You've just returned to India after years abroad.

And somewhere between the reunion dinners and the paperwork, a serious financial question is sitting quietly in the background. What do I do with all the money I saved abroad and how do I make sure I don't lose a chunk of it to taxes I didn't plan for?

If you qualify for RNOR Resident but Not Ordinarily Resident status, you have a two to three year window where your foreign income is not taxed in India. That's a meaningful advantage. But only if you use it deliberately.

This guide covers exactly what returning NRIs should do with their money during the RNOR period. You'll find:

- What RNOR actually means for your investments and why the timing matters

- What to do immediately after returning - which accounts to protect, which to convert, and what not to touch

- The best investment options during RNOR - from FCNR deposits and RFC accounts to equity mutual funds and NPS

- What to avoid - the common mistakes that cost returning NRIs lakhs in unnecessary tax

- A worked example showing exactly how one returning NRI structured his RNOR plan across different asset types

- Answers to the most common RNOR questions - including account conversion timelines, foreign asset reporting, and ITR filing

The RNOR window doesn't wait. The NRIs who get the most out of it are the ones who planned it early - not the ones who figured it out after it closed.

Quick Recap Why the RNOR Window Is a Once-in-a-Lifetime Opportunity

Think of RNOR status as a financial bridge.

You've left your life abroad. But the Indian tax system hasn't fully claimed you yet.

During this period, typically 2 to 3 financial years, foreign income that accrues and is received outside India is generally not taxable in India. This can include overseas rental income, FCNR interest, and capital gains from foreign assets, subject to applicable tax rules and exceptions. Once RNOR ends and you become a Resident and Ordinarily Resident (ROR), your global income generally becomes taxable in India. Once RNOR ends and you become a Resident and Ordinarily Resident (ROR), everything changes. Your global income becomes taxable in India, at Indian rates.

That's why this window matters so much.

It's the optimal time to restructure your investments, remit your foreign savings in a planned way, and start building an India-based portfolio in the right order, at the right pace.

(For the full breakdown of what RNOR status means and how it's calculated, refer to our RNOR explanation blog in the MostlyNRI series.)

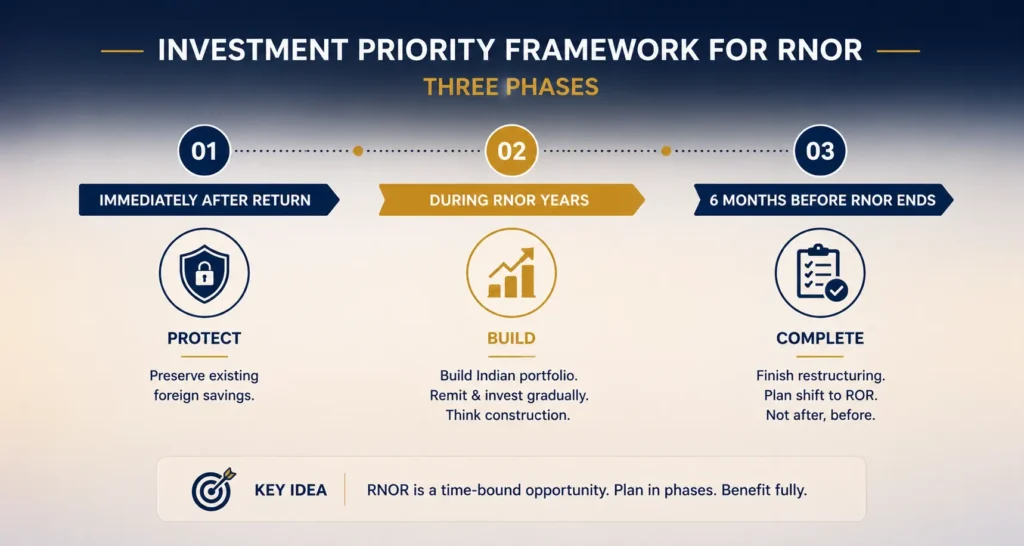

The Investment Priority Framework for RNOR -Three Phases

Before we get into specific products, let's get the strategy right.

