Here is something most Indians living abroad get wrong.

They assume that because they live outside India, work abroad, or hold a foreign visa, they are automatically Non-Resident Indians for tax purposes. Simple as that.

It is not that simple.

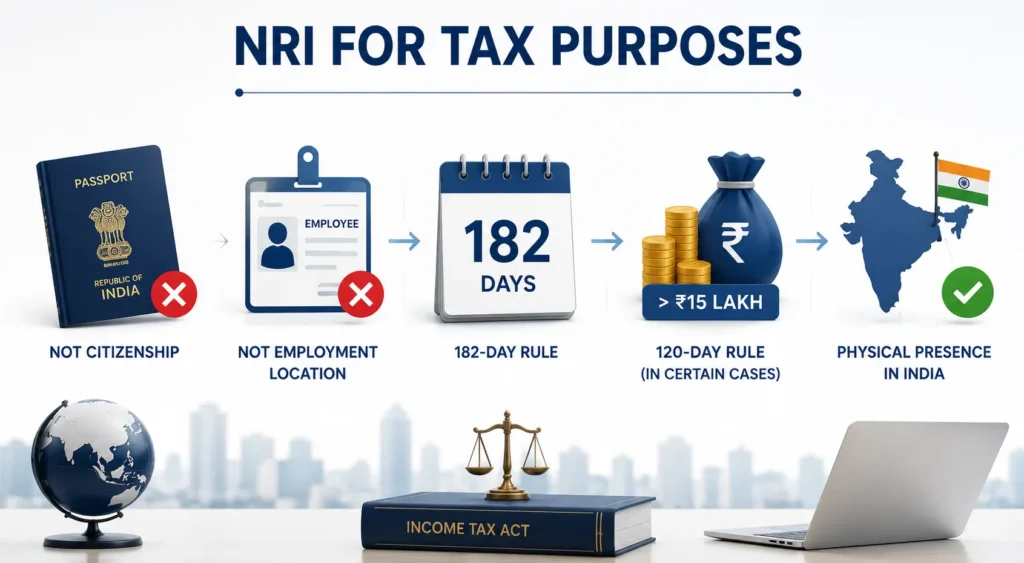

In India, NRI status for income tax has nothing to do with your visa. Nothing to do with your passport. Nothing to do with where your employer is located. It comes down to one thing only: how many days you physically spent in India during a financial year.

Get that day count wrong and you could end up being taxed as a full resident on your global income without even realising it.

This guide covers exactly who qualifies as an NRI under Indian tax law, how to count the days correctly, the key exceptions introduced in recent years, and what happens if you do not declare your status right.

NRI for Tax Purposes: The Legal Definition Under the Income Tax Act

Let us start with the direct answer.

For income tax purposes in India, an individual qualifies as a non-resident if they do not satisfy any of the conditions for being treated as a resident under Section 6 of the Income Tax Act. In practice, the most common test is the 182-day rule. However, additional conditions, including the 120-day rule for certain individuals with Indian income exceeding Rs. 15 lakh, may also apply. Residential status is determined primarily by physical presence in India. Not citizenship. Not passport type. Not employment location.

This definition comes from Section 6 of the Income Tax Act, 1961. Under Section 6, a person is a resident of India if they meet certain day-count conditions. If they do not meet those conditions, they are a non-resident. It is almost a process of elimination.

One important distinction to understand early: NRI status under tax law is not the same as NRI status under FEMA (Foreign Exchange Management Act). FEMA uses a different test based on intent and purpose of stay. The two can and do give different results for the same person. This guide focuses entirely on the Income Tax Act definition.

The Day Count Rules: All Three Thresholds Explained

This is where most people stop at the 182-day rule and miss the full picture. There are actually three rules. Each applies in different situations.

| Rule | Threshold | When It Applies |

|---|---|---|

| Standard 182-Day Rule | Less than 182 days in India = NRI | Applies to most Indians living abroad |

| 120-Day Rule (Finance Act 2020) | Less than 120 days in India = NRI | Applies only if Indian income exceeds Rs. 15 lakh |

| 60-Day Rule with 4-year look-back | Less than 60 days in India = NRI | Applies to certain residents; most NRIs employed abroad are exempt |

Rule 1: The Standard 182-Day Rule

This is the baseline. If you spend 182 days or more in India in a financial year (April 1 to March 31), you are a resident for that year. Fewer than 182 days, and you are an NRI. This applies to the vast majority of Indians working or settled abroad.

