Imagine you are visiting family in India. You are at a local market. You see a beautiful gift. You want to pay for it. But you do not have cash. Your international credit card is not accepted. You feel stuck.

This was a common problem for Non-Resident Indians. Not anymore.

The rules have changed. Now, you can pay using your phone. Instantly. Just like everyone in India does. This is the power of UPI for NRIs.

If you have asked, “Can I use UPI with my foreign number?” the answer is a clear yes. This guide will walk you through everything. We will cover the new rules, the setup process, and what you can and cannot do. Let us get you started.

What is UPI? A Quick Refresher

UPI stands for Unified Payments Interface. Think of it as India’s digital payment highway. It lets people send money between bank accounts instantly. All with a few taps on a phone.

You do not need to remember long bank account numbers or IFSC codes. You just need a UPI ID. This is a simple address, like yourname@axisbank.

You can also scan QR codes at shops to pay. It is that simple. The system is run by the National Payments Corporation of India (NPCI). It works 24/7. It connects almost every bank in the country.

I remember my first UPI payment. I was buying street food. I scanned a code. The payment went through in seconds. The vendor gave me a nod and a smile. It was seamless. Now, that ease is available to you, even from abroad.

Can NRIs Use UPI? Yes — Here’s How the Rules Changed

For a long time, UPI was only for people with Indian mobile numbers. This locked out millions of NRIs. Your NRE and NRO accounts were ready. But you could not link them to UPI. That barrier is now gone.

The RBI and NPCI Policy Update

In January 2023, the NPCI made a big announcement. They allowed NRIs to use UPI. You can now use your international mobile number to link your NRE or NRO account.

This was a game-changer. The Reserve Bank of India (RBI) and the NPCI worked together to make this happen. It is fully compliant with FEMA rules. Your money is moving through official, legal channels.

This was not an overnight decision. It was a careful step to include the Indian diaspora in the country’s digital revolution.

Supported Countries and Banks

This service is not yet available for every single country code. But it covers most of the major countries where NRIs live.

The supported country codes include:

- +1 (USA, Canada)

- +44 (UK)

- +971 (UAE)

- +966 (Saudi Arabia)

- +65 (Singapore)

- +60 (Malaysia)

- +61 (Australia)

- +974 (Qatar)

Many leading Indian banks now support this feature. The list is growing every month. Key banks that offer UPI for NRIs include:

- Axis Bank

- HDFC Bank

- ICICI Bank

- State Bank of India (SBI)

- IDFC First Bank

- Kotak Mahindra Bank

It is always best to check with your bank directly. Or look at the official NPCI website for the latest list of supported banks.

Step-by-Step: How NRIs Can Set Up UPI

Setting up UPI is like setting up a new social media account. It is a straightforward process. Follow these steps, and you will be ready to pay in minutes.

| Step | Action | What You Need to Know |

|---|---|---|

| 1 | Hold a valid NRE or NRO account | This is the foundation. Your bank account must be an NRI account. Regular savings accounts will not work for this purpose. |

| 2 | Register your foreign number with the bank | Your international mobile number must be officially linked to your NRE/NRO account. Call your bank’s NRI desk to confirm this. |

| 3 | Download a UPI app | You can use your bank’s own app (like iMobile by ICICI) or a third-party app like BHIM. Some banks require you to use their specific application. |

| 4 | Link your bank account and verify | Open the app. Select your bank. The app will send an OTP to your foreign number to verify it is you. |

| 5 | Create your UPI ID and PIN | Choose a unique UPI ID, like yourname@icici. Finally, you will create a secure four or six-digit UPI PIN to authorize transactions. |

A friend of mine in Dubai did this recently. He used his UAE number. He had his ICICI NRO account ready. The whole process, from downloading the app to making his first payment, took less than ten minutes. He was shocked at how easy it was.

