You get a call from your CA. Or maybe an email from your Indian bank. The message is simple: "Please submit Form 10F before we process your payment."

And your first thought is: what even is Form 10F?

This happens to hundreds of NRIs every year. You're receiving interest on your NRO account, a royalty from an Indian company, or dividends from your Indian portfolio. And your payer refuses to apply the lower tax treaty rate until you submit this form. Without it, TDS gets deducted at 20% or higher. With it, you could be paying half that or less. This guide covers what Form 10F is, who actually needs to file it, what documents to keep ready, and a step-by-step walkthrough of how to file Form 10F online on the Income Tax e-filing portal. By the end, you'll know exactly what to do.

What Is Form 10F and What Is Its Purpose?

Form 10F is a self-declaration form filed by non-resident taxpayers under Rule 21AB of the Income Tax Rules. It provides residency and identity details that are missing from their Tax Residency Certificate, allowing them to claim DTAA benefits and lower TDS rates on income received from India. It is required under Section 90 or Section 90A of the Income Tax Act.

Think of it this way. Your Tax Residency Certificate (TRC) is like your ID card. It proves you live and pay taxes in another country. But some ID cards don't carry all the details Indian tax law requires. Form 10F fills those gaps. It is your supplementary declaration that says: here is the information my TRC didn't include.

Without Form 10F, your Indian payer has no basis to apply the lower DTAA rate. So they default to the higher rate under Indian domestic law. That's the financial hit you're trying to avoid.

Form 10F is filed online on the Income Tax e-filing portal at incometax.gov.in. It is linked to a specific assessment year and must be filed before the payment is made or TDS is deducted.

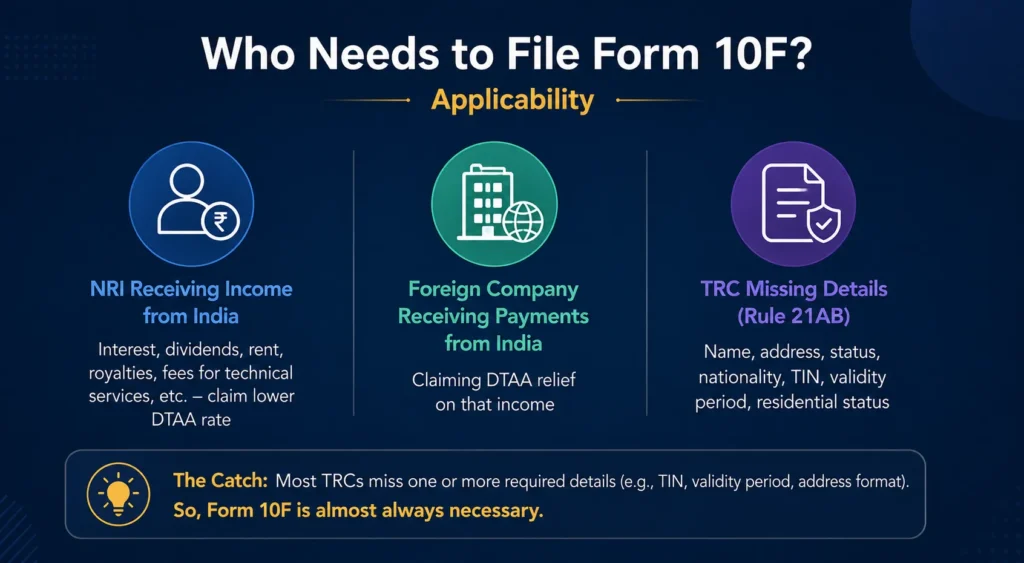

Who Needs to File Form 10F: Applicability

Not every NRI needs to file Form 10F. But most do. Here is the full picture.

You need to file Form 10F if you are:

- An NRI receiving income from India, including interest on NRO accounts, dividends, rent, royalties, or fees for technical services, and you want to claim the lower DTAA rate instead of the default TDS rate

- A foreign company receiving payments from an Indian entity and claiming DTAA relief on that income

- Any non-resident whose TRC does not include all the details required under Rule 21AB: name, address, status, nationality, Tax Identification Number (TIN), period of TRC validity, and residential status

Here's the catch. Technically, if your TRC already contains all the above details, you don't need to file Form 10F separately. But in practice, most TRCs issued by foreign governments are missing one or more of these fields. A UAE TRC, for instance, may not mention your TIN or specify the exact period. A UK certificate may omit your address in the format India requires. So even if you think your TRC is complete, Form 10F is almost always necessary.

