You bought a property. The deal went through. You paid the full amount. You moved in. And then... a notice arrives from the Income Tax Department.

Your heart drops. You have no idea what you did wrong. You start Googling frantically.

Here's the thing. You probably missed one small but mandatory step. Deducting 1% TDS before paying the seller.

This happens more than you'd think. Every day, property buyers across India receive notices under Section 194-IA for exactly this reason. The Income Tax Department has been actively tracking these defaults. And if you've received one, you need to act fast.

Don't panic. This guide walks you through exactly what happened, what it costs you, and what to do right now.

What is TDS on Property Purchase? (Section 194-IA)

Think of TDS like a tax checkpoint. Before the buyer hands over the full payment to the seller, the government says: "Hold on. Keep 1% of that amount with you, and deposit it with us."

This is Section 194-IA. It applies when you buy any immovable property (land or building) worth more than Rs 50 lakh.

So if you bought a flat for Rs 80 lakh, you were supposed to:

- Deduct Rs 80,000 (1% of Rs 80 lakh) from the seller's payment

- Deposit that Rs 80,000 to the government using Form 26QB

- Give the seller a Form 16B TDS certificate

Simple enough, right? But most first-time buyers don't know this rule exists. And that's exactly why these notices happen.

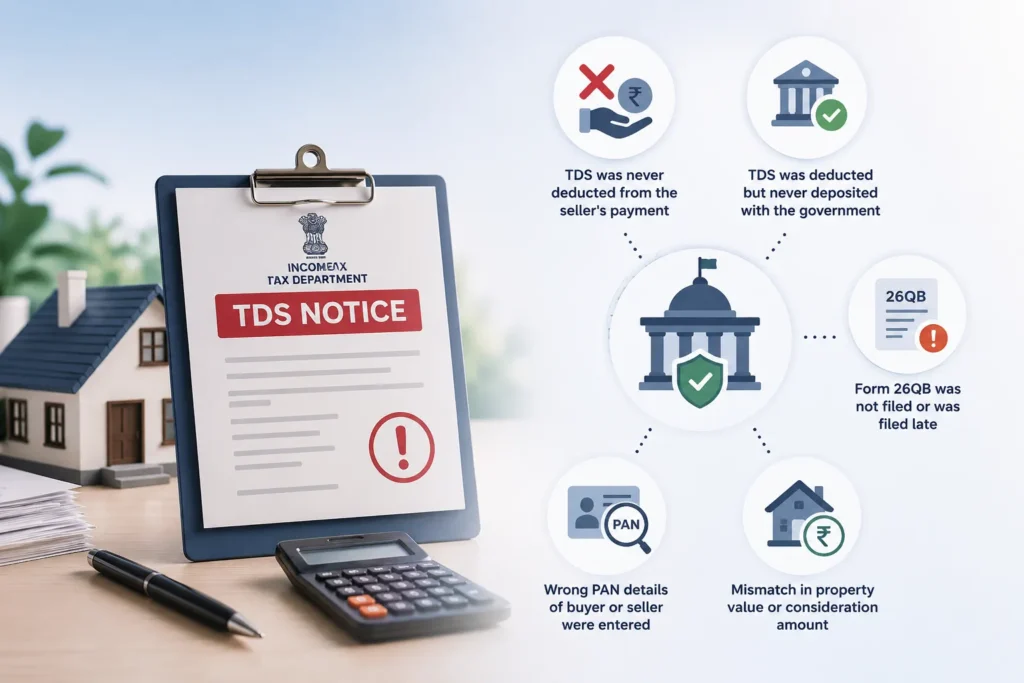

Why Did You Receive This TDS Notice?

There are a few common reasons the Income Tax Department sends these notices:

- TDS was never deducted from the seller's payment

- TDS was deducted but never deposited with the government

- Form 26QB was not filed or was filed late

- Wrong PAN details of buyer or seller were entered

- Mismatch in property value or consideration amount

The department cross-checks property registrations with tax records. When they spot a gap, the notice goes out. It's increasingly automated now, which is why so many buyers are receiving these.

