You get a TDS deduction on your NRO interest. Out of nowhere. No warning.

Or you receive a tax notice on rental income from your Delhi flat. And you are sitting in Toronto or Dubai thinking: what exactly is India allowed to tax me on?

It is a fair question. It is also a confusing one. Because the rules are not obvious. And most people find out only after the deduction has already happened.

Here is the short answer. India taxes NRIs only on income that accrues, arises, or is received in India. Not on global income. But within that boundary, different income types are treated very differently. NRO interest gets taxed at a flat 30%. NRE interest? Completely exempt. Same bank. Two accounts. Completely opposite tax treatment.

This guide breaks down every category of NRI income what is taxable, what is not, the applicable rates, and what you can actually do about it. All in one place. Read it once. Bookmark it. Come back whenever you need it.

The Core Rule How India Decides What to Tax NRIs On

Let us get this out of the way first.

NRIs are taxed in India only on income that accrues, arises, or is received in India. That is the foundational rule. Everything else flows from this.

Under the Income Tax Act, your income is taxable in India if it:

- Accrues or arises in India

- Is deemed to accrue or arise in India

- Is received in India

That is the complete list. Nothing outside these three buckets touches you as an NRI.

So your salary from a US company? Not taxable in India. Rental income from your Dubai apartment? Not India's concern. Capital gains from selling US stocks? India has no claim on it.

Think of it like a boundary drawn around India's borders. Only the income that originates inside that boundary is India's to tax.

Now compare this to a Resident and Ordinarily Resident (ROR) taxpayer. They get taxed on global income. Every rupee earned anywhere in the world. That is a much wider net. As an NRI, you are not in that net.

Your residential status is determined under Section 6 of the Income Tax Act. It is based on the number of days you spend in India in a financial year. Not your citizenship. Not which passport you hold. Just days.

NRI Tax Slab Rates for FY 2025-26 What Rates Apply

Before we get into specific income types, you need to understand the rates that apply to you.

These are the slab rates for NRIs for AY 2026-27.

New Tax Regime (Default)

| Income Range | Tax Rate |

|---|---|

| Up to ₹3,00,000 | Nil |

| ₹3,00,001 to ₹7,00,000 | 5% |

| ₹7,00,001 to ₹10,00,000 | 10% |

| ₹10,00,001 to ₹12,00,000 | 15% |

| ₹12,00,001 to ₹15,00,000 | 20% |

| Above ₹15,00,000 | 30% |

Old Tax Regime

| Income Range | Tax Rate |

|---|---|

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 to ₹5,00,000 | 5% |

| ₹5,00,001 to ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

On top of slab tax, there is more.

Surcharge applies at 10% if your income crosses ₹50 lakh. It goes to 15% above ₹1 crore. And 25% above ₹2 crore.

Health and Education Cess is 4% on your tax plus surcharge. Always. No exceptions.

And now the part that trips up a lot of NRIs at filing time.

NRIs cannot claim the Section 87A rebate. Under the new regime, a resident with income up to ₹7 lakh effectively pays zero tax because of this rebate. NRIs do not get it. Even if your total Indian income is ₹4 lakh. Even if it is ₹2.5 lakh. The rebate simply does not apply to you.

Many NRIs assume they owe nothing because their Indian income is below ₹7 lakh. They skip filing. Then they get a notice. So flag this clearly before you file.

Complete Breakdown Which Income Is Taxable for NRIs and Which Is Not

This is the section to save. This is your master reference.

