You sold your property in India. The money came through. You thought the hard part was over.

And then a letter arrives. Or an email. From the Income Tax Department of India.

Your stomach sinks. You're sitting thousands of kilometres away in the US, UK, Canada, or Dubai. And suddenly you're staring at a legal notice about a property you sold months ago.

This happens to NRIs constantly. Not because they did something deliberately wrong. But because property sale taxation for NRIs is genuinely complex. One wrong number, one missed form, one buyer who didn't follow the rules properly, and the notice is on its way.

Here's the good news. Most of these notices are resolvable. You don't need to panic. You need a plan.

This guide gives you exactly that.

Why Did You Receive a Tax Notice After Selling Property?

Think of the Income Tax Department as a system that constantly cross-checks numbers. Your buyer reports certain figures. Your Form 26AS shows certain credits. Your ITR (if you filed one) shows certain income. When these don't match up, the system flags it. And a notice goes out automatically.

Here are the most common reasons NRIs receive notices after a property sale:

- TDS mismatch. The buyer deducted a different amount than what you reported, or the TDS isn't reflecting in your Form 26AS at all.

- Incorrect capital gains reporting. The sale value or cost of acquisition was calculated incorrectly in your ITR.

- Missing ITR filing. You received income from an Indian property sale but never filed a return. The department noticed.

- Buyer errors. The buyer filed the wrong form, used the wrong section code, or entered your PAN incorrectly.

- High-value transaction flagged. Property sales above certain thresholds get automatically flagged for scrutiny.

The important thing to understand: receiving a notice does not mean you've committed a crime. It means the department wants clarification or correction. That's all.

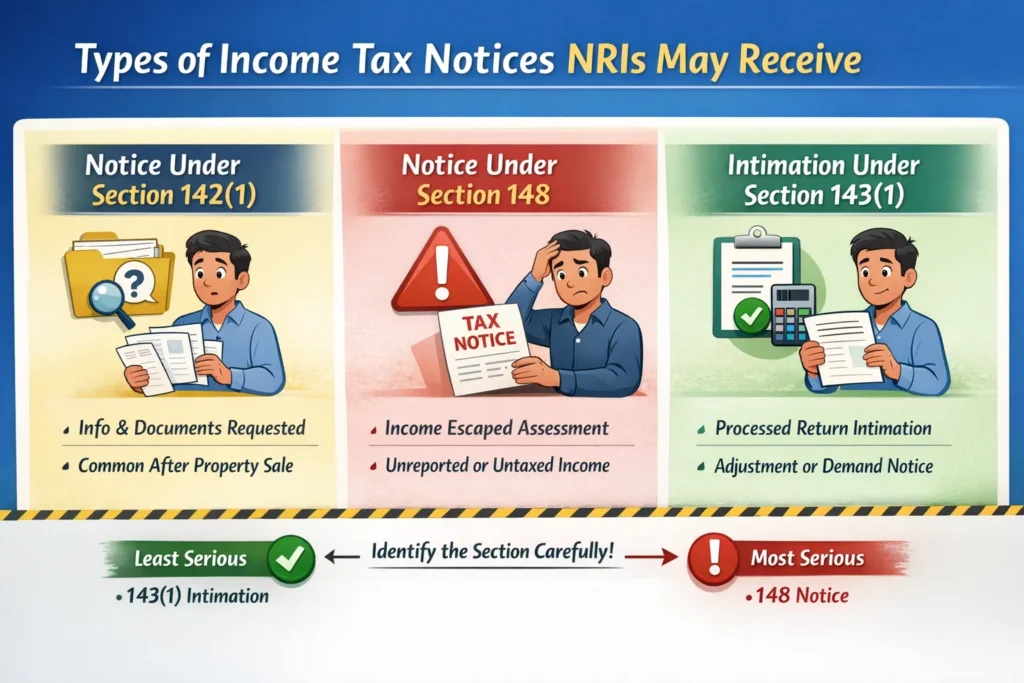

Types of Income Tax Notices NRIs May Receive

Not all notices are the same. The type of notice tells you exactly what the department is asking for.