Can a Buyer Be Treated as “Assessee in Default”?

Yes. Absolutely. This is the most important thing to understand.

Under Section 201 of the Income Tax Act, if you fail to deduct TDS or fail to deposit it after deducting, you become an "assessee in default." This status triggers:

- Interest charges

- Late filing fees

- Penalty in serious cases

- Legal notices and possible proceedings

It doesn't matter if the seller is a great person who paid all their taxes correctly. Your obligation as a buyer is independent. The law puts the responsibility squarely on you.

Consequences of Not Deducting TDS on Property

Let's be honest about what ignoring this can cost you.

This isn't just about paying the TDS amount you missed. There's a cascade of financial consequences that pile up over time.

- Interest on the TDS amount (per month)

- Late fee of Rs 200 per day for not filing Form 26QB

- Penalty up to Rs 1,00,000 in extreme cases

- Legal notice and possible assessment proceedings

- Your property registration could be flagged in government systems

The longer you wait, the more it costs. Acting within days of receiving the notice is always better than waiting.

Penalty and Interest for Non-Deduction of TDS

Interest under Section 201

This is the big one. Interest is calculated per month, and it compounds quickly.

| Situation | Interest Rate |

|---|---|

| TDS not deducted at all | 1% per month from the date tax was deductible |

| TDS deducted but not deposited | 1.5% per month from date of deduction to actual deposit |

Note: Even a partial month counts as a full month. So a delay of 1 day into the next month means you pay for the entire month.

Late Fee under Section 234E

This one is separate from interest. If you delay filing Form 26QB, you owe Rs 200 per day as a late fee.

But here's the cap: the late fee cannot exceed the TDS amount itself. So if your TDS was Rs 50,000, the maximum late fee is also Rs 50,000.

Still, Rs 200/day adds up fast. 90 days of delay = Rs 18,000 in late fees alone.

Penalty under Section 271H

In more serious cases, the Assessing Officer can impose a penalty ranging from Rs 10,000 to Rs 1,00,000. This doesn't happen in every case. But if you've received repeated notices, or if the amounts are large, this becomes a real risk.

Step-by-Step: What to Do If You Didn’t Deduct TDS

Okay. Deep breath. Here's your action plan.

Step 1: Read the notice carefully

Check what section it's issued under. What is the exact demand? Which property does it relate to? What period are they asking about? Note every number they mention.

Step 2: Calculate the pending TDS amount

If the property cost Rs 70 lakh, your TDS obligation was Rs 70,000 (1% of Rs 70 lakh). If the consideration was split across instalments, TDS was due on each instalment.

Step 3: Calculate interest and late fees

Use the formula in Part 4 of this guide. This tells you the total amount you owe today.

Step 4: Pay TDS using Form 26QB

Go to the TIN-NSDL portal. Fill in the form. Make the payment. Save the acknowledgment number. This is your proof of compliance.

Step 5: File the TDS return

Form 26QB itself is both the TDS return and the payment challan. Once submitted and paid, the filing is done.

Step 6: Download Form 16B

After 5 working days, log into TRACES and download Form 16B. Give a copy to the seller. Keep one for yourself.

Step 7: Respond to the notice

Login to the Income Tax portal, go to your pending notices, and submit a response with proof of payment.

Step-by-Step Process to Pay Pending TDS Using Form 26QB

Here's exactly how to pay on the TIN-NSDL portal:

- Visit tin.tin.nsdl.com and click on TDS on Property

- Select Form 26QB from the menu

- Enter your PAN and the seller's PAN carefully. A wrong PAN is one of the most common mistakes.

- Enter the property address, total consideration (the full price you agreed to pay), and date of agreement

- Enter the TDS amount, interest, and late fee as applicable

- Choose your payment method: net banking or challan

- Submit and save the acknowledgment number and challan immediately

How to Calculate Interest for TDS Default

Let's take a real example so you can calculate your own liability.