Rule 2: The 120-Day Rule

Introduced by the Finance Act 2020, this rule targets certain high-income Indian citizens and Persons of Indian Origin who make extended visits to India. If your income from Indian sources exceeds Rs. 15 lakh during the financial year, and you stay in India for 120 days or more during that year while also having spent 365 days or more in India during the preceding four financial years, you may be treated as a resident.

Think of it this way. If you earn significant income from India and spend substantial time in the country over multiple years, the residential status rules become stricter than the standard 182-day test.

Rule 3: The 60-Day Rule with 365-Day Look-Back

This one is more complex. For certain individuals, if they spend 60 or more days in India in the current financial year and 365 or more days in India over the previous four financial years combined, they become resident.

However, there is an important exemption. An Indian citizen who leaves India for employment abroad, or as a crew member of an Indian ship, is exempt from the 60-day rule. For them, only the 182-day threshold applies. Most NRIs living abroad for jobs fall into this exempt category. But it is worth verifying your specific situation.

How to Calculate the 182 Days: What Counts and What Does Not

Knowing the rule is one thing. Calculating it correctly is another.

The financial year runs from April 1 to March 31. You count only the days spent in India within this window. Not the calendar year. Not any 12-month rolling period.

A few important counting rules:

- Generally, any part of a day spent in India is counted as a day of stay in India. As a result, arrival and departure dates are typically included when calculating the total number of days spent in India during a financial year.

- All trips are added together. Three visits of 30 days each equals 90 days total for the year.

- Short visits, holidays, and family trips all count. There is no exemption for the reason you were in India.

- Transit days do not count, provided you do not clear immigration. If you pass through an Indian airport without entering the country officially, those hours are not counted.

A worked example:

Priya works in Dubai. In FY 2025-26, she visits India three times: 25 days in May, 18 days in October, and 30 days in January. Total days in India: 73. She qualifies as an NRI for FY 2025-26. Clear.

Now consider Rahul. He was in India for a family emergency. He spent 55 days in April-May, took a short trip back in August for 40 days, and returned again in February for 90 days. Total: 185 days. Rahul is a resident for FY 2025-26, even if he has been living abroad for years. Past NRI status does not protect you for the current year.

Not sure how your days add up for FY 2025-26? Get a personalised NRI residential status assessment from MostlyNRI.

The Deemed Residency Rule: When High-Income NRIs Become Taxable in India

This is one of the most misunderstood provisions introduced in recent years. And it catches people off guard.

Under the Finance Act 2020, an Indian citizen who earns Rs. 15 lakh or more from Indian sources and is not liable to pay tax in any other country is deemed to be a resident of India for tax purposes. Even if they spent zero days in India.

The key phrase is "not liable to pay tax in any other country." This targets individuals who have moved to zero-tax jurisdictions specifically to avoid paying tax anywhere.

If you pay income tax in the US, UK, Singapore, or most other countries, this rule does not apply to you. You are liable to tax there, so you are not caught by the deemed residency provision.

The UAE is where this gets nuanced. The UAE has no personal income tax. So if you are based in the UAE, earn Rs. 15 lakh or more from Indian sources, and are not taxed anywhere else, you could be treated as a deemed resident of India.

One important clarification: deemed residents are generally treated as Resident but Not Ordinarily Resident (RNOR). They are not taxed on global income in the same manner as Resident and Ordinarily Resident individuals. However, certain foreign income connected with a business controlled from India or a profession set up in India may still be taxable. They also lose the NRI classification and some of the benefits that come with it.

If you are a UAE-based NRI with significant Indian income, this provision is worth reviewing carefully with a qualified tax advisor.

NRI vs RNOR vs Resident: The Three Tax Statuses and What They Mean

Once residential status is determined, it feeds into a broader classification system. There are three possible tax statuses under Indian law:

- NRI (Non-Resident Indian): Taxed only on income that is earned or received in India. Foreign income is not taxable in India.

