Millions of NRIs across the US, UK, UAE, Canada, and Australia send money back home every single month. For most, it is not just a financial transaction. It is how they take care of their parents from thousands of kilometres away. Living expenses, medical bills, festival gifts, household costs it all adds up, and it all comes from you.

Yet one question keeps coming up. Is this money taxable? And is there a limit on how much you can send?

The short answer is reassuring. But the confusion is real, and it leads to real consequences. Some NRIs hold back from sending large amounts because they fear creating a tax problem. Others send money without any documentation and worry later.

This guide on how to send money to India for parents as an NRI covers everything in one place. The tax rules for both sides. The best transfer methods. Any limits that apply. And what records to keep.

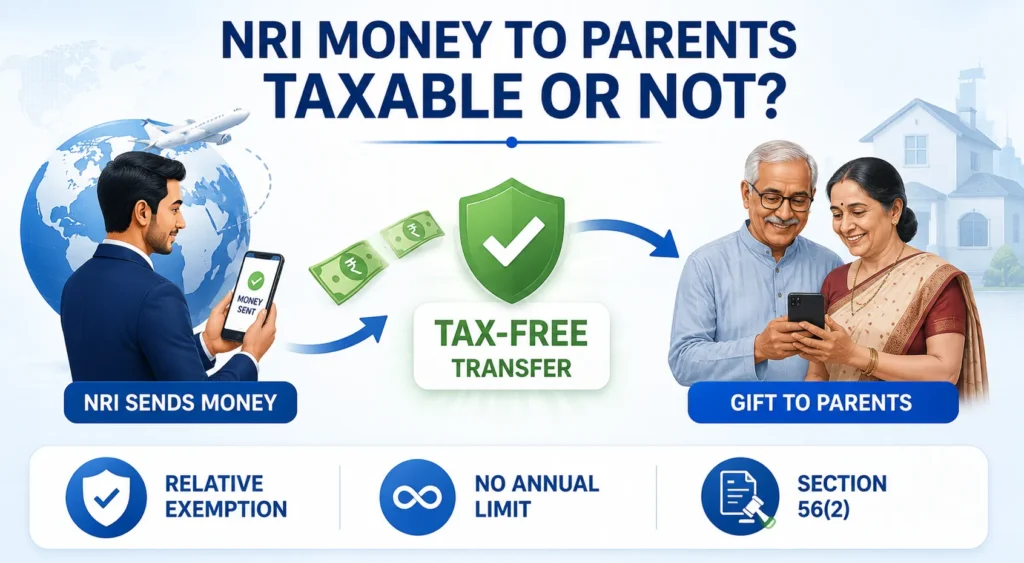

Is Money Sent by an NRI to Parents in India Taxable?

Let us answer this directly.

Money sent by an NRI to their parents in India is not taxable in India neither for the NRI who sends it, nor for the parents who receive it. Under Section 56(2) of the Income Tax Act, gifts received from a relative are fully exempt from income tax. Parents receiving money from their child, NRI or resident, fall squarely within that exemption.

Here is how it breaks down on each side.

For the NRI sender: When you remit money to India from abroad, you are transferring funds from your foreign income. The act of sending that money to India does not create any Indian tax liability for you. You may have tax obligations in your country of residence on income before it is remitted. But the transfer itself? No Indian tax applies.

For the Indian parent recipient: The definition of "relative" under Section 56(2) explicitly includes parents and children. So when your mother or father receives money from you, it qualifies as a gift from a relative. It does not matter whether you are a resident Indian or an NRI. The exemption applies either way.

And here is the most important part. There is no upper limit. No annual cap. No ceiling. Whether you send ₹5 lakh or ₹50 lakh, the exemption covers the full amount.

Hold on to that before reading anything else.

Gift Tax Rules: Why Parents Do Not Pay Tax on Money Received From Their NRI Child

Section 56(2) does the heavy lifting here. It lists specific categories of gifts that are exempt from income tax in India. Gifts received from relatives fall squarely in that exempt category.

The Income Tax Act defines "relative" to include lineal ascendants and descendants. That means parents receiving money from their child, NRI or not, are fully covered. The exemption is not capped. There is no threshold beyond which the gift becomes taxable.

So if you send ₹5 lakh, ₹50 lakh, or even ₹1 crore to your parents, none of it is taxable in their hands. They do not need to declare it as income in their ITR. It simply does not count as income at all.

