The email arrives on a Tuesday morning.

Your father sold the family property. The money sits in an Indian bank. You cannot touch it. Your resident account is frozen. The bank says you need an NRO account.

You stare at the screen. NRO. NRE. FCNR. Three letters. Zero understanding.

I remember my own confusion. I had just moved abroad. My salary needed to go somewhere. My savings in India needed management. Every bank website threw acronyms at me like confetti.

Here is the truth.

Opening an NRI bank account is not hard. You just need to know which account does what. Pick the wrong one and you pay extra tax. Pick the right one and your money flows freely.

Let me break it down so clearly that you never mix up NRE and NRO again.

Why NRIs Need Special Bank Accounts in India

Think of it like this.

You are an Indian citizen. You live abroad. You earn in dollars or dirhams or euros. But you still have financial ties to India.

Maybe you rent out an apartment in Mumbai. Maybe you get dividends from shares bought years ago. Maybe you send money home to your parents.

The Reserve Bank of India watches all this. They have rules. They want to know where your money comes from. They want to track what leaves India and what stays.

Regular resident accounts are not built for this. If you keep using your old account after becoming an NRI, you break the law. Not on purpose. But the bank will catch it eventually.

That is why three special accounts exist. NRE. NRO. FCNR.

Each serves one purpose. Each has different tax rules. Pick the one that matches your situation.

The Three Types of NRI Bank Accounts

Let me introduce you to each one.

NRE Account – Non-Resident External Account

This account holds money you earn outside India. Your Dubai salary. Your London bonus. Your US freelance payments.

Key features:

- Money stays in Indian rupees

- You can send the money back abroad anytime. Full repatriation.

- Interest earned is tax-free in India

- You can open it as savings, current, or fixed deposit

Think of NRE as your foreign income parking spot. Money comes in from abroad. You use it for investments or expenses in India. If you need to send it back out, no questions asked.

NRO Account – Non-Resident Ordinary Account

This account holds money you earn inside India. Your rental income from that Pune apartment. Your pension from an Indian company. Your dividends from Indian shares.

Key features:

- Money stays in Indian rupees

- You can send money abroad, but with limits. Up to one million US dollars per financial year.

- Interest is taxable in India. TDS applies.

- You can open it as savings, current, or fixed deposit

NRO is your Indian income catcher. Money that originates in India stays here. You can use it locally. If you want to move it abroad, you can. Just stay within the limits.

FCNR Account – Foreign Currency Non-Resident Account

This one is different.

The money stays in foreign currency. US dollars. British pounds. Euros. Not rupees.

Key features:

- Fixed deposits only. No savings account.

- Term ranges from 1 year to 5 years

- Interest is tax-free in India

- Full repatriation

- Exchange rate risk? You are protected. The bank bears it.

FCNR is for people who want to save in their home currency. If you believe the rupee will weaken, this protects you. Your money grows in dollars while sitting in an Indian bank.

NRE vs NRO vs FCNR – The Quick Comparison

Here is a table. Bookmark it.

| Feature | NRE Account | NRO Account | FCNR Account |

|---|---|---|---|

| Source of funds | Foreign income | Indian income | Foreign income |

| Currency held | Indian rupees | Indian rupees | Foreign currency |

| Repatriation | Unlimited | Limited to $1 million/year | Unlimited |

| Tax on interest | Tax-free | Taxable | Tax-free |

| TDS applicable | No | Yes | No |

| Account type | Savings, FD, current | Savings, FD, current | Only FD |

| Best for | Sending foreign money to India | Managing Indian earnings | Saving in foreign currency |

Step by Step Guide to Open Your NRI Bank Account

Now for the practical part. How do you actually open one?

Step 1 – Choose Your Account Type

Ask yourself one question.

Where does my money come from?

If it is salary from abroad, you need NRE. If it is rent from your Indian property, you need NRO. If you want both, open both. Many NRIs do.