If you are an RNOR filing to claim foreign tax credits or documenting your DTAA position, you may also encounter Form 10F as part of your paperwork. The same applies to returning NRIs in transition years. For a deeper look at RNOR status and its tax implications, the MostlyNRI RNOR Checklist covers that ground well.

What Information and Documents Are Required for Form 10F?

Before you sit down to file, get everything in order. This is a ten-minute task if you're prepared. It becomes an hour-long headache if you are not.

Information you will enter directly in Form 10F:

- Name of the taxpayer (as it appears on your passport or TRC)

- Status: individual, company, firm, or other

- Nationality (for individuals) or country of incorporation (for entities)

- Taxpayer Identification Number (TIN) or unique identification number issued by your country of residence

- Period for which the TRC is valid (start and end dates)

- Address of the taxpayer in the country of residence during the TRC validity period

Documents to have ready before you start:

- Tax Residency Certificate (TRC): issued by the tax authority of the country where you reside. This is mandatory. Without it, Form 10F has no legal backing

- PAN (if you hold one): you will use this to log in to the portal. If you do not have a PAN, read the section below on the CBDT relaxation

- Passport and visa details: useful for identity verification during registration

- Bank account details for the Indian income source: sometimes needed for EVC verification

A small but important note: double-check that the TIN you enter in Form 10F matches exactly what appears on your TRC. Even a single digit mismatch can cause a rejection or create issues when the payer verifies the form. Also, ensure the period you mention in the form falls within the TRC's validity dates. These are two of the most common errors, and both are completely avoidable.

For context on how Form 10F connects to your broader tax filing, especially if you are also claiming Foreign Tax Credit under Form 67, check the MostlyNRI Form 67 guide.

Step-by-Step: How to File Form 10F Online on the Income Tax Portal

This is the section you actually came for. Let's walk through it.

Step 1: Go to the Income Tax e-filing portal at incometax.gov.in

Step 2: Log in using your PAN and password. If you are an NRI without a PAN, see the H3 section below on the CBDT relaxation route for non-PAN filers.

Step 3: Once logged in, go to the top menu and click on e-File. From the dropdown, select Income Tax Forms, then click File Income Tax Forms.

Step 4: In the search bar or the list of forms, look for Form 10F. Select it.

Step 5: Choose the relevant Assessment Year. For income received in FY 2025-26, select AY 2026-27.

Step 6: Fill in all the required details in the form:

- Name, status, nationality

- TIN or unique identification number from your country of residence

- Period of TRC validity (exact start and end dates)

- Your address in the foreign country during that period

Step 7: Upload your TRC as a supporting document. The portal will prompt you to attach it. Make sure the file is clear, legible, and in PDF or image format within the size limits specified.

Step 8: Verify the form. You have two options:

- DSC (Digital Signature Certificate): used by NRIs who have a registered DSC on the portal. More common for companies and professionals.

- EVC (Electronic Verification Code): the more common route for individual NRIs. You can generate an EVC via net banking, Aadhaar OTP (if linked), or through your bank account.

Step 9: Submit. The portal will generate a transaction ID and an acknowledgement number. Save both.

Step 10: Download the submitted Form 10F as a PDF. Share this with your Indian payer. They will need it on record before applying the lower DTAA rate on your income.

One important rule: File Form 10F before the payment is made or TDS is deducted. If TDS has already been deducted at the higher rate, Form 10F cannot fix that retroactively at the source. Your only option then is to claim a refund through your ITR, which takes far longer.

Note: The Income Tax portal UI is updated periodically by CBDT. The navigation path above reflects the general structure at the time of writing. Always verify the current steps directly on the live portal before filing.

Filing Form 10F Without PAN: The CBDT Relaxation Explained

This is the question most non-resident filers ask. "I don't have an Indian PAN. Can I still file Form 10F online?"

The answer is yes.

CBDT issued a relaxation specifically for non-resident taxpayers who do not hold a PAN. Under this, NRIs and foreign entities can register on the Income Tax e-filing portal using their foreign tax identification details and file Form 10F through that route.

During registration, you use your passport details, foreign TIN, and country of residence instead of a PAN. Once registered, the filing process follows the same steps outlined above.

This relaxation was introduced because the earlier requirement of a PAN was creating genuine hardship for non-residents who had no other reason to obtain one. If you fall into this category, verify the exact current registration path on the portal or with a qualified NRI tax advisor, as CBDT updates these instructions periodically.

TRC vs Form 10F: What Is the Difference and Do You Need Both?

Short answer: yes, you need both. They are not interchangeable.