Most returning NRIs make the mistake of treating RNOR as just a tax label. It's not. It's a time-bound opportunity with a clear beginning, middle, and end. Your investment decisions should reflect that.

Here's how to think about it:

Phase 1 - Immediately After Return

Protect your existing foreign savings. Don't rush to convert. Don't move money impulsively into Indian accounts. Your job in this phase is to preserve the tax-free structures you already have.

Phase 2 - During the RNOR Years

Gradually build your Indian investment portfolio. Use the tax-free window to remit foreign savings in a structured, deliberate way. Start RFC accounts. Continue FCNR deposits. Begin SIPs. Think of this phase as construction.

Phase 3 - 6 Months Before RNOR Ends

This is the completion phase. Finish your restructuring. Transfer or liquidate remaining foreign assets. Sit with a tax advisor and plan the shift to ROR before it happens, not after.

Think of it like defusing a financial clock. Do it in the right sequence and you walk away with everything intact. Rush it or ignore it, and you leave a lot of money on the table.

Phase 1 What to Do With Foreign Savings Immediately After Returning

This is where most returning NRIs go wrong.

Some panic-convert everything to rupees the moment they land. Others do nothing at all and let money sit in overseas accounts with no plan. Neither approach works.

Here's what to actually do:

Don't close your FCNR deposits: If you have Foreign Currency Non-Repatriable deposits running, leave them where they are. The interest remains tax-free during RNOR even after you've returned to India. There's no urgency to break them early. In fact, breaking them before maturity usually comes with a penalty. Let them run.

Open an RFC account immediately: A Resident Foreign Currency account is the right vehicle for you right now. It lets you hold and receive foreign currency income inside India. The interest earned is tax-free during your RNOR period. Think of it as the Indian home for your overseas money that doesn't cost you in taxes. This should be your first financial action after return.

Don't convert NRE accounts to NRO prematurely: Interest on existing NRE deposits may continue to enjoy tax benefits during the RNOR period, subject to FEMA compliance and bank redesignation requirements. Once funds are held in an NRO account, the applicable interest becomes taxable under Indian tax rules. There is a right time to do this conversion. Day one is not that time.

Keep foreign salary, rental income, and overseas capital gains where they are: Don't route them into Indian savings accounts or NRO accounts. Once that money touches the wrong type of Indian account, the tax advantage disappears. It's like letting a perfectly good tax shield rust in the rain.

(Our RNOR Checklist blog and Foreign Currency Accounts blog cover the full account conversion sequence with step-by-step guidance.)

Phase 2 Best Investment Options During the RNOR Period

Now we get to the heart of it.

What should you actually be investing in during these 2 to 3 years?

There are two categories here. Investments that are tax-free during RNOR specifically, and investments that you should start building even though their returns will eventually be taxable. Both matter. Let's take them one at a time.

Tax-Free Investments to Prioritise During RNOR

These are your highest-priority options. They're tax-efficient because of your RNOR status. The window is open. Use it.

FCNR Deposits

Foreign Currency Non-Repatriable deposits are denominated in foreign currency. USD, GBP, EUR, and other accepted currencies. The interest you earn is completely tax-free during your RNOR period. You carry no currency risk because you're earning and holding in the same currency. If you already have FCNR deposits, hold them to maturity. If you're remitting fresh foreign savings, new FCNR deposits are worth considering for the portion you want to keep in foreign currency safely.

Practical tip: Don't break existing FCNR deposits just because you're back in India. The tax-free status continues through RNOR regardless of where you are physically.

RFC Account Deposits

The RFC account is the unsung hero of RNOR planning. Very few returning NRIs know about it or open one quickly enough. You can park your overseas savings here in foreign currency, earn interest that is tax-free during RNOR, and the funds remain freely repatriable if you ever need to send money back abroad. It gives you flexibility without sacrificing the tax advantage.