I opened an NRE for my foreign salary. I kept an NRO for the rent from my Delhi flat. Two accounts. Two purposes. No confusion.

Step 2 – Select Your Bank

Not all banks treat NRIs equally.

Some have better forex rates. Some offer smoother online banking. Some have branches in your current country.

Big players include:

- State Bank of India

- HDFC Bank

- ICICI Bank

- Axis Bank

Compare their NRI services. Check if they have a representative office where you live. Read reviews from other NRIs in your country.

Step 3 – Fill the Online Application

Most banks now let you start online.

Visit the NRI section of the bank website. Choose the account type. Fill the form.

They ask for personal details. Your name. Your date of birth. Your parents names. Your Indian address. Your overseas address.

Take your time here. Mistakes cause delays.

Step 4 – Submit Your Documents

This is where people get stuck.

You need:

- Passport – First and last page, plus any pages with stamps

- Visa or residence permit – Proof you live abroad legally

- Overseas address proof – Utility bill, bank statement, rental agreement

- Indian address proof – Aadhaar, passport, voter ID

- PAN card – Mandatory for all accounts

- Photographs – Recent, passport size

- Proof of occupation – Employment letter or business registration

Some banks ask for more. Some ask for less. But this list covers 90 percent of cases.

Step 5 – Complete KYC Verification

KYC means Know Your Customer. The bank needs to see you.

If you are in India, you walk into a branch. If you are abroad, you have options.

Video KYC is common now. You sit in your living room. A bank officer appears on screen. You show your documents. They take a screenshot. Done.

Embassy attestation is another route. You visit the Indian embassy in your country. They certify your documents. You courier them to India.

Courier submission works too. You send physical copies. The bank verifies and returns them.

Step 6 – Fund Your Account

The account is not active until you put money in.

Minimum balance varies by bank. Some want 50,000 rupees. Some want 1 lakh. Some have zero balance accounts for NRIs.

Transfer money from your foreign account. Use bank transfer or specialized remittance services. The money lands in your new NRI account.

Documents Required for NRI Account Opening

Let me give you the detailed checklist. Print this.

Essential documents:

- Passport – Self-attested copies of first and last page

- Visa – Copy showing your current status abroad

- Residence permit – If your country issues one

- Overseas address proof – Electricity bill, bank statement, driving licence

- Indian address proof – Aadhaar, passport, or any government document

- PAN card – Mandatory for all transactions

- Photographs – Two recent, white background

- Signature proof – Usually on the form itself

Additional if applicable:

- Employment letter – If salaried abroad

- Business registration – If self-employed

- Income proof – For certain high-value accounts

- Reference from existing customer – Some banks ask

A friend once forgot his visa copy. He sent the application. The bank rejected it after two weeks. He had to start over. Do not be that person.

Open NRE Account Online from Abroad

Good news. You can do this without visiting India.

I opened my NRE account while sitting in a café in Dubai. Coffee in one hand. Phone in the other.

Here is how.

Go to the bank’s NRI portal. Select NRE savings account. Fill the form. Upload scanned documents. Schedule video KYC.

During video KYC, the officer asks basic questions. Your name. Your date of birth. Your current location. Show your passport. Show your visa.

The whole call lasts ten minutes.

Once approved, you get account details by email. You can start transferring money immediately. The debit card arrives at your overseas address in a week or two.

Banks that offer smooth online NRE opening:

- ICICI Bank – Their Money2India platform is excellent

- HDFC Bank – NRI services are well structured

- SBI – Branches worldwide, but online process varies by country

- Axis Bank – Good digital experience

Open NRO Account for Indian Income

Your NRO account handles everything that earns money inside India.

Rental income goes here. Pension from your old Indian employer goes here. Dividends from shares bought years ago go here.

The process is similar to NRE. Same documents. Same KYC. Same online application.

But remember one thing.

