Imagine you are a partner in a small business. The year ends. Your business does not send you a W-2. It does not send you a 1099 either. Instead, a few weeks later, you get a form that says Schedule K-1 at the top. And your first thought is: "What on earth is this?"

You are not alone. K-1 forms confuse thousands of taxpayers every year. They look unusual. They feel complicated. But once you understand the core idea behind them, everything clicks into place.

This guide breaks it all down. Simple language. Step-by-step explanations. Real examples. By the end, you will know exactly what a K-1 is, who gets one, and what to do with it when tax season arrives.

What is a Schedule K-1 Tax Form?

A Schedule K-1 is a tax document. It reports your share of income, losses, deductions, and credits from a business or entity that you are part of.

Think of it like this. You own 30% of a small business. That business made $100,000 in profit this year. You did not receive all of it in cash. But your share is $30,000. The K-1 is the form that tells you, and the IRS, about that $30,000.

The K-1 is not like a W-2 (which reports salary from an employer) or a 1099 (which reports freelance or investment income). It is specifically designed for pass-through entities. These are businesses where income "passes through" directly to the owners, instead of being taxed at the business level.

Key idea: The business does not pay the tax. You do. The K-1 tells you how much income to report on your personal tax return.

What Does “K-1” Mean in Taxes?

The name comes from the IRS form numbering system. The "K" in Schedule K refers to the section of the tax code that deals with partner and shareholder reporting. It has nothing fancy behind it. It is just a label that stuck.

What matters is what it does. The K-1 tells you your specific portion of the entity's financial activity for the year. It is your personal summary of what happened inside a business or trust that you have a stake in.

Types of Schedule K-1 Forms

There are three different K-1 forms, each used for a different type of entity.

| Form Type | Issued By | Received By |

|---|---|---|

| K-1 (Form 1065) | Partnerships and multi-member LLCs | Partners and LLC members |

| K-1 (Form 1120-S) | S Corporations | Shareholders |

| K-1 (Form 1041) | Estates and Trusts | Beneficiaries |

Each form looks slightly different, but they all serve the same purpose: reporting your share of the entity's financials.

How Does a K-1 Tax Form Work?

Let's use a simple analogy. Think of a pizza business owned by three friends: Alex (50% share), Ben (30% share), and Clara (20% share). The business earns $200,000 in profit this year.

The business itself does not pay tax on that $200,000. Instead, the income passes straight through to the owners. Alex reports $100,000 on his personal return. Ben reports $60,000. Clara reports $40,000.

Each of them receives a K-1 from the pizza business. That K-1 tells them exactly how much to report. The IRS gets a copy too, so they know what to expect on each person's return.

This is pass-through taxation in a nutshell. The business is the vehicle. The income flows straight to the owners.

What Information Is Included in a K-1?

A K-1 covers a lot of ground. Here is what you will typically find on one:

- Ordinary business income or loss (your share of day-to-day business profits or losses)

- Rental income (if the entity owns rental properties)

- Interest and dividend income

- Capital gains and losses (short-term and long-term)

- Deductions (such as Section 179 expensing or other business deductions)

- Credits (tax credits passed through to you)

- Your ownership percentage

- Your beginning and ending capital account balance

Each line item on the K-1 gets reported in a specific place on your personal tax return. Some income types are taxed differently. Long-term capital gains, for example, are taxed at lower rates than ordinary income. That distinction matters, and your K-1 will spell it out clearly.

What is a K-1 Tax Document Used For?

The short answer: it is the bridge between the entity's tax return and your personal tax return.

Without it, the IRS would have no way to know what income passed through to you. The entity files its own return (Form 1065, 1120-S, or 1041), reports the total income or loss, and then issues individual K-1s to each partner, shareholder, or beneficiary showing their allocated portion.

You then use that K-1 to complete your own Form 1040.

Who Receives a Schedule K-1?

You will receive a K-1 if you are one of the following:

- A partner in a general or limited partnership

- A member of a multi-member LLC (single-member LLCs generally do not issue K-1s)

- A shareholder in an S corporation

- A beneficiary of an estate or trust (for example, if a family member passed away and you inherited a portion of their estate)

It does not matter if you are an active participant in the business or a silent investor. If you hold an ownership stake, you will get one.

K-1 Tax Form for LLCs, Partnerships and Investments

Many common investment vehicles use the K-1 structure. If you have invested in any of the following, a K-1 is almost certainly in your future:

- Real estate limited partnerships (LPs): Very common for real estate syndications and deals

- Private equity funds: These almost always issue K-1s

- Hedge funds structured as partnerships

- Oil and gas investments

- Investment syndicates and crowdfunded real estate platforms

Even startup founders who structure their company as an LLC or partnership can receive K-1s.