Here is a practical example. Say you send ₹20 lakh to your mother. She puts it in a fixed deposit earning ₹1.2 lakh interest per year. The ₹20 lakh is completely tax-free. But the ₹1.2 lakh FD interest is taxable in her hands at her applicable slab rate.

That distinction matters. The gift is exempt. The income earned on the gift is not.

One more thing worth noting. Clubbing provisions do not apply for gifts to parents. The returns on the gifted money are taxed in the parents' hands, not the NRI's. This is actually favourable, especially if your parents have low or zero taxable income.

Have Questions About NRI Remittances and Tax? Talk to an NRI Tax Expert at MostlyNRI

Is There a Limit on How Much an NRI Can Send to Parents in India?

No. There is no limit.

Under the Income Tax Act, there is no annual cap on gifts between relatives. Under FEMA (Foreign Exchange Management Act), genuine inward remittances to India through authorised banking channels for family maintenance, support, or gifts are generally permitted, subject to normal banking documentation and compliance requirements. NRIs can freely send money to their family members in India through approved channels.

One important clarification here. The Liberalised Remittance Scheme (LRS) is often mentioned in this context. But LRS applies to resident Indians sending money abroad, not to NRIs remitting money into India. Do not confuse the two. LRS does not restrict or govern what you send to your parents in India.

From the sending country's side, rules may vary. US citizens, green card holders, and other US tax residents should be aware that US gift tax reporting rules may apply when making large gifts to parents abroad. While actual gift tax is rarely payable due to the substantial lifetime exemption, reporting requirements can still arise. For significant transfers, consult a qualified US tax advisor.

One practical note for very large transfers. Large or unusual inward remittances may prompt routine compliance queries from the receiving bank. This is standard procedure and does not mean there is a tax issue. Just have basic documentation ready stating the purpose, for instance "gift to parents for maintenance and living expenses." It usually resolves quickly.

Banks do not deduct TDS merely because parents receive a genuine gift remittance from their NRI child. However, any income subsequently earned from those funds, such as FD interest, may be subject to applicable TDS provisions.

Best Ways to Send Money to India for Your Parents: Methods Compared

Now that the tax question is settled, the practical question is: what is the best way to actually send the money?

The answer depends on how much you are sending, how often, and how quickly it needs to arrive.

| Method | Speed | Cost | Best For |

|---|---|---|---|

| Bank Wire Transfer (SWIFT) | 2-5 business days | Moderate fees + exchange rate margin | Large one-time transfers |

| Online Remittance Services (Wise, Remitly, Western Union) | 1-2 days | Lower fees, better exchange rates | Regular monthly transfers |

| NRI Bank Products (SBI Express Remit, HDFC QuickRemit, ICICI Money2India) | 1-2 days | Competitive rates | Existing NRI banking customers |

| PayPal / Digital Wallets | Fast | High fees | Small amounts only |

| Foreign Currency Demand Draft | Slow | Low relevance today | Largely obsolete |

For regular monthly support, online remittance services or bank-specific NRI products are typically the best combination of cost, speed, and convenience. Wise, for instance, often offers rates very close to the mid-market rate with a flat fee.

For large one-time transfers, compare exchange rates carefully before confirming. Even a 0.5% difference on ₹50 lakh works out to ₹25,000. That is real money. Take ten minutes to compare rates across two or three services before hitting send.

Which Account Should the Money Go Into: Account Options for Parents

This is simpler than most people expect.

Your parents, as resident Indians, have regular Indian savings accounts. That is all they need. Money received as a gift from an NRI child goes directly into their savings account. No special procedure is required.

NRO and NRE accounts are for NRIs, not for resident Indians. Your parents do not need to open any special account to receive international transfers. Their existing savings account at any Indian bank is sufficient.

Once the money is in their account, they are free to use or invest it as they choose. FDs, mutual funds, recurring deposits, or simply keeping it as savings. The choice is theirs.

If the transfer is for a specific purpose, like funding a medical procedure or contributing to a property purchase, keep a brief note documenting that separately. This becomes useful later if the source of funds is ever questioned.

For very large amounts, your parents may want to give their bank a heads-up in advance. It is not a legal requirement. But large inward international transfers sometimes prompt routine queries from the bank's compliance team. A simple explanation closes it quickly.