- RNOR (Resident but Not Ordinarily Resident): Also taxed only on Indian income in most cases. This is a transitional status typically available to returning NRIs for a few years after they come back to India.

- ROR (Resident and Ordinarily Resident): Taxed on global income. This is the most comprehensive tax liability.

The jump from NRI to ROR is significant. It means income earned in the UAE, the US, the UK, or anywhere else becomes reportable and potentially taxable in India.

The RNOR status acts as a buffer. It gives returning NRIs time to reorganise their finances before full resident taxation kicks in. For a detailed breakdown of how RNOR works and who qualifies, see the RNOR vs NRI vs Resident guide on MostlyNRI.

NRI vs OCI vs PIO: Are They All the Same for Tax Purposes?

These three terms are often used interchangeably. For tax purposes, they are not identical. Here is how they compare:

| Category | Who They Are | Tax Treatment | Residency Determined By |

|---|---|---|---|

| NRI | Indian citizen residing outside India | Taxed on Indian income only (if non-resident) | Day count under Section 6 |

| OCI | Foreign national of Indian origin with OCI card | Same as NRI for tax | Day count under Section 6 |

| PIO | Person of Indian Origin (largely merged into OCI since 2015) | Similar to OCI for tax | Day count under Section 6 |

The most important takeaway: an OCI card does not give you permanent non-resident tax status. OCI holders are subject to the same residential status tests under Section 6 of the Income Tax Act. Depending on the number of days spent in India and other applicable conditions, an OCI holder may be a non-resident, RNOR, or resident. The card is an immigration and travel document. It does not override the residential status rules under the Income Tax Act.

Is It Mandatory to Declare NRI Status? And What Is the Penalty for Not Doing So?

Yes. Residential status must be correctly declared every time you file an ITR (Income Tax Return). It is not a one-time declaration. It must be assessed and reported each financial year.

Filing with the wrong residential status is a misrepresentation of facts. The consequences can be serious.

If a resident incorrectly files as an NRI and this results in under-reporting or misreporting of income, additional tax demands, interest, and penalties may apply. Under Section 270A of the Income Tax Act, penalties in cases of misreporting can be substantial. In serious cases involving wilful tax evasion, prosecution provisions such as Section 276C may also become relevant.

On the FEMA side, NRIs are separately required to inform their banks of their change in residential status. Failure to convert NRE/NRO accounts appropriately or to notify the bank can attract penalties under FEMA. This is a separate compliance requirement from the income tax declaration.

Practical advice: review your residential status every financial year. NRI status is not permanent. It changes based on the actual days you spend in India that year. A long visit due to illness, a family emergency, or remote work from India can change your status without you realising it.

Common Situations Where NRI Status Is Incorrectly Determined

These are the mistakes that come up again and again.

1. Counting days wrong. Not including arrival and departure days. Forgetting a short trip taken in the middle of the year. These small errors can push the total across the threshold.

2. Assuming NRI status continues automatically. Many long-term NRIs return to India for six months or more without tracking their days. If you cross 182 days in any single financial year, you are a resident for that year. Your past years do not matter.

3. Ignoring the 120-day rule. High-income NRIs who earn Rs. 15 lakh or more from Indian sources often do not know their threshold is lower. They spend four months in India thinking they are safe. They are not.

4. Confusing FEMA NRI status with Income Tax NRI status. Someone can be an NRI under FEMA but a resident under the Income Tax Act in the same year. The two definitions work independently. Both matter for different financial decisions.

5. Not reviewing status after extended medical or family visits. A three-month stay to care for a sick parent still counts toward the day total. Intent and circumstances are not relevant to the calculation.

6. Assuming an OCI card means permanent NRI tax status. It does not. Day count rules apply to OCI holders just as they apply to Indian citizens.

Conclusion

Understanding your NRI status is not just a technical tax requirement—it directly affects how your income is taxed in India. While the 182-day rule is the most commonly known test, the additional 120-day rule, 60-day rule, and deemed residency provisions mean that many individuals can unintentionally lose their NRI status. Since residential status is determined afresh every financial year, even a few extra weeks spent in India can significantly change your tax obligations.