NRO interest is taxable. The bank deducts TDS at 30 percent on interest above a certain limit. You claim this back when filing your income tax return in India.

Also, if you sell property in India, the money goes to NRO. You can repatriate it later, up to one million dollars per year.

I have seen NRIs accidentally put rental income into NRE. The bank catches it eventually. They reverse the transaction. It creates a mess. Keep Indian income in NRO. Keep foreign income in NRE.

FCNR Account Opening and Benefits

FCNR is the quiet cousin. Less discussed. But very useful.

You open it when you want to keep money in foreign currency. Dollars. Pounds. Euros. Whatever you earn in.

The money stays in that currency for the entire deposit term. 1 year. 2 years. Up to 5 years.

At maturity, you get back the same currency. Plus interest in that currency.

Why do this?

Exchange rate protection.

If the rupee falls against the dollar, your NRE deposit loses value in dollar terms. Your FCNR deposit stays exactly where it is. The bank bears the currency risk, not you.

Interest rates on FCNR are usually lower than NRE. But the safety is worth it for some people.

Opening an FCNR is similar to NRE. Same documents. Same process. But you specify the currency and deposit term upfront.

Convert Your Resident Account to NRO

This is mandatory.

The day you become an NRI, your resident account status changes. You cannot keep using it as if nothing happened.

Banks find out eventually. When your visa details show up. When your overseas address appears. Then they freeze the account until you convert it.

The conversion process:

- Visit your bank branch or use online NRI services

- Submit your NRI status proof (visa, residence permit)

- Fill the account conversion form

- Provide updated KYC documents

- Sign a new mandate for the NRO account

Your old account number usually stays the same. But the account type changes in the bank’s system. New rules apply. New tax treatment applies.

Do this within a reasonable time. Do not wait years. It creates compliance headaches.

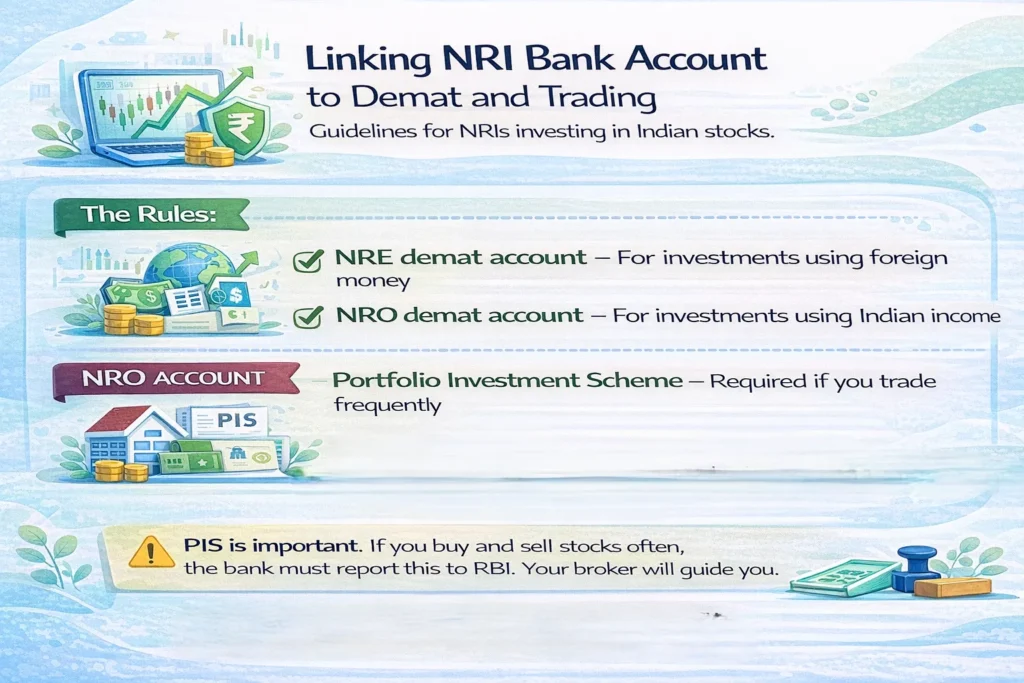

Linking NRI Bank Account to Demat and Trading

You want to invest in Indian stocks. Good move.