NRE Fixed Deposits

These are rupee-denominated fixed deposits held in your NRE account. Interest is tax-free during RNOR. If you're remitting foreign savings and converting to rupees, parking the converted funds in NRE FDs rather than a regular savings account gives you the same safety with a meaningful tax benefit. The interest rates on NRE FDs from Indian banks are often quite competitive too.

ELSS Mutual Funds

Equity Linked Savings Schemes are tax-saving mutual funds with a mandatory 3-year lock-in. Start buying ELSS units during your RNOR years. By the time the lock-in ends, you'll have a growing equity portfolio. If you opt for the old tax regime, you may also claim Section 80C deductions on eligible investments. The compounding starts now. The payoff builds over time. Mutual fund investments are subject to market risk. Past performance does not guarantee future returns.

Mutual fund investments are subject to market risk. Past performance does not guarantee future returns.

Indian Investments to Start Building During RNOR

These won't be tax-free. But starting early is what makes the real difference in the long run.

Think of RNOR as the construction phase of your India wealth portfolio. You're laying the foundation while the tax environment is still relatively forgiving.

Equity Mutual Funds

Start SIPs in diversified equity mutual funds. Long-term capital gains on equity funds are taxed at 12.5% above Rs. 1.25 lakh after a holding period of one year. The earlier you start, the longer your compounding horizon. You don't need massive lump sums. A consistent monthly SIP started during RNOR builds serious corpus over 10 to 15 years. Slow and steady genuinely wins here.

PPF (Public Provident Fund)

If you maintained a PPF account before moving abroad, you can continue contributing during RNOR. Contributions qualify for Section 80C deductions under the old tax regime. PPF maturity proceeds are tax-free. It's a low-risk, long-term vehicle that makes strong sense to keep running.

NPS (National Pension System)

RNOR holders can contribute to NPS and claim deductions under Section 80CCD. The additional Rs. 50,000 deduction under Section 80CCD(1B) is available over and above the 80C limit. That's meaningful tax saving during RNOR. It also builds a retirement corpus structured specifically for your India life going forward. Note that these deductions apply under the old tax regime.

Indian Real Estate

If you're planning to buy property in India anyway, the RNOR period is a reasonable window to do it. Rental income will be taxable, but the acquisition itself doesn't create any unusual tax complications. Capital appreciation is a long-term goal. And owning property early in your return helps anchor your financial life in India.

Direct Equity

Once your accounts are re-designated to resident status, you can invest in Indian stocks through a regular resident demat account. Start building a portfolio with a long-term horizon. The fundamentals of good stock investing don't change, but starting early gives your holdings more time to grow.

What to Avoid Investing In During RNOR

Knowing what not to do is just as important as knowing what to do.

Here's the honest list.

Don't put foreign savings into NRO fixed deposits: NRO interest is taxed at 30% with no threshold. That's the same money that could be earning tax-free returns in FCNR or RFC. The difference over 2 to 3 years is significant. This is probably the most common and costly mistake returning NRIs make.

Don't rush all foreign income into Indian accounts: Once money lands in a regular Indian savings account, it loses its tax-advantaged status. Repatriation also becomes more complicated afterward. Move it in planned tranches, through the right account types, on a schedule that suits your RNOR timeline.

Don't lock large sums in illiquid products close to RNOR ending: The transition to ROR may require restructuring. If your money is tied up in long lock-in products you bought in a hurry, you lose the flexibility you'll need most during that transition period.

Don't ignore Schedule FA in your ITR: Even as an RNOR, you are required to declare all foreign assets in Schedule FA of your Income Tax Return. Overseas bank accounts, foreign property, stocks held abroad, pension funds. All of it. Failure to disclose attracts penalties under the Black Money Act, up to Rs. 10 lakh per undisclosed asset per year. The Income Tax department receives foreign financial data automatically through FATCA and CRS international agreements. Non-disclosure is not a strategy. It's a risk.

Don't buy high-commission products from agents who don't understand RNOR: ULIPs and endowment plans are frequently sold to returning NRIs as "tax-saving" options. Most of them are unsuitable for this specific phase. Understand what you're buying and why it fits your RNOR situation before signing anything.