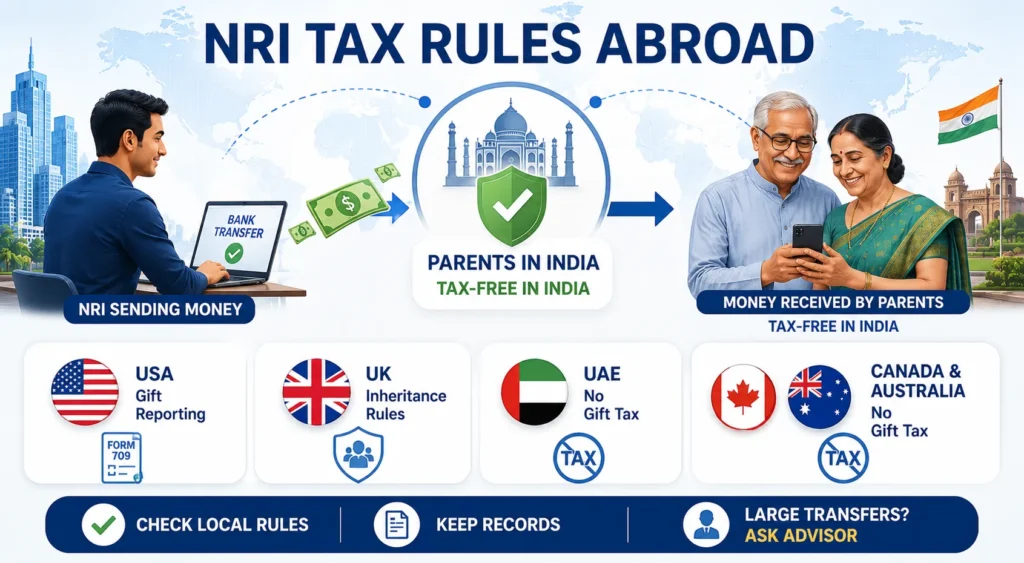

Tax Rules in the NRI’s Country of Residence: What to Check

This is the section most Indian-focused content skips entirely. But it matters.

Sending money to your parents in India does not create any tax liability in India for you as the NRI. We have established that. But what about the tax rules in the country where you live and earn?

- United States: The IRS allows an annual gift tax exclusion of USD 19,000 per recipient (2025 and 2026). Gifts above this amount may need to be reported on Form 709, the US Gift Tax Return. Actual gift tax is rarely owed due to the substantial lifetime exemption. For regular monthly support amounts, this is generally not a concern. For a large one-time transfer above USD 19,000, consult a US tax advisor.

- United Kingdom: There is no gift tax in the UK. However, large gifts can have Inheritance Tax implications if the donor passes away within seven years of making the gift. For regular support transfers, this is typically not a concern.

- UAE, Canada, Australia: These countries generally do not impose gift tax on amounts sent to family members abroad. Transfer freely, though large one-time amounts should still be documented for your own records.

For regular monthly support to parents, the foreign tax angle is rarely an issue. For large one-time transfers, consult a tax advisor in your country of residence. Rules vary, and getting it right upfront saves complications later.

Documentation NRIs Should Maintain for Remittances to Parents

You do not need a notarised gift deed for transfers to parents. Cash gifts between relatives do not require formal documentation under Indian law. But a basic paper trail is always smart. Here is what to keep:

- Transfer records: Save all transfer receipts, SWIFT confirmations, or transaction records from your remittance service. These prove the amount and date of each transfer.

- Purpose note: For large transfers, a brief written statement, even a simple email to yourself, saying "Gift to parents for maintenance and living expenses" is sufficient. No formal format is required.

- Bank statements for parents: Your parents should retain bank statements showing the receipt of funds. These are useful if the bank or tax authorities ever request clarification.

- Source of funds documentation: If the money is later used to buy property or make investments in the parents' names, the source of funds trail becomes important. Keep it organised from the start.

- For US-based NRIs: If your total gifts to one recipient exceed USD 17,000 in a calendar year, maintain documentation in case Form 709 filing is required.

A simple folder, physical or digital, with these records goes a long way. Most transfers to parents are never questioned. But if they are, documentation means the matter closes in a conversation rather than a prolonged process.

What Happens to the Money After: Tax on Returns Earned by Parents

This is the one area where many NRIs and their parents get confused. The gifted money is tax-free. But what happens when that money starts generating income?

The gifted amount remains exempt. Always. But any income earned on that amount is taxable in the parents' hands.