Notice under Section 142(1)

This is a request for information or documents. The department wants you to explain something or submit specific records. It's essentially saying, "We have questions. Please answer them." This is the most common type NRIs receive after a property sale.

Notice under Section 148

This one is more serious. It means the department believes income has escaped assessment. In other words, they think you earned money that was never taxed. This is usually triggered when ITR was not filed or capital gains were significantly under-reported.

Intimation under Section 143(1)

This is a processed return intimation. It's not always bad news. Sometimes it just confirms your return was processed. But it can also show a demand if there's a discrepancy between what you filed and what the department calculated.

Know this: A 143(1) intimation is the least serious. A 148 notice demands the most urgent attention. Always identify which section your notice is under before doing anything else.

TDS on Sale of Property by NRI (Section 195 Explained)

Here's where most of the confusion starts. And it's important to get this right.

When a resident Indian sells property, the buyer deducts 1% TDS under Section 194-IA. Simple.

But when an NRI sells property, the rules are completely different. The buyer must deduct TDS under Section 195. And the rates are much higher.

| Type of Capital Gain | TDS Rate | Surcharge + Cess |

|---|---|---|

| Long-Term Capital Gain (held 2+ years) | 20% | Applicable |

| Short-Term Capital Gain (held under 2 years) | 30% | Applicable |

So on a property sold for Rs 1 crore, if it's a long-term gain, the buyer should deduct roughly Rs 20-23 lakh as TDS (after surcharge and cess). That's a significant amount sitting with the government until you claim it back.

The buyer is legally responsible for this deduction. But if they get it wrong, the notice can come to you.

Why TDS Issues Lead to Tax Notices

The gap between what should happen and what actually happens is where notices are born.

- Wrong TDS rate used. Many buyers (and even some CAs) mistakenly apply the 1% rate under Section 194-IA instead of the 20-30% rate under Section 195. This creates a massive mismatch.

- TDS not deposited at all. The buyer deducts the amount from payment but never deposits it with the government.

- Form 27Q not filed. For NRI sellers, the buyer must file Form 27Q (not the standard Form 26QB). If they file the wrong form, your TDS credit doesn't show up correctly.

- Form 16A not issued. The buyer must issue Form 16A as the TDS certificate. Without it, you can't claim the credit when filing your ITR.

Each of these errors creates a trail of mismatched data. And when the department's systems detect that mismatch, a notice is generated.

Common TDS Mistakes in NRI Property Sale

Let's talk about the mistakes that actually happen. Because understanding the mistake helps you fix it faster.

Deducting 1% instead of 20%

This is the single most common error. A buyer purchases property from an NRI, follows the standard process they've seen for resident sellers, and deducts 1% TDS. On a Rs 80 lakh property, that's Rs 80,000 instead of the Rs 16 lakh+ that should have been deducted. The shortfall is enormous. And the department will notice.

Wrong PAN entry

If your PAN is entered incorrectly in the TDS filing, the credit doesn't get linked to your account. Your Form 26AS won't show the TDS. And when you file your return, the income appears untaxed. Notice follows.

Wrong section used (194-IA vs 195)

This is a technical error but has major consequences. Filing under the wrong section means the payment goes into the wrong bucket in government records. Corrections are possible but time-consuming.

Partial TDS deduction

Some buyers deduct TDS only on part of the payment. For example, they deduct on the registered value of the property but not on the full market value or actual consideration. If the actual sale consideration is higher, the gap gets flagged.

TDS Mismatch Between Form 26AS and Sale Value

Your Form 26AS is like your tax passport. It records all tax deducted against your PAN. If your property sale was for Rs 90 lakh but Form 26AS only shows TDS on Rs 60 lakh, the department sees a Rs 30 lakh gap. That's income that appears unaccounted for.

