Section 195 of the Income Tax Act, 1961 governs TDS on payments made to non-residents. If you are paying an NRI for a property purchase, consulting work, royalties, or anything else taxable in India you are required to deduct tax before the money leaves your account. The obligation sits with the payer, not the NRI.

Most people only discover this after the payment has already gone through. That is when the notices start.

This guide covers everything you need to know about Section 195 compliance:

- What Section 195 is and which payments it applies to

- TDS rates for FY 2025-26 and FY 2026-27, including surcharge and cess

- How Section 195 differs from Section 194IA the mix-up that costs property buyers the most

- How NRIs can reduce TDS through DTAA relief or a lower deduction certificate

- Documents required for both the payer and the NRI payee

- Consequences of non-compliance interest, penalties, and disallowance under Section 40(a)(i)

Whether you are buying property from an NRI seller, paying a foreign consultant, or an NRI trying to understand what gets deducted from your Indian income this guide gives you the full picture.

What Is Section 195 of the Income Tax Act?

Let us start with a direct answer.

Section 195 of the Income Tax Act 1961 requires any person making a payment to a non-resident that is chargeable to tax in India to deduct TDS before making that payment. The obligation to deduct lies with the payer. Not the NRI.

Think of it like this. When you pay a contractor, you hold back a portion for taxes. Section 195 works the same way. Except here, the "contractor" lives abroad.

A few key things to understand:

- It applies to any payer individual, company, firm, or HUF. Not just businesses. If you are an individual buying property from an NRI seller, Section 195 applies to you personally.

- It covers any sum chargeable under the Income Tax Act. It does not limit itself to specific income types. The scope is deliberately broad.

- TDS must be deducted before payment is made or when the amount is credited to the NRI's account. Whichever comes first. You cannot pay first and deduct later.

- It applies whether you are a resident paying an NRI or an Indian company paying a foreign entity.

Most people only hear about Section 195 after they have already made the payment. That is the worst time to hear about it.

What Types of Income Are Covered Under Section 195?

Here is where a lot of payers get confused. They think Section 195 only applies to property deals. It does not.

Section 195 covers any income of a non-resident that is chargeable to tax in India. In practice, that is a long list:

- Interest income - on loans, deposits, and debentures paid to NRIs

- Royalties - payments for use of intellectual property, patents, or trademarks

- Fees for technical services - consulting fees, management fees, technical support paid to non-residents

- Capital gains - when an NRI sells Indian property, shares, or other assets and receives the sale proceeds

- Rent - payments for use of property or equipment owned by an NRI

- Salary - for services rendered inside India by a non-resident

- Any other income that is taxable in India under the Income Tax Act

Now here is an important clarification that saves payers a lot of confusion.

Not all payments to NRIs attract TDS. Income that is not chargeable to tax in India falls outside Section 195 completely. NRE account interest is tax-free in India. FCNR deposit interest is also exempt. If you are remitting interest earned on an NRE account, you do not need to deduct TDS.

The test is simple. Ask yourself one question: Is this income taxable in India? If yes, Section 195 applies. If no, it does not.

TDS Rates Under Section 195 of Income Tax Act — FY 2025-26 and FY 2026-27 Rate Chart

This is what most people come searching for. Here are the base TDS rates under Section 195 for FY 2025-26 and FY 2026-27:

| Type of Payment | Base TDS Rate | Surcharge Applicable | Notes |

|---|---|---|---|

| Interest (other than Sec 194LB / 194LC) | 20% | Yes | On NRI loans, deposits |

| Royalties | 10% | Yes | Revised by Finance Act 2023 |

| Fees for Technical Services | 10% | Yes | Consulting, management fees |

| Long-term capital gains on property (Sec 112) | 12.5% | Yes | Post-Budget 2024 |

| Short-term capital gains on equity (Sec 111A) | 20% | Yes | STT-paid transactions |

| Long-term capital gains on equity above Rs 1.25 lakh (Sec 112A) | 12.5% | Yes | Post-Budget 2024 |

| Any other income chargeable to tax | 30% | Yes | Default rate |

Surcharge kicks in on top of the base rate:

- 10% surcharge if total income exceeds Rs 50 lakh

- 15% surcharge if total income exceeds Rs 1 crore

- 4% Health and Education Cess on tax plus surcharge

Take the 20% base rate. Add 15% surcharge. Add 4% cess. The effective rate comes out to roughly 23.92%. That is a significant chunk of any payment.

One more thing. If the NRI's country of residence has a DTAA (Double Taxation Avoidance Agreement) with India, the treaty rate on their income may be lower than the domestic rate in this table. Always check the applicable DTAA before deducting. You are allowed to apply the lower rate, subject to the NRI providing prescribed documents such as a Tax Residency Certificate (TRC), Form 10F, and other declarations as applicable.