Here is a clean breakdown:

| TRC (Tax Residency Certificate) | Form 10F | |

|---|---|---|

| What it is | A certificate proving your tax residency in a foreign country | A self-declaration form providing supplementary details missing from the TRC |

| Who issues it | The foreign country's tax authority (e.g., HMRC in the UK, IRS in the US, FTA in UAE) | Filed by the non-resident taxpayer themselves on the Indian IT portal |

| What it contains | Proof of residence, sometimes TIN, name, and period | Name, status, nationality, TIN, TRC validity period, foreign address |

| Is it enough alone? | No: if it lacks Rule 21AB details, it is incomplete | No: has no legal value without a valid TRC to back it |

Think of the TRC as the foundation and Form 10F as the supporting wall. Neither stands without the other. The Indian payer needs to see both documents before they can apply the treaty rate.

A common error: some NRIs assume that submitting the TRC to their payer is sufficient. It is not. Most Indian payers, including banks and companies, will ask for Form 10F specifically. Do not skip it assuming your TRC covers everything.

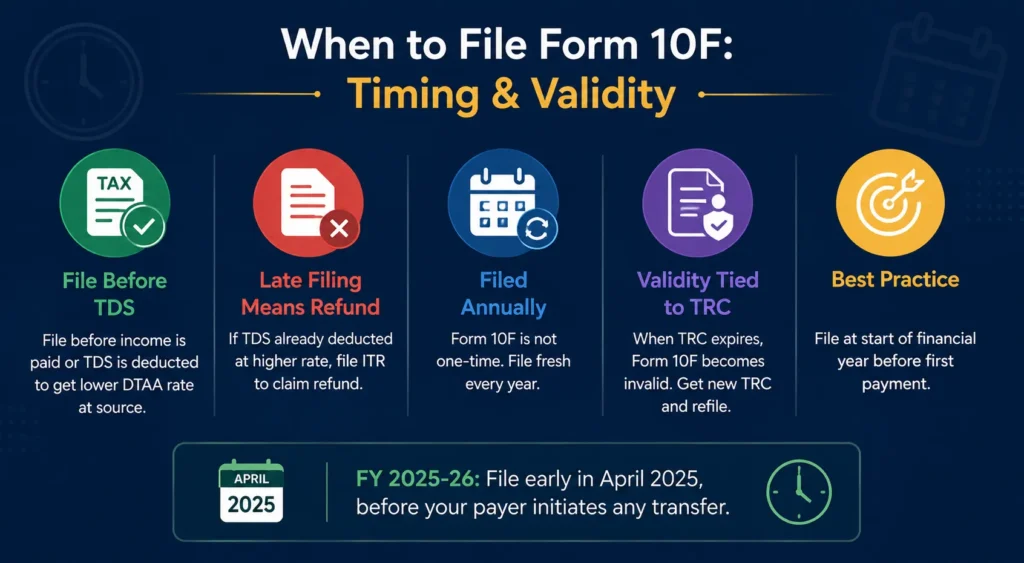

When to File Form 10F: Timing and Validity

Timing matters a lot here. Miss the window and you end up paying excess TDS and chasing a refund for months.

- File before the income is paid or TDS is deducted: That is the only way the lower DTAA rate gets applied at source.

- If TDS has already been deducted at the higher rate and you file Form 10F later, the payer cannot revise what they have already deposited with the government. You would need to file an Indian ITR and claim a refund. That is an avoidable delay.

- Form 10F is filed annually: It is not a one-time permanent declaration. You file it fresh for each assessment year.

- Its validity is tied to your TRC. When your TRC expires, Form 10F based on that TRC also becomes invalid. You need a fresh TRC first, then refile Form 10F.

- Best practice: File at the beginning of each financial year, before the first payment is expected. For FY 2025-26, that means filing early in April 2025, well before your payer initiates any transfer.

What Happens If Form 10F Is Not Filed?

Here is the practical reality.

Your Indian payer must deduct TDS at the default rate if you have not submitted Form 10F. Under Section 195, that rate is typically 20% plus applicable surcharge and cess. The lower DTAA rate, often 10-15% or even lower depending on the treaty, cannot be applied without Form 10F on record.

What can you do if this happens? You can file an Indian Income Tax Return and claim a refund of the excess TDS. It works, but it takes time. The refund process can stretch over months, and it involves paperwork you could have easily avoided.

In some cases, especially with banks and large corporate payers, they may simply refuse to process the payment until Form 10F is submitted. They are protecting themselves from liability. So practically, you may not receive your money at all until the form is in order.

