Moving your hard-earned money from India to your country of residence can feel like a giant puzzle. The rules seem complicated. The paperwork is daunting. A small mistake can lead to frustrating delays.

But what if you could navigate this process with confidence?

This guide breaks down the eight most effective methods for NRIs to repatriate funds from India. We will walk you through each option in simple, clear language. You will learn the limits, the steps, and the documents you need. Our goal is to turn a complex procedure into a straightforward task.

Let us get started.

Why Choosing the Right Repatriation Method Matters

Choosing the wrong way to send your money abroad is like taking a detour on a long trip. It wastes time, costs more, and causes unnecessary stress.

Each type of bank account and income source in India has its own set of repatriation rules, governed by the Reserve Bank of India (RBI) and the Foreign Exchange Management Act (FEMA). Using the correct method ensures your transfer is smooth, legal, and tax-efficient. It helps you avoid the headache of your bank rejecting the transaction or facing questions from tax authorities.

Think of this guide as your roadmap. It will show you the fastest and most reliable routes for your specific situation.

Method 1: Repatriate from NRE Account (No Limit)

An NRE (Non-Resident External) account is your best friend for easy repatriation. Money in this account is fully repatriable. This means you can send every single rupee abroad without any upper limit.

What does this mean for you? Any funds you transfer from overseas into your NRE account, or the interest it earns, can be sent right back out. It is a two-way street for your money.

How to do it:

- Log in to your NRE bank’s online portal.

- Navigate to the “Funds Transfer” or “Outward Remittance” section.

- Choose the overseas beneficiary (that is you in your foreign country) and enter the amount.

- Confirm the transaction with the required authentication.

Key Takeaway: The NRE account is the simplest channel for repatriation because it has no limits. The money you put in, and the interest it earns, can always come out.

Method 2: Repatriate from FCNR (B) Account (No Limit)

The FCNR (B) – Foreign Currency Non-Resident (Bank) – account is similar to the NRE account in terms of repatriation. The main difference is that you open this account in a foreign currency like US Dollars, British Pounds, or Euros. The entire balance, both principal and interest, is fully repatriable.

Why would you use this? It protects you from exchange rate fluctuations. If you deposited US Dollars, you will get US Dollars back.

The process is just as easy:

- Upon the maturity of your FCNR (B) deposit, the funds will be credited to your NRE or NRO account.

- From there, you can repatriate them as needed. Since the source is an FCNR (B) account, there are no restrictions on the amount.

Key Takeaway: Like the NRE account, FCNR (B) funds are 100% repatriable. It is a safe harbor for your foreign currency savings in India.

Method 3: Transfer from NRO Account (Up to USD 1 Million/Year)

The NRO (Non-Resident Ordinary) account is where most NRIs keep their Indian income, like rent or dividends. This is where things get a little different. Repatriation from an NRO account is not unlimited.

You can repatriate up to USD 1 million per financial year (April to March) from your NRO account. This is a combined limit for all your NRO accounts and includes other specific repatriations.

However, there is a crucial condition. You cannot just send out any money. The funds you want to repatriate must be from eligible sources. The most important of these are:

- Rental income from a property in India.

- Dividends or interest earned on investments.

- Pension or family pension received in India.

The most critical step? You must pay any applicable Indian taxes on this income before you can send it abroad. Your bank will require a certification from a Chartered Accountant to prove the taxes are paid.

How to do it:

- Ensure the funds you wish to repatriate are from eligible sources and that you have paid the due taxes.

- Obtain a Chartered Accountant’s certificate (Form 15CB).

- Fill out Form 15CA online on the Indian tax portal and declare the remittance.

- Submit these forms to your bank and request the outward remittance.

Key Takeaway: The NRO account allows repatriation, but it is capped and has tax compliance at its core. Always have your tax paperwork in order.

Method 4: Repatriate Capital Gains via PIS

If you invest in the Indian stock market as an NRI, you must do so through a Portfolio Investment Scheme (PIS). This is a special platform with your bank that allows you to buy and sell shares.

The good news is that you can repatriate the sale proceeds of these shares. The process is straightforward but follows a specific path.

Here is how it works:

- You sell your shares through your PIS-enabled trading account.

- The sale proceeds are credited to your linked NRE or NRO account. Using an NRE account is better for easier repatriation later.

- Once the money is in your bank account, you can repatriate it following the rules of that account (unlimited for NRE, up to $1 million for NRO).

Important: You must ensure that the initial purchase of these shares was made through the PIS route. This creates a clear and auditable trail for the RBI.

Key Takeaway: PIS creates a clean financial trail for your stock market gains, making their repatriation a systematic process.