- FD Interest: If your parents put the gifted money in a fixed deposit, the interest earned is taxable at their applicable slab rate. The bank will deduct TDS if interest exceeds ₹40,000 per year (₹50,000 for senior citizens).

- Tax impact for parents: If your parents have relatively low taxable income, the tax payable on returns earned from the gifted funds may be limited or even nil depending on their overall income, deductions, and the tax regime chosen.

- ITR filing: Your parents should file an ITR if their total income, including interest earned on gifted funds, exceeds the basic exemption limit applicable to them.

- No deduction for the NRI: You cannot claim any deduction or credit in India for money sent to your parents. It is a gift, not a deductible expense under Indian tax law.

The practical takeaway: plan for your parents' tax position proactively. If they are investing the gifted funds, factor in the returns and whether they will need to file an ITR or pay advance tax.

Conclusion

Sending money to your parents in India as an NRI is one of the simplest and most tax-efficient ways to support your family. Under Indian tax laws, gifts from children to parents are fully exempt from tax, with no upper limit on the amount that can be transferred. As long as the remittance is made through authorised banking channels and basic records are maintained, both the sender and recipient can remain compliant and worry-free.

The key distinction to remember is that while the gifted amount itself is tax-free, any income earned from it such as fixed deposit interest or investment returns is taxable in your parents' hands. By choosing the right remittance method, understanding the rules in your country of residence, and keeping a clear documentation trail, you can ensure smooth, secure, and hassle-free financial support for your loved ones in India.

Have Questions About NRI Remittances and Tax? Talk to an NRI Tax Expert at MostlyNRI

Disclaimer: This article is for informational purposes only and reflects tax rules applicable for FY 2025-26 and AY 2026-27. Tax laws may change, and individual circumstances vary. This content does not constitute professional tax or legal advice. For large or complex transfers, consult a qualified NRI tax advisor. MostlyNRI is not liable for decisions made solely on the basis of this content.

Frequently Asked Questions

Can NRI send money to parents in India?

Yes, absolutely. NRIs can send any amount of money to their parents in India. There is no restriction under the Income Tax Act or FEMA on remittances to close relatives. The money is not taxable in India for either the NRI sender or the parents who receive it.

Can I send money to my parents in India without tax?

Yes. Money sent by an NRI to their parents qualifies as a gift from a relative under Section 56(2) of the Income Tax Act. Such gifts are fully exempt from income tax in India, with no upper limit on the amount.

What is the maximum amount an NRI can send to family in India per year?

There is no maximum. Indian law does not cap how much an NRI can send to parents or close family. The Income Tax Act exempts gifts between relatives regardless of amount, and FEMA does not restrict inward remittances. Very large transfers may prompt a routine bank compliance check, which is resolved easily with basic documentation.

Can I gift ₹50 lakhs to my mother as an NRI?

Yes. A gift of ₹50 lakh from an NRI child to their mother is completely tax-free in India. Under Section 56(2) of the Income Tax Act, gifts received from a relative, which includes a child, are exempt from income tax regardless of amount. Your mother does not need to declare this as income in her ITR.

How much money can you send to India tax-free?

There is no tax-free limit as such, because the entire amount sent by an NRI to their parents is tax-free in India. The gift exemption under Section 56(2) for relatives is not capped. No TDS is deducted on such transfers, and no income tax is payable by the parents on receipt.

If NRI sends money to India, is it taxable?

No. From an Indian tax perspective, money sent by an NRI to their parents is not taxable. The NRI does not generate Indian taxable income by remitting funds. The parents receive it as an exempt gift from a relative. Tax only arises if the parents invest the money and earn returns, which are taxable in their hands.

Can an NRI send money to India without tax from the USA?

Yes, from an Indian tax perspective there is no tax on the transfer. However, US citizens, green card holders, and other US tax residents should be aware of the IRS annual gift tax exclusion of USD 19,000 per recipient. Gifts above this amount may require filing Form 709 in the US, though actual gift tax is rarely owed because of the lifetime exemption available under US tax law.

Is there any limit on money transfer to India from abroad?

Generally, no. NRIs can remit funds to India for family maintenance, gifts, investments, and other permitted purposes through authorised banking channels. The Liberalised Remittance Scheme (LRS) applies to resident Indians sending money abroad, not to NRIs sending money into India. These are separate regulatory frameworks and should not be confused.

0 Comments