Imagine you bought a property for Rs 60 lakh in January 2024. You paid the seller in full but didn't deduct TDS. It's now July 2024. That's a 6-month delay.

| Item | Amount |

|---|---|

| Property value | Rs 60,00,000 |

| TDS @ 1% | Rs 60,000 |

| Interest @ 1% per month (6 months) | Rs 3,600 |

| Late fee @ Rs 200/day (180 days, capped at TDS amount) | Rs 36,000 |

| Approximate total liability | Rs 99,600 |

So a Rs 60,000 TDS obligation became nearly Rs 1 lakh in total liability. That's why early action matters.

Late Fee Calculation Example

The late fee under Section 234E is Rs 200 per day from the due date (30 days from the date of payment/registration) until the date of actual filing.

Formula: Late Fee = Rs 200 x Number of days delayed (subject to maximum of TDS amount)

A 60-day delay = Rs 12,000 late fee. A 250-day delay on a Rs 20,000 TDS = Rs 20,000 (capped).

What If the Seller Has Already Paid Their Full Tax?

This is a very common scenario. A buyer thinks: the seller paid all taxes, so why should I be penalised?

Here's the legal reality. Under a 2012 Supreme Court judgment and subsequent CBDT clarifications, if the seller has already included the income in their returns and paid tax on it, the buyer may avoid being treated as assessee in default for the principal TDS amount.

But, and this is a big but, the interest under Section 201(1A) still applies to the buyer. You can't escape that just because the seller was compliant.

To claim this protection, you'll need a certificate or declaration from the seller confirming they paid tax on the property sale proceeds.

Time Limit for Income Tax Department to Issue Notice

Buyers often wonder: how far back can they go?

Under Section 201, the department can issue a TDS default notice up to 7 years from the end of the financial year in which the payment was made. For properties purchased in FY 2020-21, notices can come as late as March 2028.

So this isn't something you can just hope fades away. The paper trail exists.

What If TDS Was Deducted But Form 26QB Was Never Filed?

Some buyers mentally deducted TDS (they paid a lower amount to the seller) but never actually deposited it or filed Form 26QB. This is still a default.

In this case, file Form 26QB immediately, deposit the TDS with applicable interest, and pay the late fee. Explain in your notice response that the deduction was made but filing was delayed.

Form 26QB Correction Process

Filed Form 26QB but made a mistake? You can request a correction on the TRACES portal. But here's what you should know first.

What can be corrected online:

- PAN of buyer or seller

- Amount of TDS

- Property details (address, type)

- Date of payment

What requires additional steps:

- If PAN is completely wrong and doesn't belong to the actual seller, you may need to contact TRACES support directly.

The correction process:

- Login to TRACES portal (traces.gov.in)

- Go to Statements / Payments > Request for Correction

- Select Form 26QB and enter the acknowledgment number

- Submit the correction request

- After approval (typically 7-10 days), the corrected TDS credit gets updated in Form 26AS and AIS

How to Download Form 16B

Form 16B is the TDS certificate you must give the seller. Without it, the seller can't claim credit for the TDS you deducted.

Steps to download:

- Login to TRACES portal

- Go to Downloads > Form 16B

- Enter the seller's PAN and acknowledgment number of the Form 26QB

- Wait 5 working days after payment before the certificate is available

- Download and share with the seller

How to Respond to an Income Tax Notice for TDS Default

Once you've paid the TDS and filed Form 26QB, you need to formally respond to the notice. Here's how.

- Login to incometax.gov.in with your PAN

- Go to Pending Actions > Compliance Portal or e-Proceedings

- Locate the notice reference number (from the notice you received)

- Submit your response explaining that TDS has now been paid and Form 26QB has been filed

- Attach supporting documents (see below)

Be factual. Be brief. Don't over-explain. Just state the facts: the TDS default occurred, it has now been corrected, and attach proof.

Documents Required to Reply to the Notice

- Form 26QB acknowledgment receipt with payment confirmation

- Bank challan showing TDS payment

- Form 26AS / AIS extract showing TDS credit (available after a few days)

- Sale agreement or registered sale deed as proof of property and consideration value

- PAN copies of buyer and seller if asked

Checklist to Avoid TDS Notice in Future

If you're buying another property, or if someone you know is buying one, here's the non-negotiable checklist.