Important: TDS rates especially on royalties and capital gains were revised by the Finance Act 2023 and Budget 2024. Verify the current rates against the latest CBDT circulars before completing any transaction.

Need Help With TDS Compliance on NRI Payments? Talk to an NRI Tax Expert at MostlyNRI.

Who Is Responsible for Deducting TDS Under Section 195?

The payer. Full stop.

The NRI sitting in Dubai or Vancouver does not deduct their own tax. You the person writing the cheque or initiating the wire are responsible. And that responsibility comes with teeth.

Here is what the payer must do, in order:

- Get a TAN (Tax Deduction Account Number) before deducting anything. Without a TAN, you cannot deposit TDS to the government.

- Deduct TDS at the applicable rate before making the payment or crediting the NRI's account.

- Deposit TDS to the government within 7 days from the end of the month in which deduction was made. For March, the deadline stretches to 30 days.

- File Form 27Q every quarter. This is the TDS return for payments to non-residents. It is different from Form 26Q, which covers resident payees. Do not mix them up.

Now imagine you skipped all of that.

The Income Tax Department sends you a notice. You are now an "assessee in default" under Section 201(1). That means you personally owe the TDS that was never deducted. Plus interest. Plus penalty. The NRI payee may also face questions about receiving funds without proper TDS compliance.

It is not a comfortable place to be.

Section 195 vs Section 194IA - Why Buyers Often Get This Wrong

I have seen this mistake come up again and again in NRI property transactions. And it makes sense why it happens. Both sections involve property purchases. Both involve TDS. But they are very different in application.

Here is a clean comparison:

| Section 194IA | Section 195 | |

|---|---|---|

| Who does it apply to | Resident buying from another resident | Resident buying from an NRI |

| TDS basis and rate | 1% of sale consideration | TDS is generally deducted on the sale consideration at rates depending on the nature of capital gains, applicable surcharge, cess, DTAA benefits, and any lower deduction certificate |

| TDS return | Form 26QB | Form 27Q |

| Who deducts | Buyer | Buyer |

The typical story goes like this.

A buyer purchases a flat. The seller has an Indian name. The buyer assumes resident status. Deducts 1% under Section 194IA. Feels relieved. Files the return.

Six months later, a notice arrives. The seller was an NRI. Section 195 applied. The difference between 1% and the correct rate is now recoverable from the buyer. With interest running from the date of payment. And a penalty equal to the TDS amount that was missed.

That is a lot of money to pay for an assumption.

How do you avoid this? Simple. Always verify the seller's residential status before the transaction closes. Ask for a copy of their passport with visa stamps. Ask for proof of a foreign address. Ask about their bank account — NRO and NRE accounts may indicate non-resident status, but they do not by themselves determine residential status under the Income Tax Act. A verbal assurance from the seller is not enough. Get it in writing. Get supporting documents.

If the seller's residential status is unclear, obtain written confirmation and supporting documents before proceeding. If there is uncertainty, seek professional tax advice before deciding the applicable TDS provisions.

How NRIs Can Reduce TDS Under Section 195 — Two Routes

If you are the NRI on the receiving end of a payment from India, here is some good news. You are not stuck with the default TDS rate. There are two legitimate ways to reduce what gets deducted.

Route 1 - DTAA Relief

India has signed DTAAs with over 90 countries. If your country of residence is one of them, the treaty may prescribe a lower tax rate on your type of income than the domestic Section 195 rate.

For example, a DTAA may prescribe a lower tax rate on certain types of income such as interest, royalties, or fees for technical services compared to the applicable domestic provisions. The savings can be meaningful, especially on large transactions.

To use this route, you need to give the payer two documents before the payment is made:

- Tax Residency Certificate (TRC) - issued by the tax authority in your country of residence

- Form 10F - filed online on the Indian income tax portal

Once the payer has both, they can legally deduct TDS at the lower DTAA rate. But here is the catch. If you do not provide these documents, the payer must deduct at the higher domestic rate. They have no choice. So do not wait to be asked - send these documents early.

Route 2 - Lower Deduction Certificate

This route works when your actual tax liability is likely to be much lower than what the default rate would produce.

Section 195(2) allows the payer to apply to the Assessing Officer to determine the exact portion of the payment on which TDS should be deducted. This is especially relevant in property sales. Think about it if an NRI sells a flat for Rs 80 lakh but the capital gain is only Rs 12 lakh, deducting TDS on the full Rs 80 lakh is wildly excessive. Section 195(2) addresses this by allowing the AO to determine the portion of the payment that is chargeable to tax. Without such a determination or a lower deduction certificate under Section 197, TDS may be required on the gross sale consideration.