| Income Type | Taxable for NRI? | Rate | Notes |

|---|---|---|---|

| NRO account interest | Yes | Taxed as per applicable income tax provisions | Banks generally deduct TDS at 30% plus applicable surcharge and cess. Excess TDS can be claimed as refund through ITR filing |

| NRE account interest | No | Exempt | Fully tax-free under Section 10(4) |

| FCNR deposit interest | No | Exempt | Generally exempt during NRI and eligible RNOR status, subject to applicable conditions |

| Rental income from Indian property | Yes | Taxable after eligible deductions | Tenant is generally required to deduct TDS under Section 195 at applicable rates |

| Capital gains from Indian property | Yes | Applicable capital gains tax rates | Buyer must deduct TDS under Section 195 at applicable rates |

| Capital gains from Indian shares / equity MFs | Yes | 12.5% LTCG above ₹1.25L / 20% STCG | STT must be applicable |

| Dividends from Indian companies | Yes | Taxable in India | Withholding tax may apply and DTAA relief may be available |

| Salary for services rendered in India | Yes | Slab rates | Taxable even if salary received abroad |

| Foreign salary | No | Exempt | Earned and received outside India |

| Pension from Indian employer | Yes | Slab rates | Accrues in India |

| Gifts from non-relatives above ₹50,000 | Yes | Slab rates | Received in India |

The core insight from this table is simple. The source and location of income determines taxability. Not where you live. Not which country issued your visa.

NRE interest is exempt because the account holds foreign earnings brought into India. NRO interest is taxable because it represents Indian-origin money. Same bank branch, possibly even the same relationship manager. But completely different tax treatment.

Not sure what your Indian income actually adds up to? Get a personalised NRI tax assessment from MostlyNRI and know exactly where you stand before you file.

NRO Interest Income The Most Common Taxable Income for NRIs

If you have an NRO savings account or a fixed deposit in India, you are already generating taxable income. Every month. Quietly. Whether you check your account or not.

A lot of NRIs I speak to are genuinely surprised when they see TDS deducted on their NRO interest. They assumed the bank would handle it in some neutral way. It does handle it. By taking 30% off the top.

Here is how it works in practice.

Interest earned on NRO savings accounts, fixed deposits, and recurring deposits is taxable in India. Banks generally deduct TDS at 30% plus applicable surcharge and cess before crediting the interest to your account. However, the final tax liability is determined based on your overall taxable income and applicable income tax provisions, and excess TDS can be claimed as a refund through ITR filing.

The bank does not consider your basic exemption limit while deducting TDS. TDS is generally deducted at the prescribed rate regardless of your total Indian income. However, while filing your ITR, you may be able to claim the applicable basic exemption limit and seek a refund if excess tax has been deducted.

But there is a way to bring this rate down. India has Double Taxation Avoidance Agreements (DTAAs) with many countries. Think of a DTAA as a treaty between two countries that says: "We will not both tax the same person on the same income." Under the India-US DTAA, for example, NRO interest is capped at 15% instead of 30%.

To claim this benefit, you need to submit a Tax Residency Certificate (TRC) from your country of residence and Form 10F to your bank. Once you do this, the bank deducts TDS at the treaty rate going forward.

If TDS has already been deducted at 30% and your DTAA entitles you to 15%, file your ITR and claim the refund of the excess. You will get it back.

See our detailed guide on Form 10F for step-by-step instructions on how to apply for DTAA relief.

Rental Income From Indian Property How NRIs Are Taxed

Own a flat in Bengaluru or Noida that you have rented out? That rental income is taxable in India. No way around it.

But here is the thing. The actual tax you end up paying is usually much lower than people expect. Because deductions are generous.

You start with the gross annual rent. Deduct municipal taxes paid. That gives you the net annual value. Then a standard deduction of 30% is applied automatically. No receipts. No proof. Just 30% off, by default.

If you have a home loan on that property, the interest you pay is also deductible under Section 24(b). For a let-out property under the old regime, there is no upper cap on this deduction. So if you are paying ₹4 lakh annually in home loan interest, that comes off too.

Let us put some numbers to it. Say your Delhi flat earns ₹7.2 lakh in annual rent. Municipal taxes are ₹30,000. Net annual value: ₹6.9 lakh. After 30% standard deduction: ₹4.83 lakh. If you also have ₹2 lakh in home loan interest: taxable income drops to ₹2.83 lakh. That is a very different number from ₹7.2 lakh.

Now, the part many tenants and NRI landlords both get wrong.