- Check the property value. If the agreed price is above Rs 50 lakh, TDS is mandatory. No exceptions.

- Deduct 1% TDS. At the time of payment (or each instalment), calculate and hold back 1% of the amount.

- File Form 26QB within 30 days. 30 days from the end of the month in which payment was made.

- Verify PANs first. Cross-check the seller's PAN on the Income Tax portal before entering it.

- Download Form 16B. After 5 working days, generate and give the certificate to the seller.

- Check Form 26AS. Confirm the TDS appears in your Form 26AS after filing.

Common Mistakes Buyers Make

Let's be real. These aren't dumb mistakes. They happen because buyers are focused on the transaction itself, not the tax compliance side.

- Ignoring the TDS rule entirely. "My builder didn't mention it" is the most common explanation. But that doesn't protect you legally.

- Entering the wrong PAN. One wrong digit means the credit never reaches the seller, and you'll need to file a correction.

- Filing Form 26QB late. Even 1 day past the deadline triggers late fee. Set a calendar reminder.

- Not issuing Form 16B. The seller needs this certificate. Without it, they can't claim credit for the tax you deducted.

- Assuming TDS doesn't apply to agricultural land. Correct. Agricultural land is exempt. But urban land, commercial property, and apartments above Rs 50 lakh are all covered.

Conclusion

Getting a notice from the Income Tax Department is stressful. But this particular one, a TDS default under Section 194-IA, is very fixable. Fast.

The steps are straightforward. Calculate what you owe. Pay using Form 26QB. Download Form 16B. Respond to the notice with proof. Done.

The real cost is in waiting. Interest ticks up every month. Late fees keep adding. And a notice that could have been closed in a week can turn into an extended compliance nightmare.

So if you've received this notice, today is the day to act. Not next week. Today.

And if you're planning to buy property next, now you know. The 1% TDS is not optional. It's not the seller's job. It's yours. Get it done right the first time, and you'll never have to worry about one of these notices again.

FAQs

What happens if I don't deduct TDS?

You become an assessee in default. This triggers interest at 1% per month, late fees of Rs 200/day, and potential penalty up to Rs 1 lakh. The Income Tax Department can also initiate recovery proceedings.

Can I pay TDS after receiving a notice?

Yes. In fact, that's exactly what you should do first. Paying and filing Form 26QB is the most important step before responding to the notice. It shows voluntary compliance.

How do I calculate the penalty and interest I owe?

Interest = TDS amount x 1% x number of months delayed (if not deducted). Late fee = Rs 200 per day (capped at TDS amount). Refer to Part 4 of this guide for a full worked example.

Is TDS required if the property value is below Rs 50 lakh?

No. Section 194-IA applies only when the total consideration is Rs 50 lakh or more. Below that threshold, no TDS deduction is required.

Can the penalty be waived?

Penalty under Section 271H can potentially be avoided if TDS is deposited with full interest and the default was not deliberate. However, interest under 201(1A) and late fee under 234E cannot be waived.

What if the seller refuses to cooperate on TDS?

The buyer's obligation exists regardless of the seller's stance. You must deduct TDS from the seller's payment. If the seller insists on full payment, the law still holds you responsible. You can negotiate so the seller absorbs the TDS from their net proceeds.

How long does a Form 26QB correction take?

Typically 7 to 15 working days for the TRACES team to approve and process. Complex corrections may take longer. Follow up through the TRACES grievance portal if it's been more than 3 weeks.

Do NRIs buying property have different TDS rules?

Yes. If you are buying property from an NRI seller, Section 195 applies, not 194-IA. The TDS rate in that case depends on the seller's capital gains and can range from 20% to 30%. A CA or tax advisor should be consulted for NRI seller transactions.

Also read: NRI Seller Got a Tax Notice for Property Sale? Here's How to Respond and Resolve It

Also read: How to File US Taxes as an NRI

0 Comments