Whats the tax rule on NRIs investment in Indian mutual funds?

Investing in Indian mutual funds can be an attractive opportunity for NRIs (Non-Resident Indians), but it is essential to understand the tax implications. Here’s a breakdown of the key tax rules applicable to NRIs on mutual fund investments in India:

1. Taxation on Capital Gains:

The tax treatment for capital gains on mutual fund investments depends on the type of mutual fund and the holding period:

Equity-Oriented Mutual Funds:

- Short-Term Capital Gains (STCG): Gains from equity mutual funds held for less than 12 months are classified as short-term and taxed at 15%.

- Long-Term Capital Gains (LTCG): Gains from equity mutual funds held for more than 12 months are considered long-term. Gains up to ₹1 lakh in a financial year are tax-exempt, while gains above ₹1 lakh are taxed at 10% without the benefit of indexation.

Debt-Oriented Mutual Funds:

- Short-Term Capital Gains (STCG): Gains from debt mutual funds held for less than 36 months are considered short-term and are taxed as per the investor’s income tax slab.

- Long-Term Capital Gains (LTCG): Gains from debt mutual funds held for more than 36 months are considered long-term and are taxed at 20% with indexation benefits. Indexation adjusts the purchase price for inflation, reducing the tax burden.

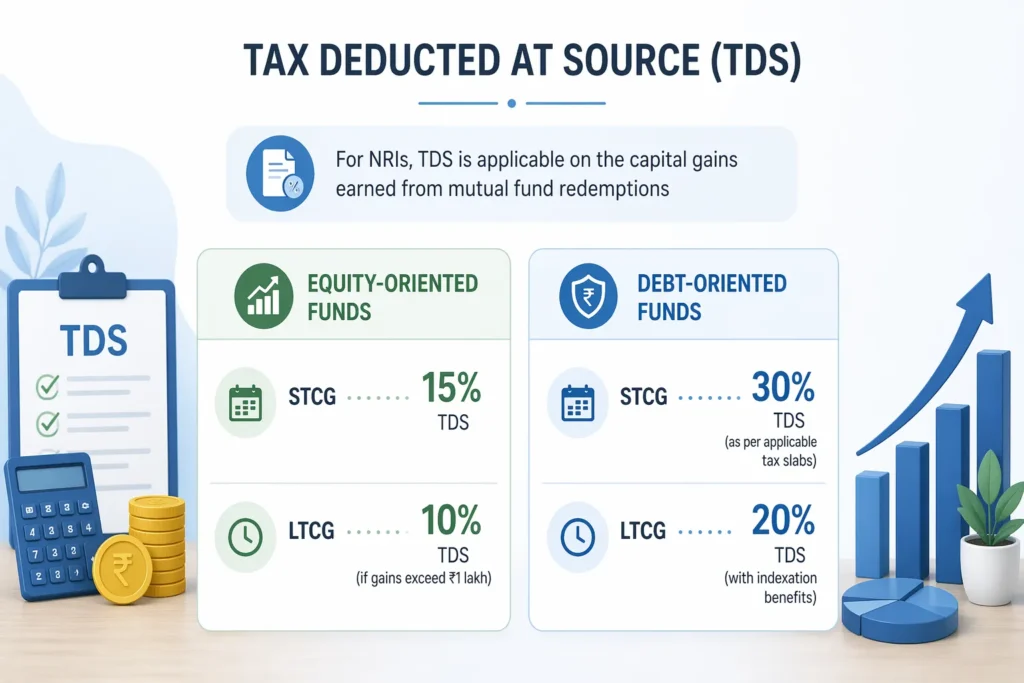

2. Tax Deducted at Source (TDS):

For NRIs, Tax Deducted at Source (TDS) is applicable on the capital gains earned from mutual fund redemptions:

Equity-Oriented Funds:

- 15% TDS is applied on STCG.

- 10% TDS is applied on LTCG (if gains exceed ₹1 lakh).

Debt-Oriented Funds:

- TDS of 30% is applicable on STCG (as per applicable tax slabs).

- TDS of 20% is applicable on LTCG, considering indexation benefits.

NRIs need to file their income tax returns in India to claim a refund if the TDS deducted is higher than their actual tax liability.