Similarly, the Annual Information Statement (AIS) now captures property sale transactions reported by the registrar. If the AIS shows Rs 90 lakh and your ITR shows Rs 60 lakh, that discrepancy will trigger a notice.

Always check your AIS and Form 26AS before filing your ITR. These are the same numbers the department uses.

Step-by-Step: How NRI Sellers Should Respond

Okay. You have the notice in hand. Or in your inbox. Here's what to do, in order.

Step 1: Read the notice carefully and completely

Don't just skim it. Identify the section number (142(1), 143(1), 148). Note the assessment year it refers to. Note the deadline for response. Write down the exact demand or question being raised.

Step 2: Identify the core issue

Is it a TDS mismatch? Missing ITR? Capital gains discrepancy? Buyer error? Each problem has a different fix. Identifying the right issue first saves you from sending the wrong response.

Step 3: Check your Form 26AS and AIS

Login to incometax.gov.in with your PAN. Download your Form 26AS and AIS for the relevant assessment year. Compare the TDS credits shown against what you know was deducted. Look for missing credits or wrong amounts.

Step 4: Collect your documents

Pull together everything related to the property sale. You'll need these to build your response. A full list is in the next section.

Step 5: Calculate the correct tax liability

Work out your capital gains accurately. Use the actual sale price, deduct the indexed cost of acquisition, factor in improvement costs, and apply the correct exemptions if any (like Section 54 or 54EC).

Step 6: Respond online through the income tax portal

Never ignore the notice. Always respond formally through the e-proceedings section of the portal. Attach your documents. Submit before the deadline.

The golden rule: Respond before the deadline. An unanswered notice escalates automatically. And what starts as a simple clarification request can turn into an ex-parte assessment, which is a judgment made without your input, almost always unfavourable.

Documents Required to Respond to the Notice

Have these ready before you start drafting your response:

- Registered sale deed with full property details and consideration amount

- Original purchase agreement and cost documents

- TDS certificates (Form 16A) issued by the buyer

- Form 26AS for the relevant financial year

- AIS (Annual Information Statement) for the relevant year

- Capital gains computation prepared by a CA

- Bank statements showing receipt of sale proceeds

- Form 27Q filing confirmation from the buyer (if available)

- Lower TDS certificate (Form 13) if one was obtained before the sale

- Passport and NRI status documents if residency status is being questioned

The more organised your documentation, the faster the notice gets resolved.

What If the Buyer Deducted the Wrong TDS?

This is frustrating because it's not your mistake. But you still need to fix it.

First, contact the buyer (or their CA) immediately. Explain the error. The buyer needs to file a revised Form 27Q with the correct TDS amount, correct section code, and correct PAN details.

If the buyer deducted only 1% instead of 20-30%, there's a shortfall. The department may demand the balance from you directly, even though the buyer was responsible for the deduction. This is one of those situations where getting a CA involved quickly makes a real difference.

Once the buyer files the correction, wait for the updated TDS to reflect in your Form 26AS (usually takes 7-10 working days after the revised filing is processed).

What If TDS Is Not Reflecting in Form 26AS?

The credit is invisible. You know TDS was deducted. But Form 26AS shows nothing.

Here's what to do:

- Ask the buyer to share the TDS payment challan and Form 27Q filing acknowledgment

- Verify that the challan shows your correct PAN in the deductee section

- If the PAN is wrong, the buyer must file a TDS correction request through TRACES portal

- If the challan shows the right PAN but credit is still missing, raise a grievance through the income tax portal under e-Nivaran or Grievance section

Think of Form 26AS like a bank passbook. If a transfer was made but doesn't show up, you trace the transaction. Same principle here.