The tenant is legally required to deduct TDS under Section 195 before paying rent to an NRI landlord. Not optional. Not a courtesy. It is a legal obligation. The applicable TDS rate depends on the provisions in force and the facts of the case. If the tenant skips this obligation, the NRI landlord may still owe tax, and the tenant can face consequences for non-compliance.

Since TDS is deducted on the full gross rent before any deductions, the actual tax after filing ITR and claiming deductions is almost always lower than what was deducted. File your ITR, declare your deductions, and claim the refund.

If you are selling rather than renting the property, see our guide on TDS on NRI property sale.

Capital Gains Tax for NRIs Shares, Mutual Funds, and Property

Capital gains is where it gets layered. The rate depends on what you sold and how long you held it. Think of it as two separate conversations: one for financial assets, one for property.

Indian Shares and Equity Mutual Funds

Long-term capital gains (held over 1 year): 12.5% on gains above ₹1.25 lakh. Below that threshold, it is exempt. Securities Transaction Tax (STT) must have been paid at the time of sale.

Short-term capital gains (held under 1 year): 20%.

One practical note for NRI investors in mutual funds. When you redeem units, the AMC deducts TDS before crediting the proceeds to your account. So if you are counting on a specific post-redemption amount to pay for something, plan for the TDS cut. The numbers you see in your statement are pre-tax.

Indian Property

Long-term capital gains (held over 2 years): The applicable tax treatment depends on the nature of the asset, date of acquisition, and provisions applicable to the transaction. Property taxation rules have undergone significant changes in recent years, and the correct method of computation should be evaluated based on the specific facts of the sale.

Short-term capital gains (held under 2 years): Taxed at slab rates. No special rate here.

The buyer deducts TDS. If you are an NRI selling property in India, the buyer must deduct TDS under Section 195 before making payment. The applicable rate depends on factors such as the nature of the gain, applicable surcharge and cess, and whether a lower deduction certificate has been obtained. This happens before you receive the sale proceeds. It is the buyer's legal obligation, and they face consequences for non-compliance.

You do not have to take the full tax hit if you reinvest. The Income Tax Act offers exemptions that let you defer or eliminate capital gains tax entirely:

- Section 54: Reinvest gains from a residential property sale into another residential property

- Section 54EC: Invest gains in specified bonds (NHAI, REC) within 6 months of sale

- Section 54F: For gains from non-residential assets reinvested into residential property

See our guides on TDS on NRI property sale and 8 Smart Ways to Reduce NRI Tax for more details.

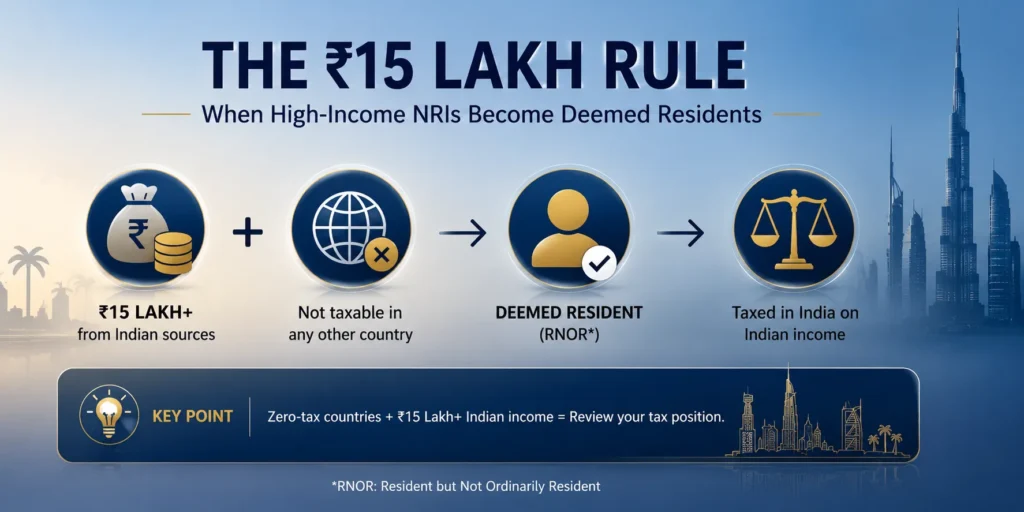

The Rs. 15 Lakh Rule When High-Income NRIs Become Deemed Residents

This one surprises a lot of people. Especially NRIs living in the UAE, Qatar, or Bahrain.