Build Your RNOR Investment Plan With an NRI Tax and Financial Expert. Talk to MostlyNRI.

How Long Can You Keep Your NRE Account After Returning to India?

This is one of the most searched questions by returning NRIs. Let's answer it clearly.

Under FEMA regulations, you are required to re-designate your NRE account to a resident savings account or an RFC account after returning to India permanently. RBI guidelines say this should happen within a "reasonable time," but there is no fixed calendar deadline in the regulations.

In practice, most banks allow NRE accounts to continue for a short transition period while documentation and residency status changes are being processed. But here's the catch. Any interest that accrues after you become a resident is taxable, even if the account still technically carries the NRE label.

For returning NRIs who wish to retain foreign currency exposure or maintain repatriation flexibility, an RFC account is often worth considering. RFC accounts preserve the foreign currency denomination, and interest may remain tax-efficient during the RNOR period subject to applicable rules.

FCNR deposits are a different story. They can be held to their maturity date even after your return. No need to break them early. NRO accounts can simply continue as-is. They were always structured for resident use and were always taxable.

(The full account conversion sequence with timing is covered in our RNOR Checklist blog.)

Foreign Assets and Tax Reporting After Returning to India

Foreign asset reporting requirements depend on your exact residential status under the Income Tax Act and the ITR form being filed. In general, the obligation to report foreign assets in Schedule FA applies to Resident and Ordinarily Resident (ROR) taxpayers.

Returning NRIs should maintain complete records of overseas bank accounts, investments, pension funds, and foreign properties throughout the RNOR period. These records become particularly important as you approach ROR status and your reporting obligations may change.

Failure to disclose reportable foreign assets when required can attract significant penalties under the Black Money Act. Since India receives financial information from many jurisdictions through international information-sharing arrangements such as FATCA and CRS, maintaining proper records and obtaining professional advice is strongly recommended.

Sample RNOR Investment Plan A Practical Example

Let's make this concrete. Meet Arjun.

Arjun is 45. He returned from the US in April 2025. Based on his residency history, he qualifies as RNOR for FY 2025-26 and FY 2026-27. Here's what his financial picture looks like:

- USD 200,000 in overseas savings

- FCNR deposit of USD 50,000 maturing in December 2025

- NRE fixed deposit of Rs. 30 lakh

- NRO account with Rs. 5 lakh in rental income from an Indian property

Here's what a structured RNOR plan looks like for him:

| Asset | Amount | Tax During RNOR | Action |

|---|---|---|---|

| FCNR Deposit | USD 50,000 | Tax-free | Hold till December 2025 maturity, transfer proceeds to RFC |

| RFC Account (new) | USD 150,000 | Tax-free | Open immediately after return, park bulk of overseas savings here |

| NRE Fixed Deposit | Rs. 30 lakh | Tax-free | Maintain till maturity, renew if still RNOR, convert to resident FD when RNOR ends |

| Equity Mutual Funds (SIP) | Rs. 50,000/month | 12.5% LTCG above Rs. 1.25L | Begin SIP from RFC or NRE converted funds |

| NPS Contribution | Rs. 50,000/year | Deductible under 80CCD(1B) | Start contributions for additional deduction under old regime |

| NRO Account | Rs. 5 lakh rental income | Taxable, TDS at 30% | File ITR to claim refund on excess TDS deducted |

Arjun doesn't move everything at once. He sequences it deliberately.

FCNR runs to maturity. RFC is opened immediately for the bulk of overseas savings. NRE FD stays as-is. SIPs begin from converted funds. NPS contributions add a deduction layer. And the NRO account gets cleaned up through proper ITR filing.

That's the discipline that makes RNOR planning actually work.

This example is illustrative only. Individual investment and tax situations vary significantly based on income sources, foreign asset types, residency history, and personal financial goals. Please consult a qualified NRI tax and financial advisor before making any investment decisions based on this example.