It is also worth noting: publicly traded partnerships (PTPs) issue K-1s too. So if you bought a master limited partnership (MLP) through your brokerage account, you will get a K-1 instead of a 1099. Many first-time MLP investors are caught off guard by this.

K-1 Tax Form Deadlines

Here is where many people run into trouble. K-1 deadlines are different from what most taxpayers are used to. Before a K-1 can be sent to you, the entity has to file its own tax return first. So the timeline looks like this:

| Entity Type | Entity Return Due | Extension Possible Until |

|---|---|---|

| Partnerships (Form 1065) | March 15 | September 15 |

| S Corporations (Form 1120-S) | March 15 | September 15 |

| Estates and Trusts (Form 1041) | April 15 | September 30 |

When Are K-1 Tax Forms Due? (And Why They Are Often Late)

This is probably the most frustrating part of K-1 investing. Your personal tax return is due April 15. But the partnership sending your K-1 may not file its own return until September if they file an extension. That puts you in a tough spot. You cannot complete your return without the K-1.

This is a very common situation, and the IRS is aware of it. Your options are:

- File a tax extension (Form 4868): This gives you until October 15 to file. Note that an extension to file is not an extension to pay. If you expect to owe taxes, you should still pay an estimate by April 15.

- File an amended return (Form 1040-X): If you already filed and your K-1 arrives later, you can amend your return.

- Use an estimate: Some experienced investors use prior-year K-1 data to estimate and file on time, then amend if needed.

Pro tip: If you invest in private partnerships or real estate syndications, plan for this every year. Filing an extension is completely normal and takes just a few minutes.

How Will a K-1 Affect My Taxes?

The honest answer: it depends on what is on the K-1.

If the K-1 shows income, it increases your taxable income. This could push you into a higher tax bracket, increase your overall tax bill, or affect your eligibility for certain deductions and credits.

If the K-1 shows a loss, it may reduce your taxable income. This is one of the reasons real estate partnerships are so popular. Depreciation and other deductions often generate paper losses that investors use to offset other income.

But there is a catch. Passive activity loss rules limit how much loss you can deduct. If you are not an active participant in the business, those losses may be "suspended" and carried forward to future years.

K-1 Income Tax Treatment

Not all K-1 income is taxed the same way. Here is a breakdown:

| Income Type | Where It Goes on Your Return | Tax Rate |

|---|---|---|

| Ordinary business income | Schedule E, Part II | Your regular income tax rate |

| Long-term capital gains | Schedule D | 0%, 15%, or 20% (lower rates) |

| Short-term capital gains | Schedule D | Your regular income tax rate |

| Rental income | Schedule E, Part I | Your regular income tax rate |

| Tax-exempt interest | Informational only | Generally not taxed |

| Self-employment income (active partners) | Schedule SE | Income tax + SE tax (~15.3%) |

One thing to watch: if you are a general partner or active LLC member, your share of ordinary income may be subject to self-employment tax on top of regular income tax. This catches many people off guard the first time.

How to File Taxes with a K-1 (Step-by-Step)

Filing taxes with a K-1 is not as scary as it sounds. Here is the process, broken down simply.

Step 1: Receive your K-1: The entity will mail or electronically deliver it to you. Check your email and physical mail, especially in March and April.

Step 2: Review every line carefully: Check your name, address, Social Security number, and ownership percentage. Errors happen. If something looks wrong, contact the entity immediately.

Step 3: Identify the income types: Look at which boxes are filled in. Box 1 (ordinary income), Box 2 (rental income), Box 9 (capital gains)? Each one flows to a different part of your tax return.

Step 4: Enter the data into your tax software: Most major tax software platforms (TurboTax, H&R Block, TaxAct) have a dedicated K-1 entry section. The software will guide you through each box and place it in the right spot.

Step 5: Review carried-forward items: Some K-1 items, like passive losses that cannot be used yet, carry forward to next year. Your software should track these automatically.

Step 6: File your return: Once everything is entered, review your overall return to make sure the K-1 data looks correct. Then file.

