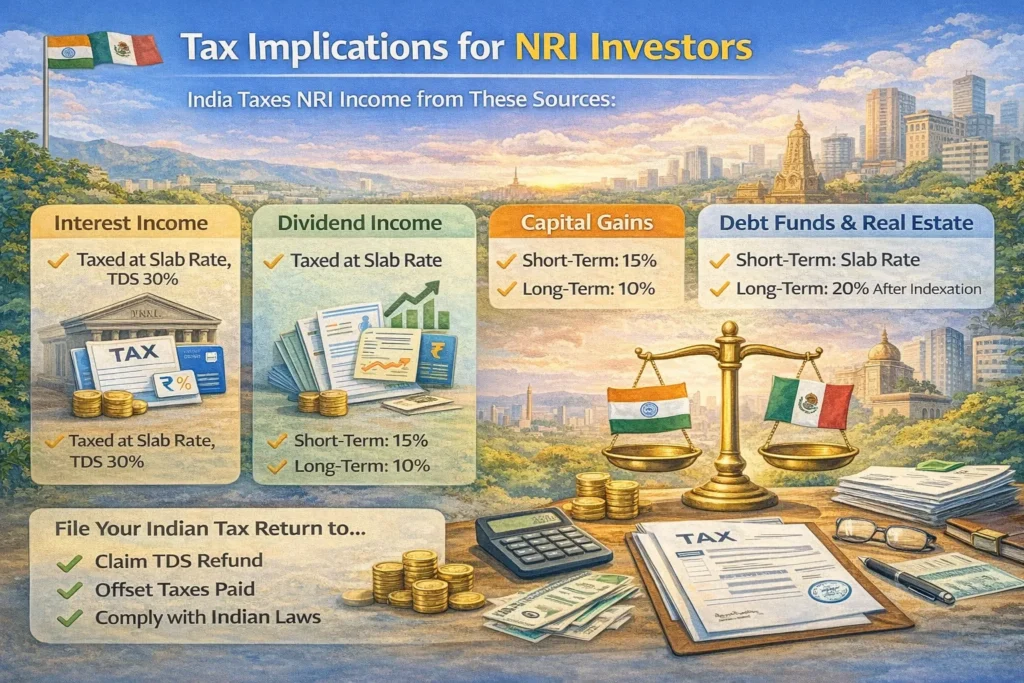

Tax Implications for NRI Investors

India will tax the income you generate from your Indian investments. Mexico may also tax it. You need to understand the Indian side first.

The tax rules are different for different incomes.

- Interest Income: from fixed deposits is taxed at your income tax slab rate. Banks will deduct TDS (Tax Deducted at Source) at 30% plus surcharge. You can file a tax return to claim a refund if your total tax rate is lower.

- Dividend Income: from stocks or mutual funds is also taxed at your slab rate.

- Capital Gains: are profits from selling an investment. The rate changes based on how long you held it.

- Equity Stocks & Equity Mutual Funds: If you sell within one year of buying, it’s Short-Term Capital Gains (STCG). The tax rate is 15%. If you sell after one year, it’s Long-Term Capital Gains (LTCG). Gains over ₹1 lakh in a year are taxed at 10%.

- Debt Mutual Funds & Real Estate: The holding period for long-term is three years. Long-term gains are taxed at 20% after indexation (which adjusts your purchase price for inflation). Short-term gains are added to your income and taxed at your slab rate.

You must file an Indian tax return if your total Indian income exceeds the basic exemption limit. Even if you don’t need to file, you might want to in order to claim a TDS refund.

Repatriation of Funds to Mexico

Repatriation is the final, crucial step. It’s the process of moving your investment proceeds from India back to your bank in Mexico.

The golden rule is simple: Use your NRE account for investments you want to repatriate.

Money in your NRE account, along with the profits made from investing that money, can be sent back freely. You log into your Indian bank’s online portal. You fill out a transfer request to your Mexican bank account. The bank will convert rupees to your chosen currency and send it. It’s that easy.

Money in your NRO account has limits. You can only repatriate up to one million USD per financial year from all your NRO accounts combined. And you must provide documents showing you paid taxes on the funds you want to send.

Plan this from the start. If you think you might want to bring the money back to Mexico one day, fund your investments through your NRE account.

Step-by-Step Process to Invest in India as an NRI from Mexico

Let’s turn this into a clear action plan.

- Open Your NRE/NRO Account: Choose a major Indian bank with good online services for NRIs. Many, like SBI, HDFC, or ICICI, allow you to start the application online from Mexico. You will need to send attested copies of your documents.

- Complete Your KYC: This is a one-time process for most investments. You will need your PAN card, passport, Mexican resident visa, and proof of address in Mexico. Your bank can often help with this.

- Open a PIS Demat Account (For Stocks): If you want to buy stocks, contact your bank’s brokerage arm or a standalone broker to open your PIS-compliant demat and trading account.

- Fund Your Accounts: Use an international wire transfer from your Mexican bank to send money to your new NRE account. Your Indian bank will provide the SWIFT details.