Section 197 allows the NRI payee to apply directly for a lower deduction certificate based on their estimated tax liability. Once the certificate is issued, the payer deducts TDS only at the certified rate.

Both routes require advance planning. You cannot apply for these certificates after the payment has already been made.

Documents Required for Section 195 Compliance

Think of this as your pre-transaction checklist. Have everything ready before the payment date not after.

For the Payer:

- TAN - mandatory before you can deduct and deposit TDS

- PAN of the NRI payee - required when filing the TDS return in Form 27Q

- TRC and Form 10F from the NRI - if you are applying a lower DTAA rate

- Lower deduction certificate - if one has been obtained under Section 197 or Section 195(2)

- Form 15CA and Form 15CB - where applicable under Rule 37BB, these may be required before foreign remittances depending on the nature and amount of the payment. A CA issues Form 15CB where required, after which Form 15CA is filed online on the income tax portal.

For the NRI Payee:

- PAN - required for TDS credit in your AIS and for filing ITR in India

- Tax Residency Certificate (TRC) - from the tax authority in your country of residence

- Form 10F - filed online on the income tax portal; supports your TRC and DTAA claim

- Form 67 - if you are claiming foreign tax credit in your Indian ITR for taxes already paid abroad on the same income

A word on Form 15CA and 15CB. These are important compliance requirements for foreign remittances where applicable under Rule 37BB. Depending on the nature and amount of the remittance, Form 15CA and, in certain cases, Form 15CB may need to be submitted before the bank processes the transfer. Treat these requirements as part of your transaction planning, not an afterthought.

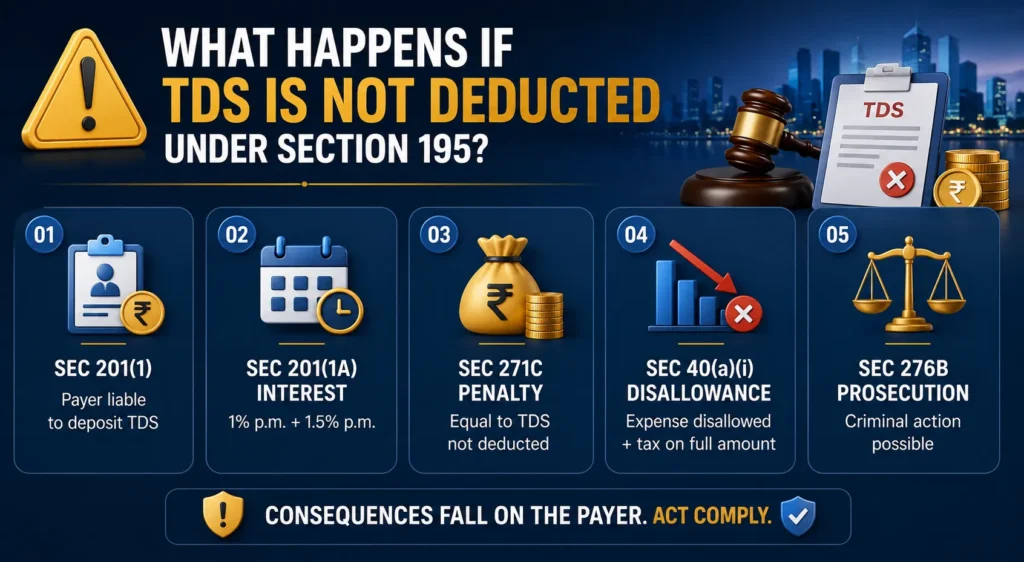

What Happens If TDS Is Not Deducted Under Section 195?

Let us be direct. The consequences fall almost entirely on the payer. And they compound quickly.

- Section 201(1): The payer is treated as an assessee in default and becomes personally liable to deposit the TDS amount to the government

- Section 201(1A) interest: 1% per month from the date of payment to the date TDS was actually deducted - plus 1.5% per month from the date of deduction to the date of deposit to the government

- Section 271C penalty: A penalty equal to the amount of TDS that was not deducted. Miss Rs 5 lakh in TDS, pay another Rs 5 lakh as penalty.

- Section 40(a)(i) disallowance: If a business misses TDS on a payment to a non-resident, the entire payment may be disallowed as a deductible business expense. So the loss is not just the TDS - it is the tax on the full payment amount too.

- Section 276B prosecution: In serious or repeated cases, criminal proceedings are possible.

On the NRI's side, the fallout is different but still real. Repatriating funds without proper TDS documentation becomes difficult. Banks require Form 15CA and 15CB before any foreign remittance. Without proper TDS compliance on the payer's end, those forms cannot be correctly filed.