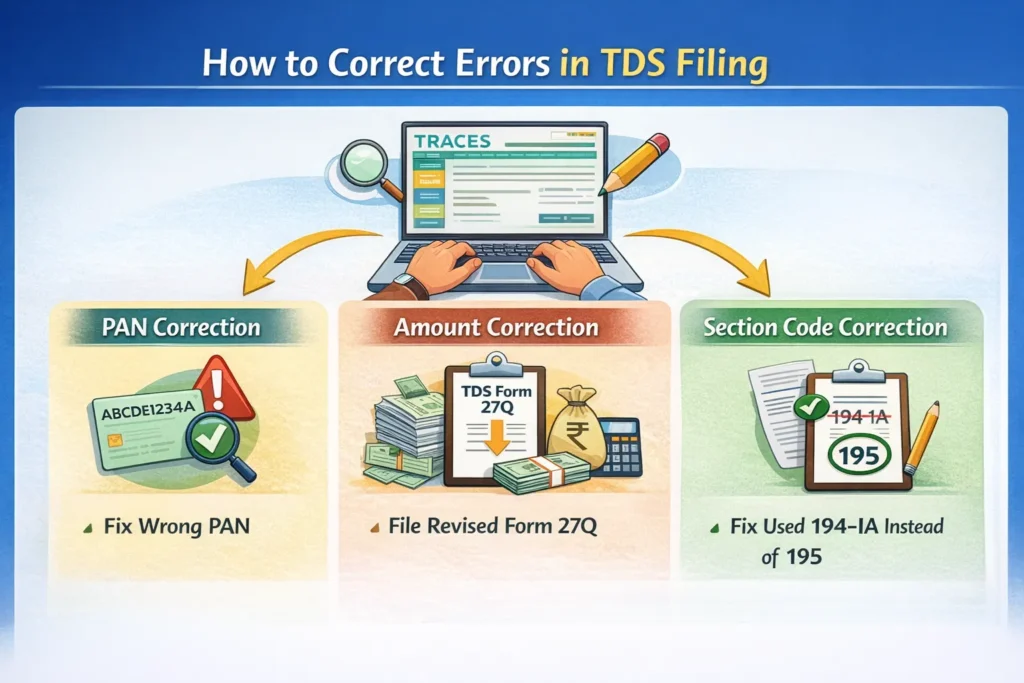

How to Correct Errors in TDS Filing

The buyer files corrections through the TRACES portal. As the seller, you need to coordinate this process. Here's what can be corrected:

- PAN correction: If your PAN was entered wrong, this must be corrected first. Nothing else works until the PAN is right.

- Amount correction: If the TDS amount is wrong (too high or too low), a revised Form 27Q must be filed.

- Section code correction: If 194-IA was used instead of 195, this needs to be corrected to ensure the credit is categorised correctly.

Corrections typically take 7 to 21 days to reflect, depending on the nature of the error and how quickly TRACES processes the request.

How to Calculate Capital Gains for NRI Property Sale

Let's walk through a real example. You bought a flat in Pune in 2010 for Rs 30 lakh. You sold it in 2024 for Rs 90 lakh. Since you held it for more than 2 years, it's a Long-Term Capital Gain (LTCG).

| Item | Amount |

|---|---|

| Sale consideration | Rs 90,00,000 |

| Indexed cost of acquisition (approx.) | Rs 72,00,000 |

| Long-Term Capital Gain | Rs 18,00,000 |

| Tax @ 20% (post-indexation) | Rs 3,60,000 |

The Cost Inflation Index (CII) is used to adjust the purchase price for inflation. This significantly reduces your taxable gain. Your CA will calculate the exact indexed cost using the CII values published by the government each year.

If the property was held for less than 2 years, it becomes a Short-Term Capital Gain, taxed at your applicable slab rate (typically 30% for NRIs at the highest bracket).

Exemptions worth knowing: Section 54 allows you to reinvest LTCG into another residential property in India and avoid tax on those gains. Section 54EC allows you to invest in specific government bonds (NHAI, REC) within 6 months to save tax.