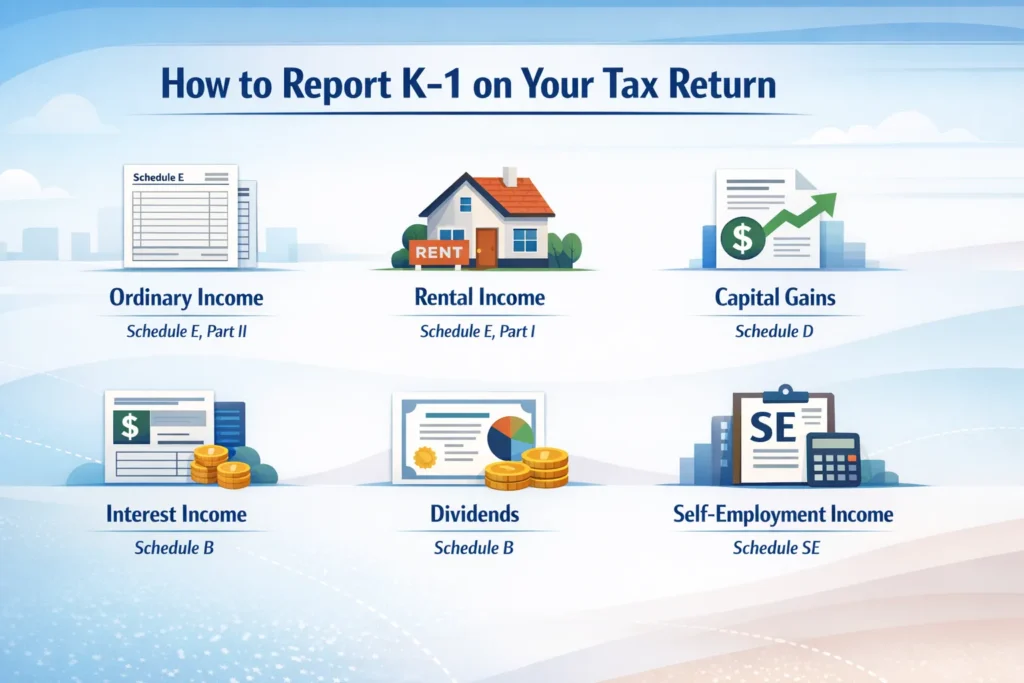

How to Report K-1 on Your Tax Return

Here is where each type of K-1 income ends up on your personal tax return:

- Ordinary income (Box 1): Schedule E, Part II

- Rental income (Box 2): Schedule E, Part I

- Capital gains (Box 8 and 9): Schedule D

- Interest income (Box 5): Schedule B

- Dividends (Box 6): Schedule B

- Self-employment income (active partners): Schedule SE

If you use tax software, it handles all of this automatically once you enter the K-1 data. If you file manually or use a CPA, make sure they have a copy of every K-1 you received.

Can You File Taxes Without a K-1?

Technically, yes. But it is not a good idea.

The IRS already receives a copy of your K-1 directly from the entity. If you do not report the income on your return, the IRS will notice. This typically leads to a notice, an audit, or penalties.

If your K-1 is late, file an extension. It is the cleanest solution by far.

K-1 Tax Form for Inheritance (Trusts and Estates)

Let's say a relative passes away and leaves behind an estate or a trust. You are named as a beneficiary. You may receive distributions from that estate during the year. And you will likely receive a K-1 (Form 1041) to report it.

This K-1 works the same way as any other. It tells you how much of the estate's income, deductions, or credits are allocated to you. You report that on your personal tax return.

One common confusion: the inheritance itself (the principal amount you inherit) is generally not taxable income. The K-1 typically covers income generated by the estate's assets, such as interest earned, dividends, or capital gains from selling estate property.

K-1 for Business Owners

If you are an active partner or managing member of an LLC, your K-1 situation is a bit different from a passive investor.

Your ordinary income from the business is likely subject to self-employment tax, which is approximately 15.3% on net earnings up to a certain threshold, and 2.9% above that. Many business owners are surprised by this when they first encounter it.

It also matters whether you are taking a guaranteed payment (similar to a salary) versus a profit distribution. Both can show up on your K-1, but they are treated differently for tax purposes. Guaranteed payments, for example, are always subject to self-employment tax, regardless of whether the business made a profit.

Filing K-1 for Multiple Investments

If you have invested in several partnerships or funds, you may receive multiple K-1 forms. This is actually quite common among real estate investors and private equity participants.

Managing multiple K-1s can get complex, especially when some entities file extensions and others do not, or when passive losses from one investment can offset passive income from another. You may also have income allocated to multiple states, which can trigger nonresident state tax filing requirements in states where you do not live.