- Start Investing: Log into your mutual fund account or trading platform. Begin with a small, simple investment to get comfortable with the process.

- Maintain Records: Keep clear records of every transfer from Mexico, every investment made, and every sale. This is vital for tax filing and repatriation requests later.

Documents & KYC Requirements

Have these ready:

- PAN Card (Permanent Account Number)

- Passport (copy of pages with photo, address, and visa)

- Mexican Residence Proof (Resident card, visa stamp)

- Proof of Address in Mexico (Utility bill, bank statement)

- Passport-sized Photographs

- Signed Application Forms (provided by the bank or broker)

The process is largely digital now. You can scan and email most documents.

Common Mistakes NRIs in Mexico Make

The biggest pitfall is using the wrong account. Investing money from an NRO account when you plan to repatriate creates a future headache.

Another mistake is ignoring taxes. Not planning for TDS or capital gains tax can lead to a nasty surprise and paperwork later.

A third mistake is rushing into complex investments like real estate without understanding the legal and repatriation nuances.

How to Avoid Investment Pitfalls

Start simple. Begin with mutual funds or fixed deposits through your NRE account. This establishes your pipeline correctly.

Consult a professional. Use a SEBI-registered investment advisor in India who understands NRI regulations. They can help you structure your portfolio the right way from day one.

Diversify. Don’t put all your money in one stock or one property. Use mutual funds to spread your risk automatically.

Conclusion

Investing in India from Mexico is a journey of connection. It connects your present in Mexico with the future potential of India. The path is well-marked with rules like FEMA and tools like NRE accounts. The key is to follow the map.

Begin with the foundation. Open your NRE account. Then take a first, confident step. Maybe it’s a fixed deposit. Maybe it’s a mutual fund SIP. Build your bridge one piece at a time.

Your financial future can have roots in more than one country. With careful planning, you can nurture both. Start today.

FAQs

What is the very first thing I need to do to start investing in India?

The absolute first step is to open an NRE (Non-Resident External) bank account with an Indian bank. This account is your main gateway. It allows you to send money from Mexico to India and, crucially, lets you freely repatriate (send back) your investment profits later.

What's the difference between an NRE and an NRO account?

Think of them as two different wallets for different money. Use your NRE account for money you earn abroad (in Mexico). Everything in it is fully and freely repatriable. Use your NRO account for money you earn inside India (like rent or dividends). Repatriation from an NRO account has an annual limit (currently $1 million) and requires tax documents.

Can I invest in Indian mutual funds from Mexico?

Yes, you can. Once you have an NRE or NRO account and complete a one-time KYC process, you can invest in most Indian mutual funds online. It's one of the easiest ways for NRIs to start investing. Use your NRE account to invest if you want to easily repatriate the money later.

Do I need a special account to buy Indian stocks?

Yes. To buy shares directly on the Indian stock exchange, you must open a PIS (Portfolio Investment Scheme) Demat and Trading Account. This is a special NRI account that your bank or broker will help you set up. It is linked to your NRE/NRO bank account and allows the RBI to monitor your stock investments.

What are the tax rates on my investment profits?

It depends on the investment:

Stocks & Equity Mutual Funds: Profits from sales within 1 year are taxed at 15%. Profits from sales after 1 year are taxed at 10% on gains over ₹1 lakh per year.

Interest from Fixed Deposits: Taxed at your income tax slab rate (often 30% plus surcharge for NRIs).

Debt Mutual Funds & Real Estate: Held less than 3 years, profits are added to your income and taxed. Held more than 3 years, profits are taxed at 20% after indexation (inflation adjustment).

How do I get my investment money back to Mexico?

This process is called repatriation. If your original investment and profits are in your NRE account, you can log in to your Indian bank's online portal and transfer the funds back to your Mexican bank account freely. If the money is in an NRO account, the process has limits and requires more paperwork.

Can I buy property in India as an NRI from Mexico?

Yes. NRIs can freely purchase residential and commercial property in India. You cannot purchase agricultural land, plantation land, or a farmhouse without special permission. You can pay from your NRE, NRO, or FCNR accounts.

What is GIFT City, and why is it relevant for me?

GIFT City in Gujarat is India's international financial zone. It allows NRIs to open accounts and invest in global products like US stocks or international funds from within India's regulatory system. It's a powerful option for diversifying your portfolio beyond Indian assets.

What is the most common mistake NRIs make?

The biggest mistake is using the wrong bank account. Investing money through an NRO account when you intend to repatriate the funds later creates unnecessary complexity and limits. For maximum flexibility, always use your NRE account to fund investments you may want to bring back.

Do I need to file a tax return in India?

You need to file an Indian tax return if your total taxable income in India exceeds the basic exemption limit. Even if it doesn't, you may want to file to claim a refund on any excess Tax Deducted at Source (TDS) from your investment income.

Also Read: How to Invest in India as an NRI from Brazil

Also Read: How To Renew Indian Passport in Finland

Also Read: How To Renew Indian Passport in Denmark

0 Comments