Method 5: Repatriate Proceeds from Property Sales

Selling a property in India is a major financial event. Repatriating those funds is possible, but it is one of the most regulated processes. The RBI wants to ensure the transaction is legitimate.

First, there is a limit. You can repatriate up to USD 1 million per financial year across all your asset sales, including property. This limit is separate from the one for NRO income.

Second, there are two strict conditions:

- The property you are selling must have been bought with readily available foreign currency or through an NRE/FCNR account. Alternatively, you can repatriate the sale proceeds of any two properties, regardless of the original purchase source.

- You must provide documented proof of the sale, like the sale deed, and proof of the original purchase.

The tax payment step is non-negotiable. You must pay the capital gains tax in India and get a Chartered Accountant’s certificate (Form 15CB) before filing Form 15CA for the bank.

Key Takeaway: Repatriating property sale proceeds is possible but comes with a strict cap and heavy documentation. Plan this well in advance and consult a tax advisor.

Method 6: Repatriate Rental Income & Pension Using NRO

This method directly ties into Method 3. Your regular Indian income, like rent from a property or a pension from a former Indian employer, is typically credited to your NRO account.

Repatriating this money is one of the most common use cases for the NRO account’s USD 1 million limit.

For rental income:

- The rent money comes into your NRO account.

- You declare this income and pay income tax on it in India.

- With the tax proof and CA certificate, you can repatriate the after-tax amount.

For pension:

- Similar rules apply. The pension is credited to your NRO account.

- Tax is usually deducted at source (TDS). You need to ensure your tax liability for the year is fully settled.

- Once compliant, you can include this amount in your annual repatriation limit.

Key Takeaway: Your NRO account is the gateway for sending your ongoing Indian income abroad. Consistent tax compliance is the key that unlocks this gateway.

Method 7: Remit through Liberalised Remittance Scheme (LRS)

The Liberalised Remittance Scheme (LRS) is not a separate method, but it is the umbrella rule that governs all these transactions. The USD 1 million limit we keep mentioning is the overall limit under LRS for most permissible transactions, including remittances for family maintenance, gifts, and travel.

For an NRI, when you repatriate from an NRO account or from property sales, you are essentially using a part of your LRS limit. Your bank will track this.

What you need to know: You must fill out a form called A2 for every outward remittance, declaring the purpose of the transfer. Your bank will then report this to the RBI, ensuring you stay within your annual cap.

Key Takeaway: LRS is the framework that makes most repatriation possible. Be aware that your various repatriations from NRO and property sales all add up against one single USD 1 million limit per year.

Method 8: Repatriate via Mutual Funds & Government Bonds

You can also repatriate the redemption proceeds from mutual funds and government bonds you held as an NRI.

The process is very similar to repatriating stock sale proceeds:

- You redeem your mutual fund units or bonds.

- The redemption amount is paid into your linked NRE or NRO bank account.

- Once the money is in your bank, you follow that account’s repatriation rules.

A key point to remember is that the initial investment should have been made from your NRE/NRO account or through proper banking channels. This maintains a clear source of funds.

Key Takeaway: Most financial investments in India can be liquidated, and the proceeds can be routed back to you abroad through your NRI bank accounts.