But NRIs cannot use regular demat accounts. You need a special one.

The rules:

- NRE demat account – For investments using foreign money

- NRO demat account – For investments using Indian income

- Portfolio Investment Scheme – Required if you trade frequently

PIS is important. If you buy and sell stocks often, the bank must report this to RBI. Your broker will guide you.

Most NRIs start with a simple buy-and-hold strategy. That works fine without PIS. But check with your bank and broker before trading.

Minimum Balance and Charges

Banks need to make money. They charge fees.

Typical charges:

- Minimum balance – 10,000 to 1,00,000 rupees depending on bank and city

- Non-maintenance penalty – 500 to 1,000 rupees per month if balance drops

- Inward remittance charges – 0 to 1 percent of transfer amount

- Outward remittance charges – 500 to 2,000 rupees per transaction

- Debit card annual fee – 500 to 1,500 rupees

- Foreign currency conversion – Bank’s spread on exchange rate

Compare these before choosing a bank. Some waive charges if you maintain a high balance. Some offer zero balance accounts for NRIs.

Tax Rules for NRI Bank Accounts

This is where people get confused.

NRE account interest – Fully tax-free in India. No TDS. No income tax. You do not even need to show it in your Indian return.

NRO account interest – Fully taxable. Bank deducts TDS at 30 percent on interest above 5,000 rupees per year. You file a return and claim refund if your total income is below taxable limit.

FCNR account interest – Tax-free like NRE. No TDS. No income tax.

TDS on NRO can be reduced if you have a lower total income. File Form 10F with the bank. Provide a Tax Residency Certificate from your country. Use the India Double Taxation Avoidance Agreement.

I know an NRI in Canada who got 30 percent TDS on his NRO interest every year. He never filed for lower deduction. He lost thousands in refunds he never claimed. Do not let that be you.

How NRIs Choose the Best Bank

Every bank claims to be best for NRIs. Here is what actually matters.

Forex rates : Banks add a margin to the exchange rate. A difference of 10 paise on a lakh of rupees is 1,000 rupees. Check rates before transferring.

Remittance speed : Some banks credit same day. Some take three days. If you send money monthly, speed matters.

Digital banking : Can you open account online? Can you transfer money from your phone? Is the app usable abroad?

Global presence : SBI has branches in many countries. HDFC has representative offices. ICICI has partnerships. If you want face-to-face service, choose a bank with local presence.

Customer service : Call them. See if they pick up. Email them. See if they reply. Bad service is painful when you need help.

Interest rates : Compare savings account rates. Compare FD rates. But remember, NRE interest is tax-free, so effective return is higher than it looks.

Common Mistakes NRIs Make

I collect these stories to help you avoid them.

Mistake 1 – Choosing wrong account type

A doctor in the US put his Indian rental income into NRE. The bank reversed the transaction after three months. He had penalties and confusion.

Mistake 2 – Not updating PAN

PAN is mandatory. If your account is not linked to PAN, transactions get blocked. TDS gets deducted at higher rate.

Mistake 3 – Ignoring KYC updates

Banks periodically ask for updated KYC. Ignore them and your account gets frozen. Then you are stuck.

Mistake 4 – Keeping resident account active

Using your old resident account after becoming NRI is illegal. The bank will catch you. Better to convert proactively.

Mistake 5 – Not tracking exchange rates

Transferring money without checking rates costs thousands. Use comparison sites. Time your transfers.

Mistake 6 – Missing TDS refunds

Pay tax on NRO interest. But if your total income is below taxable limit, file a return and claim refund. Many NRIs do not bother. They leave money on the table.