Here is a simple way to think about it. The financial impact of non-compliance can be substantial because the payer may become liable for unpaid TDS, interest, and penalties where applicable. Getting compliance right upfront costs a fraction of what fixing it later will.

Section 195 - The Bottom Line

Section 195 is not a technicality. It is not something you deal with later. It is a legal obligation that applies the moment you decide to make a payment to a non-resident in India.

The payer carries the full burden of compliance. Get the TAN. Verify the NRI status before the deal closes. Deduct at the correct rate. File Form 27Q on time. Arrange Form 15CA and 15CB before the wire goes out. If the NRI wants to use DTAA or a lower certificate, collect the TRC and Form 10F early.

Miss any of this, and the cost compounds fast. Interest starts from the date of payment. Penalties match the TDS amount. And in the worst cases, the entire payment gets disallowed as a business expense.

Getting Section 195 compliance right is not complicated. But it does require knowing it exists before the transaction, not after.

Need Help With TDS Compliance on NRI Payments? Talk to an NRI Tax Expert at MostlyNRI.

Disclaimer: This article is for informational purposes only. TDS rates and compliance requirements under Section 195 are subject to change based on Finance Act amendments and CBDT circulars. Every transaction has its own structure and specific facts. Consult a qualified NRI tax advisor or Chartered Accountant before making or receiving payments involving non-residents.

Frequently Asked Questions

What is Section 195 of TDS for NRIs?

Section 195 of the Income Tax Act 1961 requires any person making a payment to a non-resident that is taxable in India to deduct TDS before sending the money. It applies to income types like interest, royalties, consulting fees, capital gains, and rent. The payer holds the obligation. The NRI is on the receiving end.

What is the new TDS rule for NRIs under Section 195?

Budget 2024 revised certain capital gains tax rates that may impact TDS calculations under Section 195. The applicable TDS rate depends on the nature of income, applicable surcharge and cess, DTAA benefits, and any lower deduction certificate. The Finance Act 2023 also revised the domestic tax rate for royalties and fees for technical services to 10%. Always confirm the applicable rate with a CA or against the latest CBDT notifications before completing a transaction.

What is TDS on receipt of foreign remittance under Section 195?

When an NRI receives money from India for a property sale, consulting work, or royalties the Indian payer must deduct TDS under Section 195 before remitting. After deduction, the payer must obtain Form 15CB from a CA and then file Form 15CA online. The bank processes the foreign wire only after these forms are submitted. This is how Section 195 TDS compliance is documented for the bank and the RBI.

Who is responsible for deducting TDS under Section 195?

The payer is responsible. Always. Whether you are an individual buying an NRI's flat or a company paying a foreign consultant, the deduction obligation is yours. The NRI does not self-deduct. If the payer misses TDS, they personally owe the amount to the government along with interest and penalties.

What types of income are covered under Section 195?

Section 195 covers any income of a non-resident that is chargeable to tax in India. That includes interest, royalties, fees for technical services, capital gains from Indian property or shares, rent from Indian assets, and salary for work done in India. Income that is tax-exempt in India like NRE account interest is not covered.

What is the 90% rule for non-residents?

The 90% rule refers to an eligibility condition for RNOR (Resident but Not Ordinarily Resident) status under Section 6 of the Income Tax Act. You can qualify as RNOR if you have been a non-resident in India in 9 out of the 10 previous financial years, or if you have spent 729 days or fewer in India in the past 7 years. RNOR is a middle-ground residential status with limited Indian tax obligations. For a detailed breakdown, refer to the MostlyNRI guide on RNOR status.

Can an NRI apply for a lower TDS certificate under Section 195?

Yes. Under Section 197, the NRI can apply to their Assessing Officer for a certificate that authorises the payer to deduct TDS at a lower rate, based on the NRI's estimated actual tax liability. The payer can also file an application under Section 195(2) to get the AO to determine the taxable portion of the payment especially useful in property sales where TDS should only apply to the capital gains, not the full sale price.

What documents does a payer need for Section 195 compliance?

The payer needs a TAN, the NRI's PAN, TRC and Form 10F from the NRI if applying DTAA rates, a lower deduction certificate if one was obtained, and Form 15CA and 15CB before the foreign remittance is processed. All of this must be in place before the payment date.

What is Section 195(2) of the Income Tax Act?

Section 195(2) allows the payer to approach the Assessing Officer to determine the portion of a payment on which TDS should actually be deducted when the full payment is not entirely taxable. In a property sale, for example, only the capital gains are taxable. Section 195(2) lets TDS be calculated on that portion alone, rather than on the total sale price. This prevents the NRI from having excessive tax withheld upfront.

0 Comments