The key takeaway is that NRI status depends on actual physical presence in India, not your passport, visa, OCI card, or place of employment. Correctly tracking your days of stay, understanding the applicable residency rules, and reviewing your status annually can help you avoid unexpected tax liabilities, penalties, and compliance issues. When in doubt, especially if you have substantial Indian income or frequently travel between countries, seeking professional tax advice can ensure you remain compliant while making the most of the tax benefits available to NRIs.

Not sure of your residential status for FY 2025-26? A wrong determination can change your entire tax liability. Get a personalised NRI tax assessment from MostlyNRI.

Disclaimer: This article is for informational purposes only. Residential status determination depends on individual facts and circumstances, and tax laws are subject to change. Please consult a qualified NRI tax advisor for a personalised assessment specific to your situation.

Frequently Asked Questions

Who is eligible for NRI tax status in India?

Any Indian citizen or Person of Indian Origin who spends fewer than 182 days in India in a financial year qualifies as an NRI for tax purposes. If their Indian income exceeds Rs. 15 lakh, the threshold is 120 days. Eligibility is assessed each financial year based on actual days spent in India.

Who will not be considered an NRI in India?

Anyone who spends 182 days or more in India in a financial year is a resident, not an NRI. High-income individuals (Rs. 15 lakh+ Indian income) who spend 120 days or more in India are also resident. Deemed residents under the Finance Act 2020 provision are also not NRIs, even if they spent no time in India.

How do I know if I am an NRI for income tax purposes?

Count the total days you physically spent in India between April 1 and March 31. If the total is below 182 days (or below 120 days if your Indian income exceeds Rs. 15 lakh), you are an NRI for that financial year. Also check whether the deemed residency provision applies to your situation.

What is the new rule for NRI status in India?

Two significant rules were introduced via the Finance Act 2020. First, the 120-day rule: Indian citizens or PIOs with Rs. 15 lakh+ Indian income become resident if they stay 120 days or more in India. Second, the deemed residency rule: Indian citizens with Rs. 15 lakh+ Indian income who are not taxed in any other country are deemed residents of India.

What is the 4-year rule for NRI status?

This generally refers to one of the look-back tests used when determining residential status or RNOR eligibility. A returning NRI may qualify as RNOR if they were a non-resident in 9 out of the 10 preceding financial years, or if they spent 729 days or less in India during the preceding 7 financial years. For complete RNOR eligibility conditions, see the dedicated RNOR guide on MostlyNRI.

Is it mandatory to declare NRI status when filing ITR?

Yes. Residential status must be correctly reported in the ITR every year. Filing with an incorrect residential status is a misrepresentation. Penalties under Section 270A can be up to 200% of the tax evaded. It is a compliance requirement, not optional.

What is the 90% rule for non-residents?

There is no specific "90% rule" used to determine NRI status under the Indian Income Tax Act. Residential status is determined using the day-count tests prescribed under Section 6, including the 182-day rule, the 120-day rule in certain cases, and other applicable residency provisions. If you have come across a reference to a "90% rule," it is likely being used in a different tax context and should not be relied upon for determining NRI status.

What are the tax disadvantages of being an NRI?

Several. NRIs are not eligible for the Section 87A tax rebate (available to resident individuals with income up to Rs. 5 lakh). Interest on NRO accounts is subject to a 30% TDS (plus surcharge and cess).They also face mandatory FEMA compliance requirements for bank accounts, investments, and property. Depending on the nature of income and other applicable conditions under the Income Tax Act, NRIs may also have ITR filing obligations in India.

What is the difference between NRI, PIO, and OCI for tax purposes?

All three are assessed for Indian tax residency using the same day count rules under Section 6 of the Income Tax Act. An NRI is an Indian citizen living outside India. An OCI is a foreign national of Indian origin holding an OCI card. PIO (Person of Indian Origin) has largely been merged into the OCI category since 2015. For tax purposes, OCI holders are treated the same as NRIs. The type of document held does not change the residency test.

0 Comments