If you are dealing with five or more K-1s across different entities, consider getting professional help. The time saved and errors avoided usually outweigh the cost.

Common Issues with K-1 Tax Forms

Even experienced investors run into K-1 problems. Here are the most common ones.

Late arrival. As discussed, K-1s can arrive in March, April, or even later. The fix: file your own extension (Form 4868) so you are not under pressure.

Errors on the form. Your ownership percentage might be wrong. Your name or Social Security number could have a typo. If you spot an error, contact the general partner, fund administrator, or trustee right away. They will need to issue a corrected K-1. File your return after you receive the corrected version.

Complex reporting. Some K-1s have dozens of line items. This is common with oil and gas investments or complex real estate partnerships. Tax software helps, but these situations often benefit from professional review.

Multi-state income. If the partnership does business in multiple states, you might owe state income taxes in states where you do not even live. The K-1 will usually indicate how much income is allocated to each state. This is one of the less-known complications of K-1 investing.

When to Consult a Tax Professional

There are situations where doing your K-1 taxes yourself is perfectly fine. And there are situations where professional help is clearly worth it.

Consider getting professional help if:

- You have three or more K-1s to report

- Any K-1 shows a large dollar amount (say, over $50,000)

- You have passive losses from previous years that you are trying to use

- The K-1 has complex items related to oil and gas, Section 743(b) adjustments, or foreign income

- You received a K-1 from an estate or trust and are unsure of the tax treatment

- You are a non-resident or international investor dealing with US tax obligations

- You received a notice from the IRS related to a K-1

A qualified CPA or tax attorney who specializes in pass-through entities can save you from costly mistakes. And in many cases, their fee is itself tax-deductible.

Conclusion

Here is the core idea behind every K-1: pass-through taxation. The business does not pay the tax. You do. The K-1 just tells you your share.

Once you understand that concept, the form becomes much less intimidating. Yes, the deadlines can be tricky. Yes, some K-1s are more complex than others. But the underlying logic is always the same.

A few things to remember before you go:

- File an extension if your K-1 has not arrived by April 15

- Report every K-1 you receive. The IRS already has a copy

- Different income types on your K-1 are taxed differently, so review each box carefully

- If you are dealing with multiple K-1s, complex structures, or large amounts, get professional help

The K-1 is not your enemy. For many investors, it is actually a sign that their money is working in tax-efficient structures. Real estate depreciation, business losses, and capital gains treatment can all work in your favour. Understanding your K-1 is not just about avoiding mistakes. It is about making smarter decisions with your money and your taxes.

FREQUENTLY ASKED QUESTIONS

What is a K-1 tax form used for?

It reports your share of income, losses, deductions, and credits from a pass-through entity such as a partnership, LLC, S corporation, or trust. You use it to complete your personal tax return.

How do I get a K-1 tax form?

You do not request it. The entity you are invested in prepares and sends it to you after they file their own return. If you have not received it by mid-April and the entity has not filed an extension, contact them directly.

When are K-1 tax forms due?

Partnership and S corporation K-1s are tied to the entity's March 15 return deadline (with a possible extension to September 15). Trust and estate K-1s follow the April 15 deadline (with extension to September 30). In practice, many arrive late when the entity files an extension.

Can I file taxes without a K-1?

It is not advisable. The IRS already has a copy. If you do not report the income, you risk a notice or penalties. Filing your own extension (Form 4868) is the smart move if your K-1 has not arrived yet.

Is K-1 income taxable?

Yes, in most cases. Ordinary income and rental income are taxed at your regular income tax rates. Long-term capital gains benefit from lower rates. Some items, like tax-exempt interest, are not taxable. The K-1 itself will indicate how each item should be treated.

What is the difference between a K-1 and a 1099?

A 1099 reports income paid directly to you, such as freelance payments or dividends from public stocks. A K-1 reports your allocated share of income from an entity you own a piece of. With a 1099, you received the money. With a K-1, you may or may not have received cash, but you are still responsible for reporting your allocated share.

Do I need a CPA for K-1 filing?

Not always. If you have one simple K-1 with a few line items, tax software can handle it. But if your K-1 is complex, involves large amounts, or you have multiple K-1s across different entities, a CPA is worth the investment.

What happens if I ignore a K-1?

The IRS receives a copy directly from the entity. If you do not report the income, the IRS will notice the discrepancy. This typically leads to a CP2000 notice, where the IRS proposes additional tax, interest, and possibly penalties. It is not worth the risk. Report every K-1 you receive.

0 Comments