Repatriation Rules Simplified

Repatriation means sending money out of India.

From NRE – Unlimited. Any amount. Any time. No questions.

From NRO – Limited to one million US dollars per financial year. You need Form 15CA and 15CB. The bank handles most of it, but you must provide documents.

From FCNR – Unlimited at maturity. You get back your foreign currency.

If you sell property in India, the money goes to NRO. You can repatriate sale proceeds up to the limit. For multiple properties, spread sales across years if needed.

Opening Joint Accounts

You can open joint accounts.

NRI + NRI – Both must be Non-Resident Indians. Works for NRE, NRO, FCNR.

NRI + Resident Indian – Only for NRO accounts. The resident must be close relative. Spouse, parents, children. Not friends. Not distant cousins.

Joint accounts operate on either or survivor basis. Both can operate independently unless you specify otherwise.

Safety and Compliance

Your money is safe.

Indian banks are regulated by RBI. Deposits are insured up to 5 lakh rupees per bank. For larger amounts, spread across banks.

Compliance matters though.

RBI tracks all NRI transactions. Large deposits get flagged. Unusual patterns get reported. Keep everything documented.

Do not accept cash deposits in your NRI account. Do not let friends use your account to transfer money. These are red flags.

If you follow the rules, you have nothing to worry about.

Conclusion

Here is what I want you to do.

Figure out where your money comes from. Foreign salary? Go NRE. Indian rent? Go NRO. Both? Open both.

Pick a bank. Start the online application today. Not tomorrow. Not next week. Today.

The form takes twenty minutes. The video KYC takes ten. A week later, your account is active.

Then you relax. Your money has a home. Your finances are compliant. Your future investments have a foundation.

Thousands of NRIs open accounts every month. They figure it out. So will you.

Just start.

Frequently Asked Questions

Can NRIs open a bank account in India without visiting the country?

Yes. Most major Indian banks offer fully online account opening. You complete the application, upload documents, and do video KYC from your phone. The debit card arrives at your overseas address.

What is the difference between NRE and NRO accounts?

NRE holds foreign income, offers tax-free interest, and allows unlimited repatriation. NRO holds Indian income like rent or pension, has taxable interest, and allows limited repatriation up to one million dollars yearly.

Which NRI account is best for saving foreign currency?

FCNR account is designed for this. You deposit and maintain money in foreign currency like dollars or pounds. The bank bears exchange rate risk. Interest is tax-free. Withdrawal happens in the same currency.

What documents are required to open an NRI account?

You need passport, valid visa or residence permit, overseas address proof, Indian address proof, PAN card, photographs, and proof of occupation. Some banks ask for additional documents depending on your country of residence.

Is NRE account interest taxable in India?

No. Interest earned on NRE savings and fixed deposits is completely tax-free in India. You do not need to show it in your income tax return. This makes NRE attractive for parking foreign earnings.

Can I convert my existing resident account to NRO?

Yes. You must do this after becoming an NRI. Visit your bank branch or use online NRI services. Submit proof of NRI status and updated KYC documents. Your account number usually remains the same.

How much money can I send abroad from NRO account?

You can repatriate up to one million US dollars per financial year from your NRO account. This requires filing Form 15CA and 15CB. The bank assists with documentation but you must provide source of funds proof.

Can NRIs open joint accounts with residents?

Yes, but only for NRO accounts. The resident must be a close relative like spouse, parents, or children. Friends and distant cousins are not permitted. NRE and FCNR joint accounts require both holders to be NRIs.

Do I need a PAN card for NRI bank account?

Yes, PAN is mandatory. Without it, TDS gets deducted at higher rates on interest income. Your transactions may also get blocked. Apply for PAN online if you do not already have one.

What happens to my NRI account when I return to India permanently?

You must convert it back to a resident account. Inform your bank about your return within a reasonable time. Provide proof of your return and updated KYC. The account type changes but number usually stays same.

0 Comments