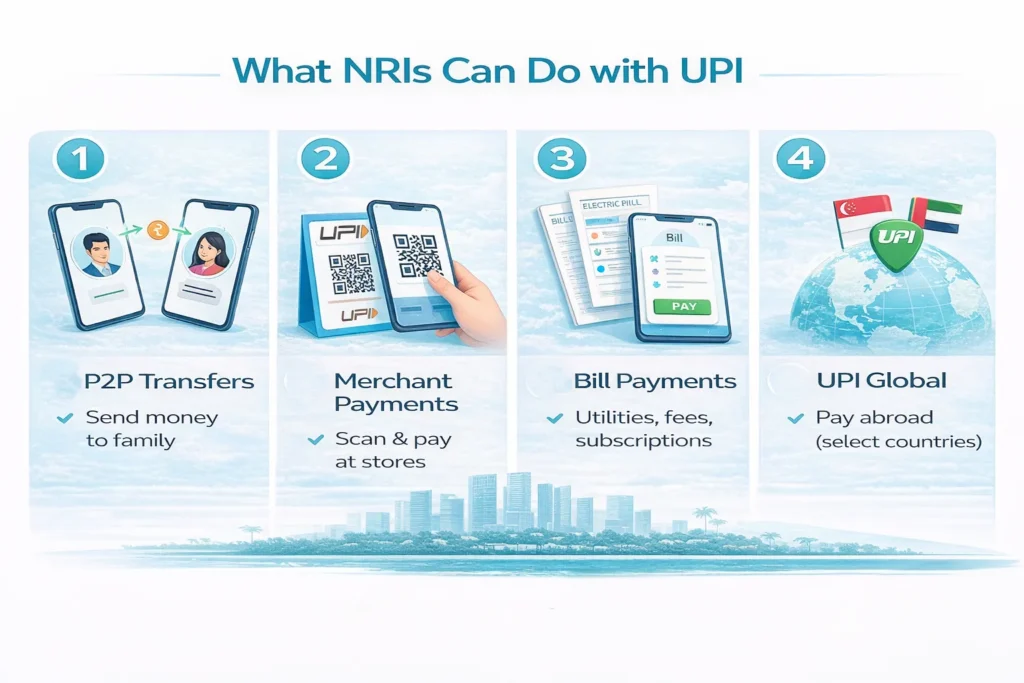

What NRIs Can Do with UPI

Once your UPI is active, a world of financial convenience opens up. It is not just for sending money to one person. The uses are vast.

- Person-to-Person (P2P) Payments: This is the most common use. You can send money instantly to family in India. Paying rent for a property you own? Send it via UPI. Helping with parents’ medical bills? UPI makes it immediate. You can even split a dinner bill with friends back home.

- Merchant QR Code Payments: When you visit India, you can pay at almost any store. From large retail chains to the smallest chai stall, QR codes are everywhere. Just open your app, scan the code, enter the amount, and approve with your PIN. The payment is done.

- Bill Payments: You can pay utility bills for your family home in India. Electricity, water, gas, and internet bills can all be paid through UPI apps. You can also pay for subscriptions and school fees.

- Limited International Use (UPI Global): This is a newer feature. It allows you to pay international merchants directly from your Indian bank account. It is available in select countries like Singapore and the UAE. Look for merchants that display the UPI logo abroad.

Benefits of Using UPI as an NRI

Why should you go through the setup? The benefits are real and tangible.

- Instant Transfers: Money moves from your account to the recipient’s in seconds. No more waiting for wire transfers that can take days.

- Cost-Effective: Sending small amounts via international wire transfer is expensive. Banks charge high fees. UPI transactions are virtually free. This saves you a significant amount over time.

- Full Digital Ecosystem Access: You are no longer an outsider looking in. You can use every Indian app and service that requires UPI. This includes investing apps, e-commerce sites, and donation platforms.

- Seamless Travel Payments: Your trips to India become smoother. You do not need to carry as much cash. You do not have to worry about currency exchange for small daily expenses. Your phone is your wallet.

Limitations and Rules to Know

No system is perfect. It is important to know the boundaries so you are not caught by surprise.

- Supported Countries Only: If you live in a country with a code that is not yet supported, you will have to wait. The list is expanding, but it is not universal.

- Bank and App Support Varies: Just because the NPCI allows it, does not mean every bank has implemented it perfectly. Some bank apps may still have bugs when using a foreign number. Patience is key.

- Transaction Limits Apply: UPI has per-transaction and daily limits set by the RBI and your bank. For most P2P transactions, the limit is often ₹1,00,000 per transaction. There is also a daily cap on the number of transactions. Check with your bank for their specific limits.

- OTP Delays Can Happen: Since the OTP is sent to your foreign number, there can sometimes be a delay. Network issues between countries can cause this. It is rare, but it is good to be aware of it.

- Legal Compliance: All transactions are monitored under RBI and FEMA guidelines. This is for your safety and the country’s financial security. Use your accounts for legitimate purposes only.