There is no specific penalty for not filing Form 10F. But the financial cost of excess TDS deducted is very real, and the hassle of claiming a refund even more so.

Common Mistakes to Avoid While Filing Form 10F

- Filing for the wrong assessment year: Form 10F must match the financial year in which the income is received. Income in FY 2025-26 means AY 2026-27.

- TRC and Form 10F period mismatch: The TRC validity dates must cover the period for which Form 10F is being filed. If your TRC is valid from January to December but you're filing for an April-to-March financial year, there may be a gap. Check the dates carefully.

- Incorrect TIN: Your Taxpayer Identification Number must match exactly what appears on your TRC. No extra spaces, no abbreviations, no guesswork.

- Filing after TDS has already been deducted: As covered above, this doesn't help at source. File early.

- Not downloading and sharing the acknowledgement: After filing, download the PDF acknowledgement from the portal. Send it to your Indian payer. They need this for their own records before they can apply the treaty rate. Skipping this step means the payer may still deduct at the higher rate even if you've filed.

Conclusion

Form 10F is an important compliance requirement for NRIs and foreign taxpayers who want to claim DTAA benefits on income earned from India. While the form itself is simple, missing it can lead to higher TDS deductions, delayed payments, and the hassle of claiming refunds later through an Indian tax return.

The key is to treat Form 10F and your Tax Residency Certificate as a pair. Your TRC proves your foreign tax residency, while Form 10F provides the additional details Indian tax rules require. Filing both on time ensures that your bank, company, or payer can apply the lower treaty rate correctly.

If you regularly earn income from India, it is best to make Form 10F part of your annual NRI tax checklist. A few minutes spent filing it at the beginning of the financial year can save you unnecessary tax deductions, paperwork, and months of waiting for refunds later.

Frequently Asked Questions

How to download Form 10F online?

After logging in to incometax.gov.in, go to e-File, then Income Tax Forms, and select Form 10F. You can view and download the blank form from there. After filing, the submitted form with the acknowledgement is also available for download under your filed forms history.

Who is required to file Form 10F online?

Any non-resident taxpayer claiming DTAA benefits on income received from India. This includes NRIs receiving NRO interest, dividends, rent, royalties, or fees for technical services, and foreign companies receiving payments from Indian entities under a tax treaty.

What is a 10F document?

It is a self-declaration form under Rule 21AB of the Income Tax Rules. A non-resident files it to provide details not included in their Tax Residency Certificate, specifically to claim the lower TDS rate available under a DTAA.

Is Form 10F to be filed every year?

Yes. It is filed annually for each assessment year. It is linked to the validity of your TRC. When the TRC is renewed, Form 10F must be refiled.

How to fill in Form 10F India?

Log in to incometax.gov.in, navigate to e-File, then Income Tax Forms, then File Income Tax Forms. Select Form 10F, choose the assessment year, and fill in your name, status, nationality, TIN, TRC validity period, and foreign address. Upload your TRC and verify using DSC or EVC. Full steps are covered in the how-to section above.

What if Form 10F is not filed?

The Indian payer will deduct TDS at the default higher rate, typically 20% plus surcharge and cess, instead of the lower DTAA rate. You can later claim a refund by filing an Indian ITR, but this takes time and is avoidable if you file Form 10F before the payment is processed.

What are examples of Form 10F being used?

Three common scenarios: First: An NRI living in the UAE receives interest on their NRO savings account. The bank asks for Form 10F backed by a UAE TRC to apply the 12.5% DTAA rate instead of 30%. Second: A UK-based software company receives royalties from an Indian business partner. The Indian company needs Form 10F and TRC before remitting at the lower 10% treaty rate for royalties. Third: An Indian-origin consultant based in Canada provides technical advisory services to an Indian firm. The firm needs Form 10F to apply the 15% treaty rate on fees for technical services instead of the 20% domestic TDS rate.

How much does a CA charge to file Form 10F or an ITR?

CA fees vary widely depending on the complexity of your income and the professional you engage. For NRI-specific filings, you are likely looking at anywhere between Rs. 2,000 and Rs. 10,000 or more for ITR filing, and a smaller fee for Form 10F assistance. For personalised guidance on DTAA claims and Form 10F compliance, MostlyNRI's NRI tax advisory can help.

What is the difference between Form 10F and Form 10FA?

These are two different forms. Form 10F is a self-declaration filed by a non-resident to support their DTAA claim and provide TRC supplement details. Form 10FA is an application to the Assessing Officer for a certificate under Section 197 for deduction of TDS at a lower rate. They serve different purposes and should not be confused.

0 Comments