Conclusion

The RNOR period sounds long. Two to three years feels like plenty of time.

It isn't.

Before you know it, the window is tightening and you're scrambling to restructure. The NRIs who come out of this transition in the best financial shape are the ones who planned it early, moved deliberately, and got advice that was specific to their situation, not generic NRI advice from someone who doesn't know the difference between RFC and NRO.

Remember that RNOR taxation contains important exceptions. Foreign income that accrues and is received outside India is generally not taxable in India during RNOR. However, income derived from a business controlled in India or a profession set up in India may still be taxable. Professional advice is recommended before restructuring significant assets or investments.

Start with Phase 1. Protect what you have. Then build from there.

All investment information in this article is for general informational purposes only. Mutual fund investments are subject to market risk. Past performance does not guarantee future returns. This content does not constitute financial or tax advice. Individual situations vary significantly. Please consult a qualified NRI tax and financial advisor before making any investment or tax decisions.

Frequently Asked Questions

Can I keep my NRE account during RNOR status?

Yes, for a transitional period. FEMA requires re-designation to a resident account or RFC account after return, but there is no fixed deadline. Most banks allow a short continuation period during documentation processing. The smarter option is converting NRE to RFC rather than a regular resident account. RFC preserves your foreign currency denomination and the tax-free interest status during RNOR.

Does RNOR need to declare foreign assets?

Foreign asset reporting requirements depend on your residential status and the applicable ITR provisions. In general, Schedule FA reporting applies to Resident and Ordinarily Resident (ROR) taxpayers. Returning NRIs should maintain complete records of all foreign assets and seek professional advice regarding their reporting obligations.

Where should NRI invest in India?

During RNOR, start with RFC accounts, FCNR deposits, and NRE fixed deposits for tax-free returns on foreign savings. Alongside those, begin building an equity mutual fund portfolio through SIPs, contribute to NPS, and consider continuing PPF. The goal during RNOR is to build the foundations of an India portfolio while keeping foreign income in tax-efficient structures for as long as possible.

Which return should NRI file?

Most NRIs and RNOR holders file ITR-2. It is required when you have income from more than one house property, capital gains, or foreign assets. If you hold any foreign assets, Schedule FA is a mandatory part of your filing. (See our ITR filing blog for the complete walkthrough.)

How long is RNOR status valid?

Typically 2 to 3 financial years, depending on your specific residency history. The exact duration is calculated based on how many years you were an NRI and your physical presence in India over the preceding 10 years. Once you no longer meet the RNOR conditions, you become ROR and your global income becomes fully taxable in India.

What are the advantages of RNOR status?

The primary advantage is that foreign income, including salary, rental income, capital gains, and interest on FCNR and RFC accounts, is not taxable in India during the RNOR period. This gives returning NRIs a tax-efficient window to remit savings, restructure investments, and build an India portfolio without the full burden of Indian tax on global wealth hitting immediately.

What is the difference between NRI and RNOR?

An NRI is someone who is not a tax resident of India, typically someone living abroad. An RNOR is someone who has returned to India but does not yet qualify as a Resident and Ordinarily Resident under the Income Tax Act. The key practical difference: both NRIs and RNOR holders pay no Indian tax on foreign income. But RNOR is a temporary transitional status. Once it ends, all global income becomes taxable in India.

What is the 90-day rule for non-residents?

Indian tax residency is determined primarily by physical presence in India and specific conditions under the Income Tax Act. Depending on your circumstances, different day-count thresholds may apply, including the commonly referenced 182-day and 120-day tests. Since the rules can vary based on citizenship, income levels, and travel history, residency status should be calculated using your actual facts and travel records.

Will you get a notice if you don't show foreign assets in ITR?

If you are required to disclose foreign assets under applicable tax laws and fail to do so, there is a possibility of scrutiny or notices from the tax authorities. India participates in international information-sharing frameworks such as FATCA and CRS, under which financial information may be exchanged between jurisdictions. Maintaining accurate records and complying with applicable reporting requirements is important.

0 Comments