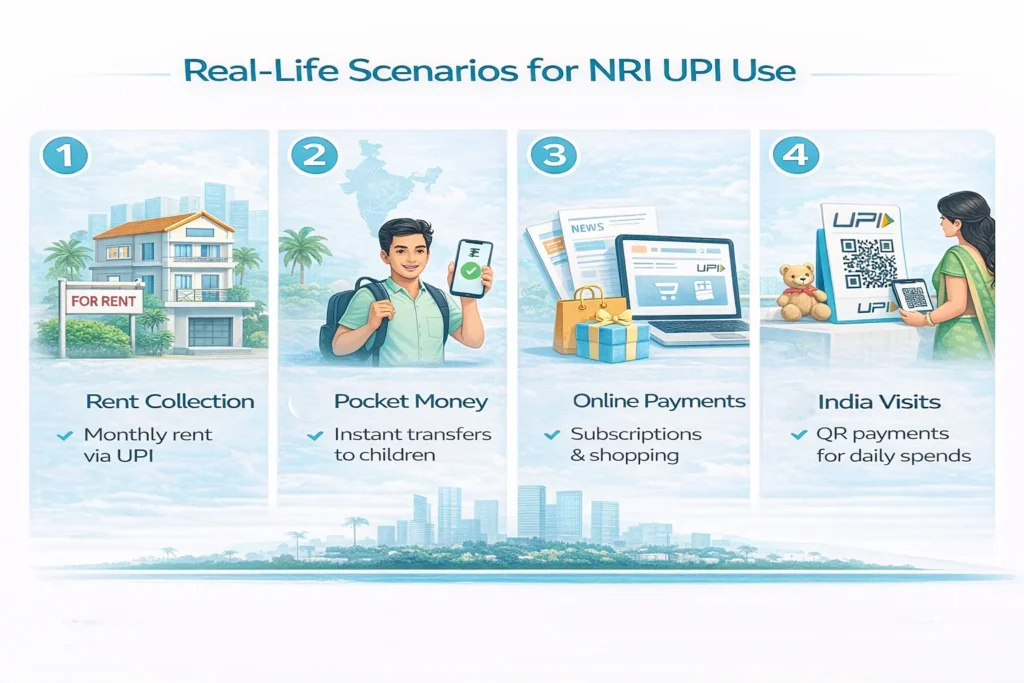

Real-Life Scenarios for NRI UPI Use

Let us make this practical. How would you use this in your daily life?

- Paying Rent for Your Indian Home: You own a flat in Mumbai that is rented out. Instead of asking your tenant to deposit a check or dealing with wire transfers, they can simply send the rent to your UPI ID each month. It is instant and trackable.

- Sending Pocket Money to Your Children: Your son is studying at a university in Pune. His expenses are unpredictable. With UPI, you can send him money the moment he asks for it. He gets it instantly to pay for books, food, or anything else.

- Paying for Online Services: You want to subscribe to an Indian news website. Or you want to buy a gift from an Indian e-commerce site for your parents’ anniversary. At checkout, you can select UPI and pay directly from your NRO account.

- Managing Expenses During Visits: You are in India for a wedding. There are countless small expenses: gifts for relatives, payments to decorators, tips for drivers. Instead of constantly withdrawing cash, you pay with QR codes. It is fast, secure, and you have a perfect record of all your spending.

Frequently Asked Questions

Here are answers to the most common questions NRIs have about using UPI.

Can NRIs use UPI without an Indian SIM card?

Yes, absolutely. The whole point of the new rule is that you can use your international mobile number. You do not need an Indian SIM at all.

Can NRIs receive payments on UPI?

Yes, you can receive money just as easily as you can send it. Someone can send money to your UPI ID, and it will credit directly to your linked NRE or NRO account.

Are there foreign exchange charges on UPI transactions?

No. Since UPI transactions are done in Indian Rupees from your Indian bank account (NRE/NRO), there are no forex charges involved. The money is already in INR.

What happens if the OTP fails to deliver to my foreign number?

This can happen due to international network issues. First, try again after a few minutes. If it persists, contact your mobile network provider to ensure you can receive international SMS. As a last resort, call your bank’s customer support for help.

Is UPI usage by NRIs legal under FEMA?

Yes. The system was enabled by the NPCI with approval from the RBI. As long as you are using your legitimate NRE or NRO accounts for permitted transactions, it is fully legal and compliant with FEMA regulations.

0 Comments