Under the Finance Act 2020, if an Indian citizen:

- Earns Rs. 15 lakh or more from Indian sources in a financial year, and

- Is not taxable in any other country or territory

...they are treated as a deemed resident of India for that year.

This rule was designed to close a specific loophole. Some NRIs had structured their affairs very carefully. They left India. They moved to a zero-tax country. They kept earning significant income from Indian sources. And they paid tax nowhere. Not India. Not their new country. Nowhere.

The Rs. 15 lakh rule puts an end to that. India says: if you are an Indian citizen, earning substantial Indian income, and paying tax to no one anywhere in the world, you may be treated as a deemed resident under the Income Tax Act. Such individuals are generally classified as Resident but Not Ordinarily Resident (RNOR), subject to the applicable conditions.

Importantly, deemed residency does not automatically make a person a fully taxable resident of India. The scope of taxation depends on the residential status determined under the Act and the applicable provisions governing RNOR taxpayers.

The practical concern: NRIs in the UAE, Bahrain, or Qatar with Rs. 15 lakh or more in Indian income should review their tax position carefully. These are zero-tax jurisdictions. If your Indian income has crossed that threshold, get professional advice before your next ITR filing.

How to Reduce Tax on NRI Income Practical Options

Being taxed on Indian income does not mean you have no options. There are several legitimate, Income Tax Act-backed ways to reduce what you actually pay.

DTAA Relief: Submit a Tax Residency Certificate and Form 10F to your bank or the payer. This lets them deduct TDS at the treaty rate instead of the default 30%. Works well for NRO interest and dividends. A US-based NRI can bring the TDS rate on NRO interest down from 30% to 15% this way.

Lower TDS Certificate under Section 197: Apply to the Income Tax department before the income is received. If the department approves it, they issue a certificate telling the payer to deduct TDS at a lower, customised rate based on your actual expected liability. Particularly useful for rental income situations where deductions will significantly reduce your final tax.

Move savings to NRE accounts: NRE interest is fully exempt under Section 10(4). If you have money sitting in NRO accounts generating 30% TDS every quarter, restructuring where your savings sit can eliminate that drain entirely. Not everything can be moved to NRE, but where it can, the tax difference is significant.

Claim deductions in ITR: Under the old tax regime, deductions under Section 80C (up to Rs. 1.5 lakh for investments like ELSS, PPF, life insurance) and Section 80D (health insurance premiums) can reduce your taxable Indian income. These are not available under the new regime.

Use capital gains reinvestment exemptions: Sections 54, 54EC, and 54F let you roll gains into new assets and defer or eliminate the tax. If you are selling Indian property, explore these before the sale, not after.

File your ITR and claim refunds: This is the most underused option. If TDS deducted during the year is more than your actual tax liability, file your ITR. You get the excess back. Many NRIs do not file because they think their income is below the threshold or that TDS has already settled everything. It has not. Unrefunded TDS is just money left on the table.

See our guides on Form 10F and 8 Smart Ways to Reduce NRI Tax.

Conclusion

Navigating NRI taxation does not have to be complicated once you understand the basic principle: India taxes only income that is earned, received, or deemed to arise in India. However, each income source—whether NRO interest, rental income, dividends, pension, or capital gains—comes with its own tax rules, TDS requirements, and potential exemptions.

By understanding which income is taxable, leveraging DTAA benefits, claiming eligible deductions and exemptions, and filing your ITR correctly, you can significantly reduce your tax burden and avoid unnecessary compliance issues. A proactive approach to tax planning not only helps you stay compliant but also ensures that you keep more of your hard-earned money while managing your finances efficiently across borders.

See our complete guide on Form 10F for step-by-step instructions.