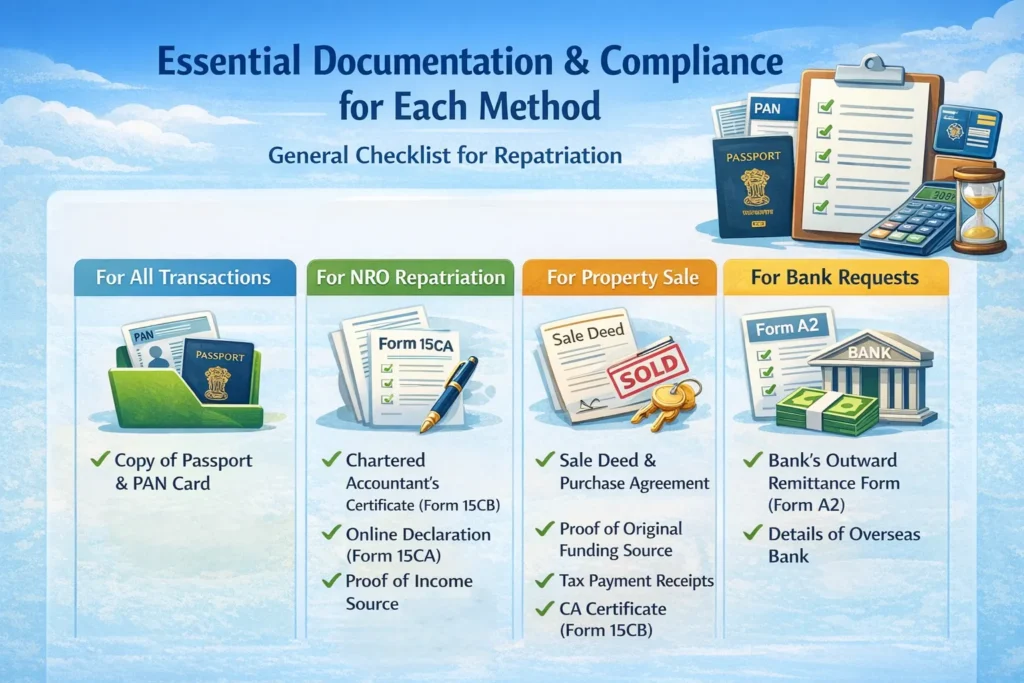

Essential Documentation & Compliance for Each Method

Paperwork is the backbone of a successful repatriation request. Having your documents ready speeds everything up. Here is a general checklist.

- For all transactions: A copy of your passport and PAN card.

- For NRO Repatriation: The Chartered Accountant’s certificate (Form 15CB) and the online declaration (Form 15CA) are mandatory. You will also need proof of the income source, like a rental agreement or dividend vouchers.

- For Property Sale: The sale deed, the purchase agreement (or proof of original funding source), and the tax payment receipts. The CA certificate (Form 15CB) is essential here too.

- For Bank Requests: You will always need to fill out the bank’s specific outward remittance form (Form A2) and provide details of your overseas bank account.

I recently helped a relative gather documents for an NRO repatriation. We spent one weekend collecting the rental agreements and bank statements. Having everything in one folder made the bank visit quick and painless. The manager approved it without a single follow-up question.

Common Pitfalls & How to Avoid Them

Many delays happen for simple, avoidable reasons. Here is what to watch out for.

- Pitfall 1: Mixing Funds. Sending money from a non-repatriable source to a repatriable account does not change its status. You cannot route personal funds through an NRE account to make them repatriable.

- Pitfall 2: Ignoring Taxes. Assuming your bank has deducted tax (TDS) and you have no further liability is a common mistake. You are responsible for your full tax liability. Get a CA to certify it.

- Pitfall 3: Missing Documents. One missing signature or an outdated address proof can set you back by days. Ask your bank for a precise checklist before you apply.

- Pitfall 4: Not Tracking the LRS Limit. If you repatriate from your NRO account and also sell a property in the same year, the amounts will be added together. Exceeding the USD 1 million LRS limit will lead to the rejection of your request.

FAQs

Can I repatriate over USD 1M via NRO in a year?

Generally, no. The USD 1 million per financial year is a strict limit set by the RBI for most capital account transactions under the LRS. There are very few exceptions, and they require special permission from the RBI. It is best to plan your large repatriations across multiple financial years.

What is Form 15CA/CB & when is it needed?

Form 15CB is a certificate from a Chartered Accountant. It states that the tax due on the income you are sending abroad has been paid or is not applicable. Form 15CA is a declaration you file online with the Indian tax authorities based on the 15CB certificate. You need these for almost all repatriations from an NRO account, especially for amounts above a certain threshold.

Are proceeds tax-free on NRE/FCNR repatriation?

The repatriation itself is not a taxable event. However, the income that originally went into the account may have been taxed. For example, the interest earned on an NRE account is tax-free in India. So, repatriating that interest is completely tax-free. The principal you put in was already yours, so sending it out is not taxed. The key is the nature of the funds, not the act of sending them.

How long does each method take?

From an NRE or FCNR account, it can be as fast as 1-3 working days once you initiate the online transfer. For NRO account repatriations, the process takes longer due to compliance checks – typically 5 to 10 working days after you submit all your documents, including Form 15CA/CB. Property sale repatriations can take the longest, often 2-3 weeks, due to the higher value and increased scrutiny.

Final Takeaways & Pro Tips for Smooth Transfers

Repatriating your money from India does not have to be a source of anxiety. It is a structured process. By understanding the rules of each account and income type, you can choose the right path.

Remember these final tips:

- Plan Ahead. Do not wait until you need the money urgently. Start the process early.

- Keep Records. Maintain clear records of all your transactions, especially for property purchases and large investments.

- Talk to Professionals. A good Chartered Accountant who specializes in NRI taxation is worth their weight in gold.

- Communicate with Your Bank. Build a relationship with your bank’s NRI desk. They can guide you through their specific internal processes.

You have worked hard for your money. Now you have the knowledge to move it confidently across borders.

Also Read: 8 Ways NRIs Can Repatriate Funds from India Without Hassle

Also Read: 5 Reasons Why NRIs Should Start a SIP in Indian Mutual Funds

Also Read: Top 7 Online Tools for NRIs to Manage Finances Remotely

0 Comments