What If Excess TDS Was Deducted?

This is more common than you'd think. The buyer deducts 20-30% TDS on the full sale value. But your actual capital gain, and therefore your actual tax liability, is much lower. Sometimes the TDS deducted is more than your entire tax bill.

The fix is straightforward: file your Indian ITR for the relevant assessment year. Show the correct capital gains computation. The excess TDS you've already paid shows up as a credit in your Form 26AS. The difference becomes a refund.

Refunds for NRIs are credited directly to the Indian bank account linked to your PAN. You can also request direct transfer to an NRO account. The refund process typically takes 3 to 6 months after filing.

Key insight: Many NRIs skip filing the ITR because they think they're not required to. But if TDS was deducted, filing the ITR is literally the only way to get that money back. It's not optional if you want your refund.

How Form 13 Helps NRIs Reduce TDS

Here's something most NRIs only learn after they've already sold a property. There's a way to legally reduce the TDS burden before the sale happens.

Form 13 is an application to the Income Tax Department requesting a certificate for lower (or nil) TDS deduction. You apply before the sale closes. The department reviews your capital gains calculation, verifies your actual tax liability, and issues a certificate saying the buyer only needs to deduct TDS at a lower rate.

Instead of losing 20% of your sale proceeds upfront, you might only have TDS deducted at 5% or 8%. This is a massive cash flow benefit for large transactions.

The application process takes about 4 to 8 weeks. So if you're planning a property sale, apply for Form 13 early, well before the registration date.

Think of it as telling the government: "I know my actual tax is only X. Can you authorise a lower deduction?" If your documents support it, they usually say yes.

To apply for Form 13, login to the income tax portal and go to the e-Services > Lower / Nil TDS section. You'll need to submit your capital gains workings, cost documents, and sale agreement details.

How to Reply to an Income Tax Notice Online

The entire process is now online. You don't need to visit any office. Here's how to submit your response.

- Login to incometax.gov.in using your PAN and password

- Go to Pending Actions > e-Proceedings

- Find the notice using its Document Identification Number (DIN), which is printed on the notice itself

- Click Submit Response

- Write a clear, factual response addressing the specific issue raised

- Upload all supporting documents (PDFs, under 5MB each typically)

- Submit and save the acknowledgment

Write your response in simple, direct language. State what happened, what the correct position is, and what documents you're attaching as proof. Don't write essays. Don't get emotional. Stick to facts.

What Happens If You Ignore the Notice?

This is where things spiral. And they spiral fast.

- First, the department sends reminders

- Then, if there's still no response, an ex-parte assessment is completed. This means they decide your tax liability without your input, almost always assuming the worst case

- Then, a demand notice is issued for the amount they've calculated (which is usually much higher than your actual liability)

- Then, interest under Section 220 starts accumulating on the unpaid demand

- Then, penalty proceedings under Section 270A or 271 may begin

- Finally, if the amount is large enough, prosecution under Section 276C becomes possible

None of this is inevitable if you respond properly. But every step becomes available to the department the moment you go silent.

An ignored notice is like an unattended fire. Small at first. Very manageable. But leave it alone and it will consume everything.

How NRIs Can Avoid Tax Notices in Future

Once you've dealt with this notice, here's how to make sure you never have to go through it again.

Ensure correct TDS deduction from the start. Before the sale, educate your buyer (or their CA) about Section 195 obligations. Put it in writing if necessary. Confirm the TDS amount, section, and filing requirements before the transaction closes.

Apply for Form 13 if TDS will be disproportionately high. This one step protects your cash flow and reduces the risk of a refund delay.

File your Indian ITR every year that you have Indian income. Property sale proceeds, rental income, interest on NRO accounts, all of this creates filing obligations. An unfiled return is one of the easiest ways to attract a notice.

Verify your Form 26AS and AIS every year. These documents are available free on the income tax portal. Check them after every major transaction. Cross-reference with your own records. Catch errors early, before the department does.