Not Sure What You Owe? Get a Personalised NRI Tax Assessment. Talk to MostlyNRI.

Disclaimer: This article is for informational purposes only. Tax rates, rules, and provisions are subject to change based on Finance Act amendments and CBDT notifications. Individual tax situations vary significantly based on residential status, income type, country of residence, and applicable DTAA provisions. Please consult a qualified NRI tax advisor before making any financial or tax-related decisions.

Frequently Asked Questions

How much income is tax-free for NRIs in India?

Under the new tax regime, the basic exemption limit is Rs. 3 lakh. Under the old regime, it is Rs. 2.5 lakh. However, tax liability, return filing obligations, TDS deductions, and the nature of income should all be evaluated separately. NRIs also cannot claim the Section 87A rebate available to resident taxpayers. But remember, NRIs cannot claim the Section 87A rebate. So there is no zero-tax benefit up to Rs. 7 lakh the way residents get. NRE account interest and FCNR deposit interest are fully exempt regardless of the amount. They do not count toward taxable income at all.

Which income is taxable in India for NRIs?

NRO account interest, rental income from Indian property, capital gains from Indian shares, mutual funds and property, dividends from Indian companies, salary for work performed in India, and pension from Indian employers. NRE interest, FCNR interest, and income earned and received entirely outside India are all exempt.

What income do non-residents pay tax on?

Non-residents pay tax on income that accrues, arises, or is received in India. This includes Indian-source interest, rent from Indian property, capital gains from Indian assets, and salary for services performed on Indian soil. Foreign-source income is not taxable in India for non-residents.

What is the 15 lakh income rule for NRIs?

Under the Finance Act 2020, an Indian citizen with Rs. 15 lakh or more in Indian income who is not taxable in any other country is treated as a deemed resident of India for that year. The rule targets NRIs in zero-tax jurisdictions who had structured themselves to pay tax nowhere. NRIs who pay tax in their country of residence are not affected by this provision.

What is the new rule for NRI in India in 2025?

The most significant recent change is the capital gains tax revision post-Budget 2024. Long-term capital gains on property can now be computed at 12.5% without indexation or 20% with indexation. Which is better depends on your specific transaction. The Rs. 15 lakh deemed residency provision from Finance Act 2020 also continues to apply. For FY 2025-26, the new tax regime is the default for NRIs as well.

What is the 90% rule for non-residents?

This is not a standard provision under Indian income tax law. You may be thinking of the 182-day residency test, which determines NRI status based on days spent in India. If you came across the "90% rule" in a specific context, do not rely on it without verifying the source. Speak to a qualified NRI tax advisor for clarity.

What is the 4 year rule for NRI?

This likely refers to the RNOR (Resident but Not Ordinarily Resident) window that returning NRIs can qualify for. When an NRI returns to India permanently, they may get RNOR status for up to 2 to 3 years, during which foreign income remains exempt from Indian tax. The conditions depend on total years spent as NRI before returning. If you are returning to India, see our RNOR blog series. RNOR rules are different from NRI rules and should not be treated the same way.

What are the disadvantages of an NRO account?

Three main ones. First, 30% TDS on all interest is deducted automatically, with no basic exemption benefit regardless of how low your total income is. Second, limited repatriation of funds is allowed, up to USD 1 million per financial year, and it requires CA certification and documentation. Third, no Section 87A rebate applies to NRO income, so the zero-tax benefit that residents get up to Rs. 7 lakh simply does not exist for NRIs with NRO income. Restructuring savings from NRO to NRE where eligible is a common and effective response to all three of these issues.

How to reduce TDS as an NRI legally?

Three legitimate routes. First, submit a Tax Residency Certificate and Form 10F to claim DTAA benefit. This brings TDS on NRO interest down to the treaty rate, such as 15% under the India-US DTAA instead of the default 30%. Second, apply for a lower TDS certificate under Section 197 before income is received. The tax department issues a certificate directing the payer to deduct at your actual tax rate. Third, file your ITR and claim a refund of excess TDS already deducted. All three are completely legal and backed by the Income Tax Act.

0 Comments