3. Taxation of Dividends:

Dividends received from mutual funds are taxable in the hands of the investor. For NRIs, dividends are subject to TDS at a rate of 20%. This rate can be reduced if a Double Taxation Avoidance Agreement (DTAA) exists between India and the NRI’s country of residence, allowing NRIs to avoid being taxed twice on the same income.

4. Double Taxation Avoidance Agreement (DTAA):

India has DTAA with several countries, allowing NRIs to either get a tax credit or tax exemption on the income taxed in India. NRIs should provide the necessary documents like Tax Residency Certificate (TRC) and Form 10F to avail of DTAA benefits. The DTAA rates and provisions vary depending on the country of residence, potentially reducing the overall tax burden on investments.

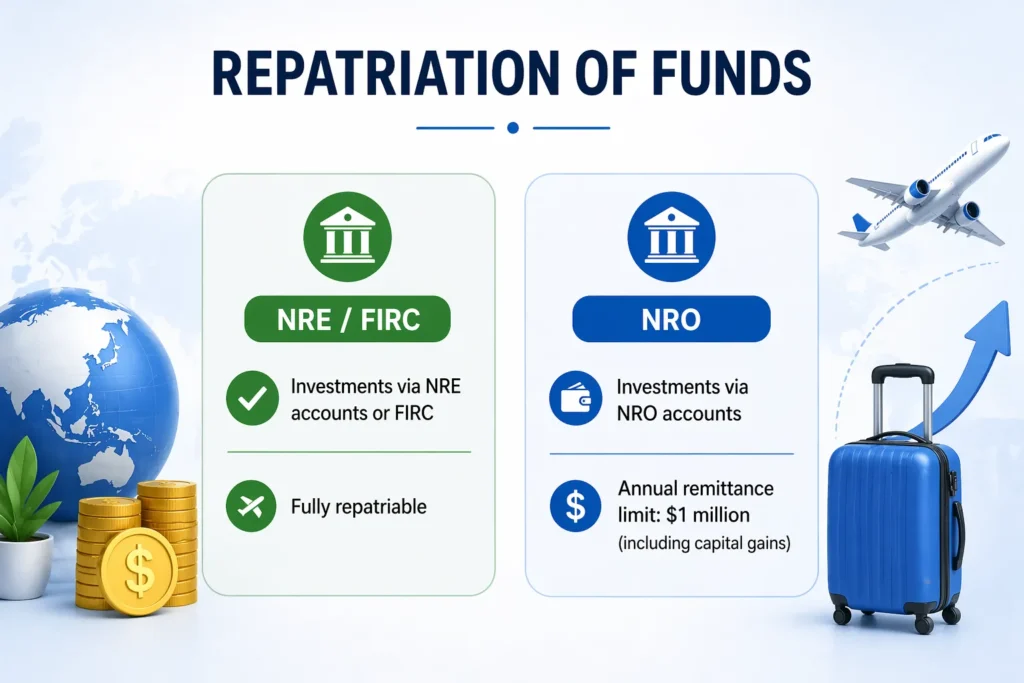

5. Repatriation of Funds:

The repatriation of funds from mutual fund investments is allowed but comes with conditions:

- Investments made through Non-Resident External (NRE) accounts or Foreign Inward Remittance Certificates (FIRC) are repatriable.

- Investments from Non-Resident Ordinary (NRO) accounts are subject to an annual remittance limit of $1 million, including capital gains.

Key Considerations for NRIs Investing in Indian Mutual Funds:

- Choose the Right Bank Account: NRIs should use an NRE or NRO account to invest in mutual funds.

- Filing of Income Tax Returns: Even though TDS is deducted at source, NRIs should file their returns in India to claim refunds or adjust their tax liability.

- Check DTAA Benefits: Understanding the DTAA between India and the NRI’s country of residence can significantly reduce the tax burden.

- Monitor Holding Periods: Knowing the difference in holding periods for equity and debt funds can help in better tax planning.

Understanding these rules helps NRIs make informed investment decisions in Indian mutual funds, optimizing returns while staying compliant with tax regulations. Consulting with a tax advisor familiar with NRI taxation is often recommended to ensure the best outcomes.

0 Comments