Hire a CA with NRI tax experience. Not just any CA. Someone who specifically handles NRI property transactions. This is not the area to cut corners on.

When Should NRIs Hire a CA?

Honestly? For most property transactions above Rs 30-40 lakh, the answer is: always.

But specifically, hire a CA when:

- The property sale involves a significant capital gain and you want to plan for exemptions under Section 54 or 54EC

- You've received a notice under Section 148 (reassessment), which is the most serious type

- There's a TDS mismatch that requires coordination with the buyer's CA and TRACES corrections

- You're not sure whether to file an ITR for the relevant year

- The property was inherited or gifted and the cost of acquisition is complicated to calculate

- You're navigating DTAA (Double Taxation Avoidance Agreement) benefits between India and your country of residence

A good CA's fee for this kind of work is a small fraction of the tax savings or penalty avoidance they can deliver.

Conclusion

Receiving a tax notice is stressful, especially when you're overseas and the Indian tax system feels like a maze from a distance.

But here's the reality. These notices are common. They are, in most cases, administrative. And they are absolutely resolvable with the right approach.

Read the notice carefully. Identify the issue. Fix the TDS problem if there is one. Check your Form 26AS and AIS. Calculate your capital gains correctly. Respond on the portal before the deadline. Attach clean documentation.

Do those things and you'll almost certainly come out fine.

The only mistake that truly hurts is silence. Ignoring the notice doesn't make it disappear. It makes it grow. And what started as a 15-day clarification request becomes a demand notice with interest, penalty, and a lot more paperwork.

So act now. Get a CA if the amount is significant or the notice is complex. And going forward, plan your property transactions properly. Form 13 before the sale, correct TDS at the time of sale, ITR filed on time after the sale.

That's all it takes to stay clean with the Income Tax Department as an NRI property seller in India.

FREQUENTLY ASKED QUESTIONS

Why did I receive a tax notice after selling property in India?

Usually because of a TDS mismatch, missing ITR, capital gains discrepancy, or buyer filing errors. The department's systems automatically flag these. It doesn't mean you've done something criminal.

What is Section 195 TDS for NRI property sale?

Section 195 requires the buyer of property from an NRI to deduct TDS at 20% (for long-term gains) or 30% (for short-term gains), plus applicable surcharge and cess. This is very different from the 1% rule that applies when both buyer and seller are resident Indians.

How do I fix a TDS mismatch?

Ask the buyer to file a corrected Form 27Q through TRACES. Verify the correction reflects in your Form 26AS. If the buyer is uncooperative, raise a grievance through the income tax portal and consult a CA to explore direct correction options.

Can I claim a refund if excess TDS was deducted?

Yes. File your Indian ITR showing the correct capital gains computation. The excess TDS already deducted will appear as a credit. The difference is refunded to your linked Indian bank account.

What if the buyer made a mistake, not me?

You're still responsible for ensuring compliance from your end. The notice comes to you because it's your income. The buyer's error needs to be corrected by the buyer, but you need to follow up and ensure it happens.

Is it mandatory for NRIs to file an ITR after selling property in India?

If your gross Indian income (including capital gains from the sale) exceeds the basic exemption limit, yes. And even if it doesn't, filing is necessary to claim a refund of excess TDS.

How long do I have to respond to an income tax notice?

It varies by notice type. Section 142(1) notices typically give 15-30 days. Section 148 notices give 30 days to respond and file return. Always check the specific deadline printed on the notice and don't miss it.

Can penalties be avoided even after receiving a notice?

Yes, in many cases. If you respond promptly, pay any outstanding tax with interest, and show that the default was unintentional, penalty proceedings can often be dropped or reduced. The key is early, documented, voluntary compliance.

Read More: Received a Notice for Not Deducting TDS on Property Purchase

Also Read: How to Get a Lower TDS Certificate in India: Step-by-Step Process

0 Comments